A $200 Billion World of Exotic Quant Trades Joins Stock Meltdown

A $200 Billion World of Exotic Quant Trades Joins Stock Meltdown

(Bloomberg) -- A burgeoning Wall Street strategy that’s been pitched as a shelter from storms is proving anything but in this once-in-a-century market turmoil.

The world’s biggest asset managers and investment banks have packaged exotic hedge-fund strategies -- known as “alternative risk premia” -- and peddled them to pension funds and wealthy individuals. Make them transparent, accessible and, above all, cheap, and investors will flock, the thinking goes.

All told these funds have an estimated $200 billion overall riding everything from short volatility to trend-following.

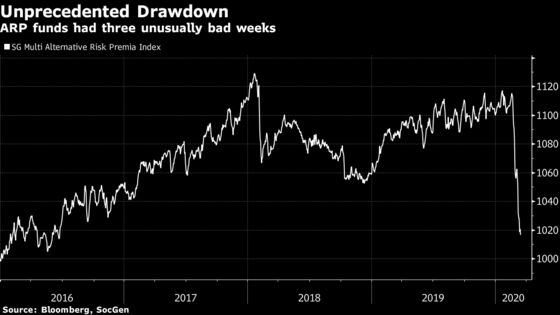

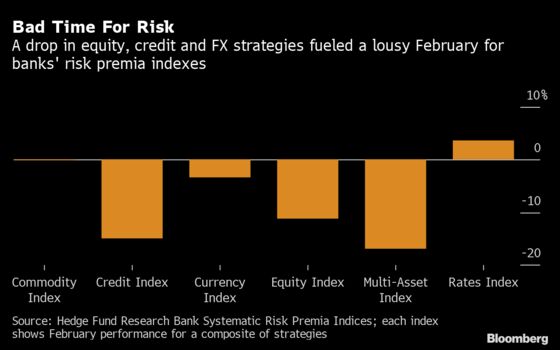

But in their first major stress test, these strategies are faltering. A Societe Generale SA index of the 10 largest products has dropped a record 8% over the past three weeks. A gauge of similar multi-asset strategies sold by investment banks plummeted 17% in February, the most since 2009, according to Hedge Fund Research.

Sure, nearly all investors are in pain. But for ARP funds supposedly designed to deliver returns decoupled from traditional assets, it’s especially disappointing.

“You’re losing money everywhere, so it’s really hard to hide anywhere,” said Clement Leturgie, who manages Lombard Odier Asset Management’s alternative risk premia fund. “A lot of strategies are actually exposed to tail risk.”

Powered by quant research and derivatives know-how, these funds thrived in a world where investors clamored to protect their portfolios but balked at paying hedge fund fees. In contrast to the traditional 2-and-20 hedge fund model, ARP funds charge a weighted average fee of 0.82%, according to MJ Hudson Allenbridge, an advisory firm. Among the biggest players in the space are AQR Capital Management LLC, BlackRock Inc. and GAM Systematic.

A single fund may chase everything from the value factor to merger arbitrage to intraday trend-following to short-volatility across stocks, commodities, currencies, rates and credit. The diverse approach isn’t a flaw -- it’s a virtue, a way of ekeing out consistent returns from a grab-bag of uncorrelated trades, according to the players.

As the past few weeks have shown however, strategies that are uncorrelated in normal times rarely prove so when you really need them to be.

Kari Vatanen, chief investment officer at Veritas Pension Insurance, points to two drags on performance lately. One is that carry is backfiring. Premised on the belief that the relationship between two things will remain stable, carry in volatility, for instance, depends on longer-dated contracts trading higher than short-dated ones. In currencies, it could be borrowing from low-yielding currencies and lending to high-yielding ones in emerging markets.

Those dynamics are virtually unassailable in normal times, but in crises, they can fall out of whack quickly, especially as market turbulence builds.

This week, a hedge fund run by former Goldman Sachs Group Inc. bankers that exploited differences across volatility markets shuttered when those trades went awry.

The other pressure points are coming from the stock component of longer-term trend-following strategies. These were heavily bullish going into the sell-off given that shares had been reliably rallying for most of the past 12 months. Equity factors such as value have also fared poorly in the maelstrom.

“The problem in typical ARP portfolios is that there is too much risk allocation in these two strategy buckets -- carry and trend-following -- and too few strategies that diversify risks,” Vatanen said.

Giving Cover

Some trades have provided cover. Lombard Odier Asset’s ARP fund benefited from a long position in bonds and shorting energy in its trend-following model, says Leturgie.

Intraday momentum has also surged as morning moves in the S&P 500 typically deepen by the close, bolstering this trade. The value strategy in foreign exchange also had a good run at the start of the sell-off as it went bullish on the euro, Societe Generale SA strategists led by Sandrine Ungari wrote in a note.

But a tough few years for these funds is starting to look merely like a prelude to more pain ahead. Even excluding three closures and a risk-on year, total assets in a survey of ARP funds fell by $7 billion from 2018 to 2019, according to MJ Hudson Allenbridge.

“During quiet times it looks like they’re diversifying -- the correlations are low between strategies,” Vatanen said from Finland. “But the problem is that correlations can change dramatically when you are measuring them at the tails of distribution.”

©2020 Bloomberg L.P.