IPOs Are Fashionable Again. Beware of the Hangover: Taking Stock

IPOs Are Fashionable Again. Beware of the Hangover: Taking Stock

(Bloomberg) --

After a very quiet first quarter for IPOs, things are now bubbling again on that front, a sign of renewed investor confidence as European stocks keep adding to their new-year gains. However, not all new listings are skyrocketing.

Valuation levels are back to acceptable levels and appetite for IPOs has been recovering, making the period an ideal window for private companies to go public. April has already seen the highest value of traded IPOs since last October, with about $5.1 billion coming to the market.

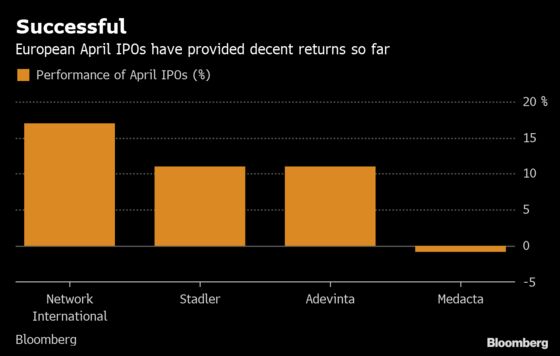

European investors had no big IPO name to trade since January. This month has been the first to see a decent size of listings, including Swiss trainmaker Stadler last Friday, which rose 13 percent on its first day of trading. At the other end of the spectrum, medical device manufacturer Medacta was less buoyant, and is now trading below its initial offering price.

Tomorrow will see Italian payment-service company Nexi trade for the first time. The books were largely oversubscribed. A repeat of Adyen’s performance (~190% return since listing on June 13 last year) may be what investors are wishing for. The listing in London of Dubai-based payment service firm Network International Holdings also went well.

But not everyone is IPO hungry.

“The problem with IPOs: they come in waves and they compete with each other as well,” says Gavin Launder, a fund manager at Legal & General Investment Management. “Not just like for like, but literally, no one’s going to do all the IPOs. So Network International yes, but therefore Nexi probably not, because they’re too similar. When you get a wave of IPOs, we’re quite careful,” he says.

The recent examples show the demand for IPOs is relatively buoyant. Companies and investment banks usually wait for market conditions to be good to list shares, in order to achieve the best pricing. That can haunt investors if the market turns however, or if the valuation was stretched in the first place.

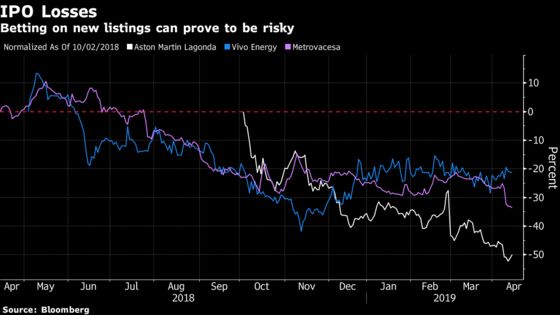

And, as other IPOs after Adyen showed, not everything does well. Aston Martin’s IPO last year is a good example. Priced like competitor Ferrari, the British carmaker did not live up to the expectations. The stock hit a new low last week and has erased about 50 percent of its value. Metrovasca and Vivo Energy also lost value after their IPOs.

There are other reasons to be cautious about the recent wave of new listings. “There’s also a nasty suspicion that these are the ones that didn’t get away in to the fourth quarter of last year and, well, ‘the market’s recovered let’s get them out quickly!’” Launder says. “So we’re quite careful about who we’re buying from as well. If it’s raising money to invest in the business, that’s good. If it’s private equity that only had it two years, and it’s levered it up and it’s getting out, not so good.”

In the meantime, Euro Stoxx 50 futures are trading up 0.2% ahead of the open.

SECTORS IN FOCUS TODAY:

- Watch trade-sensitive stocks after Treasury Secretary Steven Mnuchin said the U.S. is open to facing “repercussions” if it doesn’t live up to its commitments in a potential trade deal with China, in a sign that the two sides are edging closer to an accord. Japan said trade tensions are among the reasons for its pessimistic outlook on the global economy and the U.S. itself faces the paradox of pushing for global growth as demand is dragged by its own policies.

- Watch the pound and U.K. stocks, as there is precious little sign thus far that Conservative and Labour politicians in the U.K. are finding a way towards a compromise on Brexit, leaving the pound hanging in suspended animation and Prime Minister Theresa May facing attacks from her own party.

