For One Quant Fund, Wider U.S.-German Yield Gap Is a Money-Maker

A $20 Billion Quant Fund Wagers on Wider U.S.-German Yield Gap

(Bloomberg) -- As 10-year U.S. and German yields go their separate ways, QS Investors LLC’s global macro strategy is wagering the spread has more room to run.

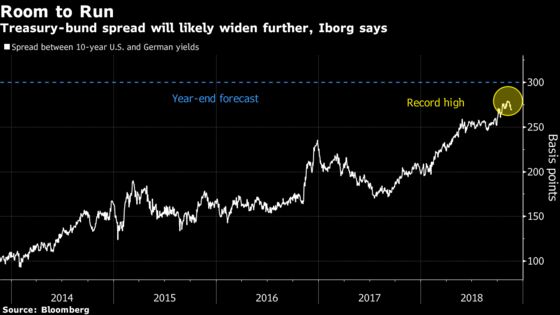

John Iborg, a portfolio manager at the $20 billion quantitative firm, expects the gap between the two rates will widen to a record 300 basis points by year-end, from about 271 now. The firm’s macro fund has expressed this view through interest-rate futures since the start of 2018, when the spread was about 200 basis points.

Underlying Iborg’s confidence is his bearish outlook for Treasuries, which he expects to be pressured lower by a combination of strong U.S. economic data, ballooning debt supply and a Federal Reserve intent on raising rates three or four times next year. On the other side of the trade, he sees bunds staying in a range as European growth cools and the European Central Bank keeps benchmark rates unchanged until late 2019.

“It’s been one of our highest conviction and most profitable trades this year,” said New York-based Iborg, who was previously an interest-rate strategist at JPMorgan Chase & Co. “It’s been our best position on a total return and risk-adjusted basis.”

The 10-year U.S.-German rate differential reached an unprecedented 281 basis points this month as benchmark Treasury yields flirted with their year-to-date high of 3.26 percent. Iborg expects 10-year U.S. yields to return to the 3.25 percent area by year-end, from 3.08 percent currently. German 10-year debt yields about 0.37 percent.

Human Intervention

The global macro strategy he helps oversee relies on tactical models that take into account inputs such as momentum, yield curves and capital flows to identify potential trades. While the macro portfolio is “heavily driven” by those models, managers can intervene.

When it comes to the Treasury-bund spread, however, the computers and Iborg’s fundamental views align.

“The last employment report was strong, inflation continues to meet market expectations -- that all points to the Fed staying on track,” he said. But in Europe, “I don’t think there’s any reason for growth to exceed expectations in the near future, so that equals bunds treading water into year-end.”

While Treasury yields have climbed to multi-year highs across the curve this year, bunds have had a decidedly less dramatic 2018. After touching their highest level since 2015 in February, 10-year German yields have traded between 0.3 percent and 0.6 percent for the past few months, and are below where they ended 2017.

The same forces that should drive U.S. and German yields apart will likely send the euro and the dollar in opposite directions as well, according to Iborg. For that reason, QS’s macro fund is positioned to benefit from further dollar strength against the euro. The greenback has gained about 5.5 percent against the common currency in 2018.

“We’re long the dollar and short euro, and that’s one of our higher conviction views as well,” Iborg said. “It’s along the same lines of reasoning for our Treasury-bund spread -- this divergence in economic growth, coupled with rates rising in the U.S. and not so much in Europe.”

To contact the reporter on this story: Katherine Greifeld in New York at kgreifeld@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Mark Tannenbaum, Ven Ram

©2018 Bloomberg L.P.