A $100 Billion Fund Manager Predicts Credit Slump Will Worsen

A $100 Billion Fund Manager Predicts Credit Slump Will Worsen

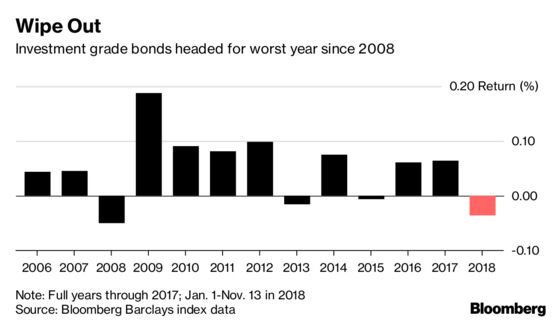

(Bloomberg) -- The worst year for corporate debt in a decade is just the start of the slump.

That’s according to Jason Shoup, head of global credit strategy at Legal & General Investment Management America, who said that rising rates, fading stimulus, weaker earnings and potentially more downgrades all add up to a tough year ahead for U.S. investment-grade credit.

“It just feels like a much more risky proposition than it did a year ago,” said Shoup, whose Chicago-based firm manages $186 billion in assets, including $100 billion in fixed income, in a phone interview. “There really is no corner in which you can obviously hide.”

High-grade bonds may be able to claw back some of the steep losses seen in October if issuance slows, Asian investors stop selling and stock markets stabilize, Shoup said in a Nov. 9 phone interview. Still, next year looks dicey.

“I wouldn’t be surprised if the second half of 2019 really poses some significant challenges and could result in wider spreads,” Shoup said. “Without that central bank support and transitioning off the fiscal stimulus, our long-term outlook for investment grade is definitely on the more bearish side over the last two to three years.”

Below are more highlights from the interview:

Slowing Growth

- As the Federal Reserve reduces its balance sheet and higher rates weigh, the economic boost from U.S. tax cuts should fade, Shoup said.

- “The contribution of fiscal stimulus to growth has to slow. It’s not like we’re going to do another tax cut on the same order of magnitude that we once got,” he said.

- That will slow growth -- possibly by at least 1 percentage point after the second quarter -- which along with rising input costs fueled by trade wars, should have a negative impact on corporate profits.

Downgrade Risk

- That could mean billions of dollars in BBB rated bonds will be cut to junk.

- “The concern is that companies can get behind on that deleveraging path and if profits really do slow meaningfully over the next 12 to 18 months, you would think that more and more of those companies are going to get behind and be subject to potential downgrade risk or at least repricing risk,” Shoup said.

- As General Electric Co. trades more like high yield, Anheuser-Busch is also a concern, Shoup said.

- “If Anheuser-Busch loses its Moody’s rating -- which we think is likely -- do we get a repeat of GE, in terms of Anheuser-Busch? At the moment I would say Asia has been selling GE risk but has been willing to buy Anheuser-Busch risk, so it seems less likely,” Shoup said.

Liquidity Wildcard

- Shoup said he expects less liquidity in the market will cause more volatility.

- Secondary liquidity is worse than it was during the last big credit sell-off at the beginning of 2016. The shape of the yield curve has made dealers reluctant to hold bonds because of the negative carry, just as foreigners may be becoming more reluctant to buy, according to Shoup.

- “Asia and the foreign bid has been such an important component to demand in the credit markets in the last few years. Any sniff that they’re going to turn into a seller of a certain name has this potential to trade an exaggerated move wider,” he said.

Diamonds in the Rough- Shoup said he sees potential opportunities in energy pipeline and financial sector bonds. Temporary increases in leverage by Master Limited Partnerships, so that holding companies can buy out operating units, make those bonds attractive, he said.

- “The Williams, the Energy Transfer Partners -- those are companies that trade on the riskier side in terms of spread and we think that that will continue to outperform,” Shoup said, adding that his firm has a strong conviction about the trade.

- Legal & General also likes banks, particularly after they failed to issue new debt following earnings. Shoup said he is “cautious” on the pharmaceutical sector, and is awaiting more mergers and acquisitions.

- Underscoring its defensive positioning, Legal & General has a higher than average allocation to cash and Treasuries, he said.

To contact the reporter on this story: Jeremy Hill in New York at jhill273@bloomberg.net

To contact the editors responsible for this story: James Crombie at jcrombie8@bloomberg.net, Randall Jensen, Dave Liedtka

©2018 Bloomberg L.P.