A $2 Trillion Debt Deluge Means BOJ Needs to Buy More Bills

A $2 Trillion Debt Deluge Means the BOJ Needs to Buy More Bills

(Bloomberg) -- A surge in Japan’s bill issuance is exerting upward pressure on yields and reinforcing the case for the central bank to buy more.

Yields on three-month treasury bills rose to -0.06% last week, a level last reached in early 2016 before the Bank of Japan introduced its negative rate policy. Demand from global funds, typically the biggest buyers, has failed to keep pace with supply, prompting the BOJ to step up purchases.

The government’s $2.2 trillion stimulus plan has unleashed a flood of bond supply, with issuance set to increase by almost two-thirds in the current fiscal year. While borrowing costs remain low by historical standards, the uptick in yields threatens to infect other parts of the curve and weigh on the nation’s hefty debt burden.

“The BOJ may be thinking that it can let the market absorb supply as long as it doesn’t affect yield curve control given debt issuance is likely to decrease next fiscal year,” said Toru Suehiro, senior market economist at Mizuho Securities Co. in Tokyo.

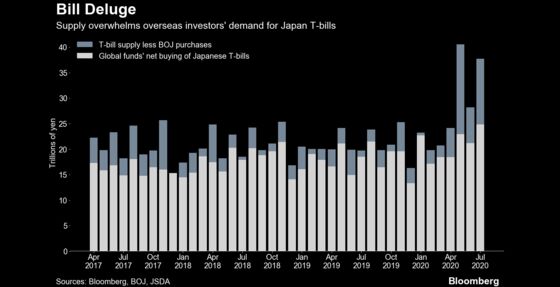

Global funds haven’t been able to absorb the glut in supply despite buying more.

They purchased a net 24.8 trillion yen in July, according to the latest data from the Japan Securities Dealers Association released on Thursday. This compared with a net supply of 37.7 trillion yen during the month, which is the difference between the amount sold by the government and bought by the central bank.

More than two-thirds of the nation’s negative-yielding T-bills were owned by global funds as at end-March, based on BOJ figures. These investors borrow yen from their Japanese counterparts at deeply negative rates while lending dollars, earning an extra yield pickup. But ample dollar supply from the Federal Reserve in recent months has capped these premiums.

T-bill yields have dipped since Aug. 12, the day the BOJ increased daily purchases by 1 trillion yen to 3 trillion yen.

“Bill yields have risen because the basis isn’t favorable for foreign investors,” said Naomi Muguruma, senior market economist at Mitsubishi UFJ Morgan Stanley Securities Co. “Given the negative-rate policy, the BOJ couldn’t tolerate a continuous rise in yields, and that’s why it increased purchases.”

Local banks also own these bills, and lenders can use them as collateral for yen and dollar loans from the central bank.

“Collateral demand for T-bills from banks has declined,” said Souichi Takeyama, a rates strategist at SMBC Nikko Securities Inc. “It all comes down to whether or not the BOJ will increase purchases” to contain a rise in bill yields, he said.

©2020 Bloomberg L.P.