COMMENT:

- “The Brexit uncertainty is not going away and may well become the new norm going forward,” Barclays strategist Emmanuel Cau writes in note. “The six-month extension of Article 50 granted to the U.K. by the EU last week will continue to keep investment and hiring decisions on hold, but a ‘no deal’/hard Brexit looks increasingly unlikely in our view. We thus stick to a small preference for domestic plays over exporters in the U.K., as the former are cheap and under-owned, but acknowledge that domestic outperformance may take time to materialize. In the meantime, Mining and Energy are the two sectors we like the most in the U.K., as both are being supported by improving global activity, pro-growth Chinese policy and dovish Fed.”

COMPANY NEWS AND M&A:

- Publicis to Buy Alliance Data’s Epsilon for $4.4 Billion

- Publicis Sees Higher Organic Growth in 2019 Compared to 2018

- Volkswagen CEO Plots Major China Push as Trouble Looms at Home

- Volkswagen Says China Demand Picked up in April on VAT Cut

- Daimler Cooperating With Authorities on Cheating Allegations

- Macron Set to Back EDF Nuclear Ops Renationalization: Parisien

- Vivendi First Quarter Revenue EU3.46b, Est. EU3.38b

- Rio Boosts Arizona Mine Spending to $2 Billion in Copper Chase

- Regulators Call on Deutsche Bank to Further Shrink U.S. Unit: FT

- Michelin Sets IDR843/Share Tender Offer Price for Multistrada

- Baloise Buys Belgian Insurer Fidea From Anbang for EU480 Mln

- Brewin Dolphin in Talks to Buy Investec Irish Wealth Mgmt Unit

- Bauer Sees 2019 Revenue About EU1.7b, Ahead of Estimate (2)

- Sabadell’s TSB Plans Refunds for Customer Losses Tied to Fraud

- Galp 1Q Average Net Entitlement Production 110.8 Kboepd

NOTES FROM THE SELL SIDE:

- Morgan Stanley says Norsk Hydro shares are seen outperforming sector by 3-4% after Alunorte and Brazilian public prosecutors jointly petitioned a federal court to lift production embargo at the aluminum refinery. Keeps overweight, base case that Alunorte will return to full production in 2Q and production at 100% for 3Q.

- RBC writes the investment case for Fevertree rests on the prospects for growth outside of the U.K. and particularly in the tough-to-crack U.S. market, upping PT to 3,800p from 3,500p.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 392.7 (July high); 403.7 (100% Fibo)

- Support at 385.7 (76.4% Fibo); 374.5 (61.8% Fibo)

- RSI: 65.6

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,516 (76.4% Fibo); 3,596 (May high)

- Support at 3,403 (61.8% Fibo); 3,309 (50% Fibo)

- RSI: 68

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- EDP upgraded to buy at HSBC; PT 4 Euros

- Sulzer upgraded to outperform at MainFirst; PT 119 Francs

DOWNGRADES:

- Atlas Copco downgraded to hold at HSBC; Price Target 280 Kronor

- Centrica downgraded to neutral at JPMorgan; PT 1.25 Pounds

- Inficon downgraded to hold at HSBC; PT 575 Francs

- LEG Immobilien cut to hold at Bankhaus Lampe; PT 109 Euros

- Nokia downgraded to sell at Goldman; PT 4.70 Euros

- Pfeiffer Vacuum downgraded to reduce at HSBC; PT 131 Euros

- VAT downgraded to reduce at HSBC; PT 102 Francs

- Wacker Chemie downgraded to add at AlphaValue

INITIATIONS:

- Alcon rated new buy at Jefferies

MARKETS:

- MSCI Asia Pacific up 0.1%, Nikkei 225 up 1.4%

- S&P 500 up 0.7%, Dow up 1%, Nasdaq up 0.5%

- Euro up 0.07% at $1.1307

- Dollar Index down 0.11% at 96.87

- Yen up 0.11% at 111.9

- Brent down 0.3% at $71.3/bbl, WTI down 0.5% to $63.6/bbl

- LME 3m Copper up 0.1% at $6493.5/MT

- Gold spot down 0.2% at $1288.4/oz

- US 10Yr yield down 1bps at 2.55%

MAIN MACRO DATA (all times CET):

- 10:30am: (IT) Feb. General Government Debt, prior 2.36t

--With assistance from Phil Serafino.

To contact the reporters on this story: Michael Msika in London at mmsika4@bloomberg.net;Lisa Pham in London at lpham14@bloomberg.net

To contact the editor responsible for this story: Blaise Robinson at brobinson58@bloomberg.net

©2019 Bloomberg L.P.