‘Extreme’ Stock-Valuation Gap Looms Over Gravity-Defying Rally

‘Extreme’ Stock-Valuation Gap Looms Over Gravity-Defying Rally

(Bloomberg) -- As the S&P 500 approaches all-time highs, defensive investing styles are trading at their most overbought levels in decades -- a sign of investor incredulity at this gravity-defying rally.

Something may have to give.

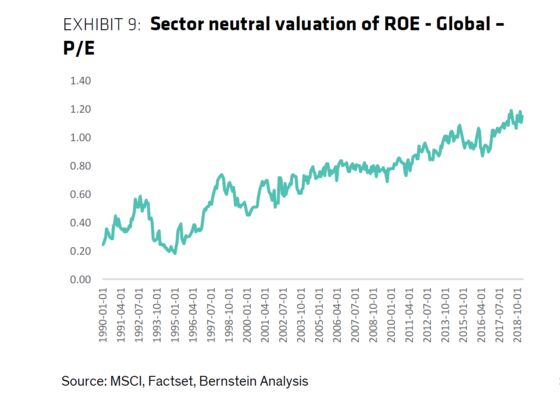

Growth shares have surged to the highest levels versus cheap equities since the dot-com bubble, underscoring fierce demand for companies less exposed to the gyrations of the economic cycle. Stocks posting a strong return on equity are near their most expensive since 1990, according to Sanford C. Bernstein & Co. To cap it all, tech multiples have jumped toward 2009 highs relative to the broader gauge.

It all suggests an “extreme” valuation gap is setting the stock market up for a rotation away from winners in favor of the losers, according to Morgan Stanley, echoing a growing number of Wall Street strategists.

“It is pretty clear that the market is fairly bifurcated at this point with growth and defensive companies designated as winners and everything else a loser,” Morgan Stanley strategists led by Mike Wilson wrote in a Monday note. “That’s a classic late-cycle playbook but it does appear to have gotten a bit extreme at this point.”

Despite one of the best starts for global equities in decades, economic angst and the weaker trajectory for corporate earnings are spurring investors to crowd into the strongest companies, from healthy balance sheets, low volatility equities to the FAANG.

Among smart-beta products, exchange-traded funds tracking quality stocks saw their biggest inflows last week since January, belying ultra-low cross-asset volatility.

With money managers paying a hefty premium for defensive bets, many of the stocks best positioned to ride an economic downturn now look overbought, according to Bernstein.

“With a U.S. recession widely expected at some point over the next 12-18 months and very little earnings growth forecast in Europe, many wish to be positioned in "Quality,” strategists led by Sarah McCarthy wrote in a note last week. “However the valuations seem prohibitive.”

Bernstein recommends European stocks with high earnings quality, which favors metrics like steady profit forecasts, and global shares with low leverage.

Shifting Tide

Cyclical sectors overall have posted aggressive gains this year but the likes of materials and financials -- likely overweights in value funds -- have underperformed markedly.

Still, there are nascent signs of an investing shift less friendly to the market leaders and kinder to the laggards.

Relative to the U.S. benchmark, a gauge of American banks has rebounded 4 percent from a 2 1/2-year low reached in March. Meanwhile, the woes afflicting health care thanks to proposed policy changes are a reminder that the most-loved sectors can fall out of favor on a dime.

As recovering bond yields weigh on valuation multiples, cheaper equities may look more attractive. Since October, value’s weighting in portfolios tracking the price-momentum factor has increased at the expense of growth, a trend that could spur inflows into the investing style, according to Morgan Stanley.

In sum, the most-loved equities look decidedly expensive in this melt-up. And all bets are off on how they will fare in any correction, with the projected earnings expansion for growth stocks this year not much stronger than peers, Wilson and team note.

“The next leg of this rotation could occur during an overall correction in the S&P 500 as growth stocks go down a lot more than value given their higher relative valuations,” the strategists wrote. “The difference this time is that we think the correction will be driven more by disappointing earnings growth rather than higher interest rates.”

To contact the reporter on this story: Justina Lee in London at jlee1489@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Sid Verma, Samuel Potter

©2019 Bloomberg L.P.