A $51 Billion Manager Says Markets Are Wrong to Cheer Fed Cuts

For Jupiter Asset Management’s Arevalo, the prospect of the Fed’s first rate cut in more than a decade is nothing to cheer about.

(Bloomberg) -- For Jupiter Asset Management Ltd.’s head of emerging-market debt strategy, the prospect of the Federal Reserve’s first interest rate cut in more than a decade is nothing to cheer about.

“The markets are wrongly reading the Fed change of policy into something positive,” said Alejandro Arevalo, who has been shifting his emerging bond portfolio towards more investment-grade debt from junk-rated securities in the past two months. “If they’re cutting rates, it’s because there’s an underlying problem with their economies. We’re becoming more defensive in what I think would be a more bumpy second half.”

Arevalo, who helps manage Jupiter’s $51 billion of assets, said he sold bonds of financial firms in countries where there’s a significant slowdown. By contrast, he’s increased holdings in Brazilian pulp and paper exporters amid an increase in demand from China, as well as in those shipping beef that will benefit as the swine flu hurts the Chinese pork industry. Jupiter declined to disclose the specific fund related to the strategy.

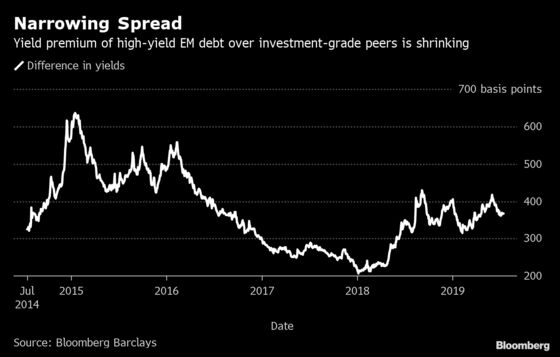

The Fed-led dovish tilt by the world’s biggest central banks has triggered a surge in the amount of negative-yielding bonds, increasing the allure of emerging-market debt. The average yield on EM high-yield dollar-denominated bonds was 7.19% on Tuesday, still about double that of investment-grade securities, Bloomberg Barclays indexes show. The yield earlier in July fell to its lowest level in over a year to 7.09%.

“In many cases, spreads are not reflecting correctly the fundamental of many high-yield companies and countries,” Arevalo said. “With the significant demand we’re seeing of investors chasing yields, it’s a great time to take profits.”

Other views from Arevalo:

- He likes high-rated corporate bonds with low leverage and exporters as they offer a natural hedge to weaker local currencies

- Utilities are also a buy, especially those with long-term contracts and linked to the fluctuations in the dollar

- Consumer companies in the Andean countries of Chile, Colombia and Peru as well as those in India and Indonesia are still “relatively strong”

- A sector to avoid is financials, especially in Turkey, where there is “significant under-reporting” of non-performing loans. They are also to be avoided in China, where asset-management firms are extended arms of the government and may have exposure to unprofitable industries

- The trade war is a “huge amount of concern.” It’s not going away especially in a scenario where President Donald Trump will run for re-election

- The Chinese economy is already under pressure where they’re trying to balance growth and leverage; on top of that, the trade tensions can push Chinese growth lower than the market expects

To contact the reporter on this story: Lilian Karunungan in Singapore at lkarunungan@bloomberg.net

To contact the editors responsible for this story: Tomoko Yamazaki at tyamazaki@bloomberg.net, Karl Lester M. Yap

©2019 Bloomberg L.P.