A 1% Treasury Yield Proves Elusive With Pandemic Intensifying

A 1% Treasury Yield Proves Elusive With Pandemic Intensifying

(Bloomberg) -- The bond market is demonstrating that the road to higher Treasury yields is going to be a rocky one, leaving bets on a reflating economy and a steeper curve hanging in the balance.

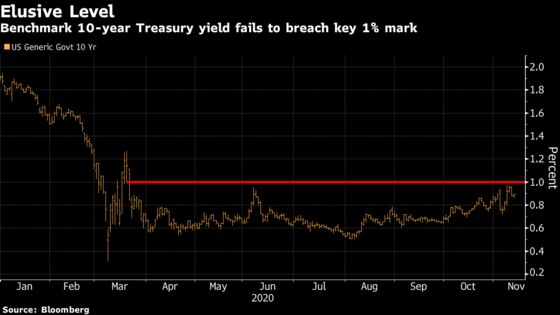

All eyes in the world’s most important debt market were on the 1% level on 10-year Treasuries last week, as a volatile, post-election selloff pushed the implied yield on futures within a hair of touching that mark for the first time since March. Surging coronavirus cases then took over the narrative, fueling a rally that left the cash rate at 0.9% to end the week.

Traders are now bracing for more wild swings, given the potential for tighter social-distancing restrictions that could darken the economic outlook, even as hopes for a vaccine build. An extended failure to breach 1%, which seemed like almost a sure thing just days ago, may eventually give pause to those wagering that a growth rebound will generate inflation and finally jolt yields decisively from near record lows. But for now, many investors are still leaning toward higher longer-maturity yields, with speculators holding a near-record short position on bond futures.

“The trend is still toward higher rates and a steeper curve,” said Scott Buchta, head of fixed-income strategy at Brean Capital. But given the daily swings seen in November, “we should not be surprised to see these larger intraday moves take place as they are driven primarily by headlines, supply and positioning.”

Even as the 10-year note pared its losses this past week, its yield still appears to have entered a higher range. It’s averaging about 0.86% in November, compared with 0.78% in October. It’s a similar story for the spread between 5- and 30-year yields, which was near the widest level since 2016 last week.

Granted, with the virus raging, some traders took a punt on another rally toward the end of last week, with demand emerging for Treasury options targeting a 0.70% 10-year rate.

Leaning Steeper

But many on Wall Street project a steeper yield curve, given the Federal Reserve’s commitment to keep front-end rates low along with the potential for more fiscal stimulus and a vaccine to help the economy recover.

See here for more on reflation bets.

Goldman Sachs Group Inc. sees the steepener as a key investment theme for 2021, saying the 10-year yield should reach 1.3% by the end of next year.

Given the lack of major economic data in the days ahead, investors will be attuned to news around the pandemic and whether its intensification increases pressure on lawmakers to forge a new stimulus package.

According to Buchta, one reason the 10-year yield failed to hit 1% is that there was a large pool of buyers ready to step in whenever the rate hovered just below that level.

Part of the momentum for this past week’s rebound in appetite for Treasuries came after the market absorbed a record $122 billion in quarterly refunding auctions, with the 30-year sale showing signs of solid foreign demand.

Buchta reckons it may take a few tries to get the 10-year rate past 1%, but he says once it breaks, “the market may look toward 1.20% as the next level of major support.”

Beyond that, firms such as Bank of America Corp. see little chance of the 10-year rate climbing above 1.35% in coming weeks.

Ed Tollefsen, senior vice president of sales and trading at investment bank Blaylock Van in Oakland, California, also sees the 10-year rate getting to 1% over time, though the market may endure “disjointed, very uneven” moves until then.

“Market participants know that rates in general are going to have to rise from these levels,” he said. Still, “we are in for volatility through the end of the year, in my opinion.”

What to Watch

- Macro highlights include Fed Vice Chair Richard Clarida’s participation in a discussion of the economic outlook.

- The economic calendar:

- Nov. 16: Empire State manufacturing survey

- Nov. 17: Retail sales; import/export prices; industrial production; business inventories; NAHB housing index; Treasury International Capital flows

- Nov. 18: MBA mortgage applications; building permits; housing starts

- Nov. 19: Weekly jobless claims; Philadelphia Fed business outlook; Bloomberg economic expectations; leading index; existing home sales; Kansas City Fed manufacturing activity

- The Fed calendar:

- Nov. 16: Clarida

- Nov. 17: Four Fed presidents -- Atlanta Fed’s Raphael Bostic, San Francisco Fed’s Mary Daly, Minneapolis Fed’s Neel Kashkari and Boston Fed’s Eric Rosengren -- discuss racism and the economy

- Nov. 18: New York Fed’s John Williams; St. Louis Fed’s James Bullard; Dallas Fed’s Robert Kaplan; Bostic

- Nov. 20: Kaplan; Kansas City Fed’s Esther George

- The auction schedule:

- Nov. 16: 13-, 26-week bills

- Nov. 17: 42-, 119-day cash-management bills

- Nov. 18: 20-year bonds

- Nov. 19: 4-, 8-week bills; 10-year TIPS reopening

©2020 Bloomberg L.P.