A $152 Billion Contrarian Says 10-Year Treasuries May Hit 3%

We should not underestimate the speed with which the market can reprice, Franklin Templeton’s Sonal Desai said.

(Bloomberg) -- Sonal Desai, chief investment officer of Franklin Templeton’s $152 billion fixed-income group, has an upbeat view of the U.S. economy that’s persuaded her to go against the grain in the Treasury market.

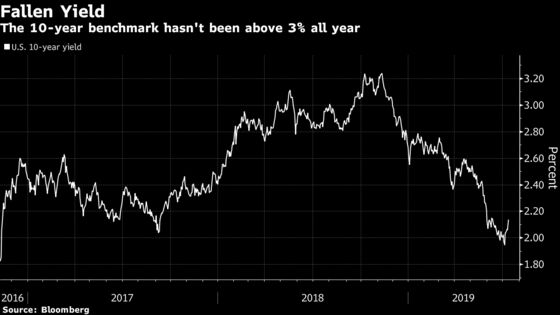

While much of the Wall Street crowd sees a decline in yields, she believes Treasury 10-year rates could jump toward 3% by year-end from just above 2% now. That should happen as a stream of solid reports prompts a swift reappraisal by investors of the economy’s health, she said.

“We should not underestimate the speed with which the market can reprice,” Desai said in an interview. Recent history shows rapid moves are possible: 10-year yields were at 3.25% in November, plunged as low as 1.94% this month and have since climbed to 2.13%.

“Can the 10-year yield get to 2.50%, 2.60%, 2.75% this year? Why not?” she said. The economy is in “incredibly good health,” she added, pointing to the better-than-estimated 224,000 jump in U.S. payrolls in June. Desai is finding “select” opportunities in U.S. corporate debt rated triple B that will do well under a scenario of rising yields.

Overshooting

When speaking before Congress this week, Federal Reserve Chairman Jerome Powell signaled that the central bank is preparing to cut interest rates. His testimony made Desai more confident that a 3% benchmark U.S. yield is “achievable” because “both the markets and the Fed are overshooting in pushing yields lower, setting the stage for a rebound,” she said. Desai expects Fed officials to deliver a 25-basis-point reduction on July 31, when the more “sensible” approach would be to remain on hold.

This is not the first time this year that Desai is forecasting higher Treasury yields, a call she’s made as the bonds rallied through the months. She said in February that the 10-year yield could reach 3.5% in the medium term, and made a 3% or more prediction in April. Other market participants including Credit Suisse Group AG and JPMorgan Chase & Co. have also warned that bonds are at risk of a sell-off.

“The Fed is continuing to cave to markets pressure by not looking at the data,” said Desai, a former assistant university professor and economist for the International Monetary Fund, who fears the central bank is heading into “dangerous” territory.

The U.S. labor market should remain solid through the summer, boosting consumption, and manufacturing and investment will gradually pick up once inventories clear. “Markets will realize that the economy is as strong as it was last November, when 10-year yields were above 3%,” only this time there will be Fed stimulus, still-easy fiscal policy, and rising wages and inflation expectations, Desai said.

Sudden Shift

“It will then not take long for investors’ views to suddenly turn around and push yields back up,” she said.

For now, asset prices appear to be based on little more than the size of the Fed’s next move. The stock market’s sell-off last week in response to the strong June jobs report was “a really bad sign” that investors are “trading on moral hazard,” the Indian-born money manager said from her offices in San Mateo, California, a suburb outside San Francisco.

The odds are growing that a financial-asset bubble will trigger the next recession, but not before Treasury yields surge, according to Desai. In her mind, “the real debate” is whether the next U.S. downturn looks more like the 2001 recession that lasted eight months or the deeper 2007-2009 contraction that was the worst since the Great Depression.

“A rate cut at this stage will just cause more froth and exacerbate distortions in asset markets,” she said. “It pushes valuations of risky assets even further away from fundamental values. For our investment strategy, that means it is even more important to be very selective.”

While not yet seeing signs of broad-based bubbles, Desai said she’s watching the corporate-credit sector closely. Desai sees a “remote” risk of widespread downgrades for most issuers of U.S. corporate bonds rated triple B, the lowest investment-grade rating. In addition, certain emerging-market corporate bonds, which have lagged behind U.S. credit in returns this year, also offer opportunities because fundamentals “have generally been improving” in some regions.

“Right now, you’re choosing from among assets you dislike the least,” she said with a laugh. The challenge is to “not play into the Fed’s attempts to move investors into greater risk,” she said. At the same time, “now is not the time to be sitting on cash, but it is a time to get very cautious.”

--With assistance from Ruth Carson.

To contact the reporter on this story: Vivien Lou Chen in San Francisco at vchen1@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Nick Baker, Mark Tannenbaum

©2019 Bloomberg L.P.