A 6,150% Surge in OTC Trading Sparks Liquidation of Delisted ETN

A 6,150% Surge in OTC Trading Sparks Liquidation of Delisted ETN

(Bloomberg) -- Barely a month after delisting a suite of notorious exchange-traded notes, Credit Suisse Group AG will kill one off for good following a more than 6,000% price jump in over-the-counter trading.

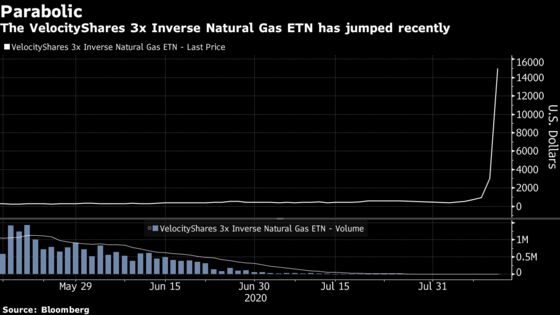

The leveraged inverse product tied to natural-gas futures surged as high as $25,000 on Wednesday from $400 on Aug. 4, creating havoc for traders still involved with the note. Several took to Twitter, claiming they faced huge margin calls to cover short positions.

Confusion grew and questions mounted over the past week as the price surged. On Wednesday evening in New York, Credit Suisse announced it will “accelerate at its option” the VelocityShares Daily 3x Inverse Natural Gas ETN, known by the ticker DGAZF.

In other words, the note will be shut down. Investors will be paid out at an average of its indicative value over several days, which was $124 on Thursday morning in New York versus a closing market price of $15,000 a day earlier.

A spokeswoman for the bank declined to comment beyond the announcement.

Read more: Notorious Cousins of the ETF Are Closing at Almost Record Pace

The drama is the latest twist in the saga of ETNs, a wonky cousin of exchange-traded funds that have become a magnet for controversy.

They trade just like ETFs, but are in fact debt obligations backed by a bank often used to invest in hard-to-access assets. ETNs frequently use derivatives to amplify returns or deliver the inverse performance of whatever they track. In the case of DGAZF, it did both.

The note was one of nine formally delisted by Credit Suisse on July 12 “to better align its product suite with its broader strategic growth plans,” according to the bank. UBS Group AG and Citigroup Inc. have also liquidated products this year.

Margin Calls

As part of the delisting, Credit Suisse stopped creating new shares in the ETN, meaning it was likely to become untethered from the natural gas prices it tracks. The exact reasons behind the surge in DGAZF remain unclear, but the extremity of the move surprised industry watchers.

“Historically there have been funds that had big premiums over the indicative value price when creations were halted,” said Vance Harwood at Six Figure Investing. “TVIX in 2012 is an example, but it ‘only’ went up 100%.”

With the distorted price, most people with a short position could be expected to face margin calls, Harwood said.

A trader who borrowed the note and sold it for around $500 a few weeks ago -- the first step in a short sale -- faced the daunting obligation of buying it back for more $10,000 in order to return shares to the lender. Brokers whose clients are caught in such a bind often demand more money to cover the swelling debt.

DGAZF was a popular short thanks to the tendency of geared notes to steadily decline in value over time, and some 140,000 shares were shorted as of July 31, according to exchange-reported data compiled by Bloomberg.

But it’s a high-risk business -- in a three-times leveraged note like DGAZF, a massive price jump could trigger a huge margin call for even a small short trade.

“The $80 million who were short in DGAZF at end of July could have owed something like $2 billion,” said Eric Balchunas, an ETF analyst at Bloomberg Intelligence.

Terminal users can read about the risks of other delisted ETNs in BI research.

By liquidating the fund, Credit Suisse has effectively “rescued” any investors who had not yet covered their short positions, Harwood tweeted after the announcement. For those who covered at elevated prices “the story is a lot less clear.”

©2020 Bloomberg L.P.