The Quant Revolution Is Coming for Corporate Bonds

The Quant Revolution Is Coming for Corporate Bonds

(Bloomberg) -- If the quant revolution disrupts corporate bonds one day, you might want to remember this name: Roni Israelov.

The wiz at AQR Capital Management just sketched a blueprint for traders seeking to hitch a high-octane ride on the global credit cycle -- powered by the very finance tools that have changed Wall Street’s game on stocks.

This is technical stuff, for sure. But in a nutshell, Israelov’s recent paper draws on the fine art of factor investing to distill the ingredients that have served up returns in credit over the past two decades.

The payoff from this data-mining: Money managers can replicate exposure to the asset class via derivatives tracking government bonds and stocks, according to the principal at the $203 billion firm.

It’s a top-down approach compared with previous efforts that group obligations by characteristics like momentum and value -- and it’s a window into the budding quant quest to dig goldmines in the world of corporate debt.

This putative portfolio stuffed with futures and options could help investors “who desire enhanced liquidity and cash efficiency or want to explicitly target duration, equity and volatility exposures,” Israelov said in a telephone interview.

Aficionados of capital-structure theory may sniff the premise here: Robert Merton’s model of debt. That method sees credit investing as economically equivalent to selling a put option on a firm’s assets and holding a risk-free bond.

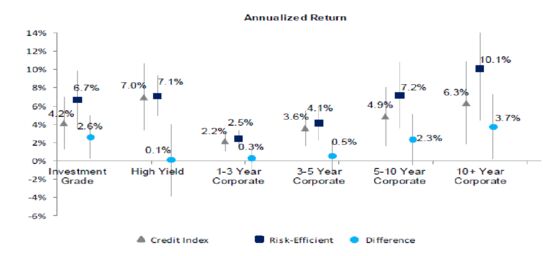

If one accepts this mantra, there are four principal exposures that explain up to 76% of corporate-debt returns, Israelov calculates: government obligations, equities, stock volatility and price swings in bonds. In his parlance, these are the most-rewarded risks out there for credit buyers.

In that spirit, investors can garner exposure to the asset class via a portfolio of fixed-income and equity-index futures, combined with selling options on a stock index and bond futures, according to the paper. All without holding cash bonds -- with smaller drawdowns and lower volatility compared with benchmarks.

Israelov, who oversees AQR’s volatility-trading strategies, declined to comment on whether the firm plans to employ the strategy in any of its funds.

Martin Fridson, an early pioneer of high-yield bond math, likes what he sees here.

While the findings won’t threaten traditional corporate-bond investing anytime soon, “institutional investors who already give mandates to quant managers should be open” to the derivatives-based strategy, says the chief investment officer of Lehmann Livian Fridson Advisors.

Quant Quest

Quants have been tip-toeing into corporate bonds of late, with big-name firms like AQR and BlackRock Inc. applying factors traditionally associated with equities to credit. Connecticut-based AQR last year launched its first fixed-income mutual fund, which has gathered around $100 million in assets.

Meanwhile, the likes of Robeco and JPMorgan Asset Management have waxed lyrical about the potential for factor investing in debt.

But it’s been slow going, as bonds present technical challenges not present in equities, such as varying maturities and lack of reliable prices for thinly traded issues.

Caveats abound, of course. Swaths of money managers are constrained in their use of derivatives and prefer corporate obligations for regulatory or accounting purposes, as Israelov acknowledges. Whether to amass futures and options, or go vanilla naturally depends on context, according to the AQR principal.

“Corporate bonds may be more appropriate in many instances, including for those who want to express a view on individual bonds or desire steady cash flows,’’ he said.

But for programmatic and fundamental traders free of such constraints, Israelov’s paper may provide a glimpse into a quant-driven future for the world of credit.

To contact the reporter on this story: Yakob Peterseil in London at ypeterseil@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma

©2019 Bloomberg L.P.