Why Aren’t Markets Worried About Profit Warnings?: Taking Stock

Why Aren’t Markets Worried About Profit Warnings?: Taking Stock

(Bloomberg) -- Ahead of the earnings season, European shares are bubbling near an eight-month high, making yesterday’s retreat seem mild against the broader rally. In the past quarter, several big companies issued profit warnings, yet the reaction of investors has been somewhat surprising.

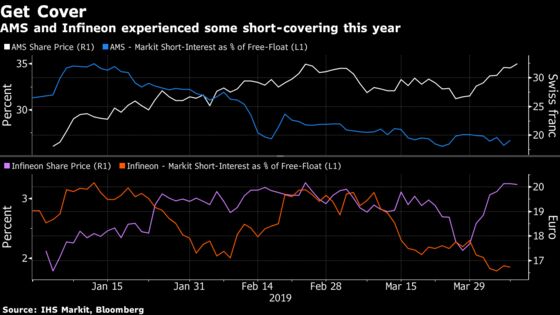

Among the names that have caught my eyes are a number of major European tech companies, namely Infineon, AMS, ASML and Ingenico. Infineon has gained 15 percent this year. Infineon quickly recovered from a profit warning in late March. AMS warned in February and even suspended its dividend, but the shares are near a five-month peak now.

Part of that may be a correction from excessive pessimism in late 2018, when a lot of bad news got priced in. Also, it seems that short-sellers have at least partially covered their positions on some of these stocks since then.

It’s not just the tech sector. German carmaker BMW has also recovered its losses after cautioning on earnings. Among financials, France’s BNP Paribas simply shrugged off its warning, while Julius Baer is up a staggering 17 percent two months after cutting its targets. Even UBS has recovered after sayings its last quarter was among the worst environments in recent history.

| Stock | 1-day change on profit warning | Returns since profit warning | Date of profit warning |

| AMS | -6.9% | +29% | Feb. 5 |

| ASML | +0.9% | +26% | Jan. 23 |

| Infineon | -5.2% | +13% | Mar. 27 |

| Ingenico | -14% | +44% | Jan. 23 |

| BMW | -4.9% | +1.7% | Mar. 20 |

| BNP Paribas | +1.8% | +6.5% | Feb. 6 |

| Julius Baer | -4.4% | +17% | Feb. 4 |

| UBS | -2.4% | +1.3% | Mar. 20 |

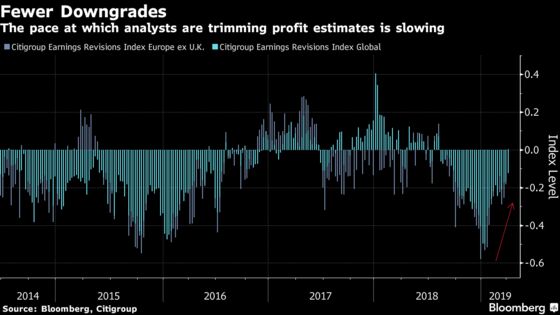

One possible reason for the strength is that earnings-per-share expectations seem to be on the rise after several months of decline. After a rally driven by dovish central banks, easing trade tensions and signs of a bottom out in PMIs, companies may need to show some profit growth. At the moment, the expectation bar is still quite low.

Obviously, there are exceptions. Airlines are a good example. Lufthansa and Easyjet warned about their earnings this year and the shares have yet to recover. The sector was penalized by Brexit uncertainty, rising oil prices as well as margin pressure.

The earnings season may prove to be crunch time for the Stoxx Europe 600 to sustain this year’s 14 percent rally. There are obstacles to overcome with trade jitters heating up again between the U.S. and Europe, Italy raising its budget deficit forecast and the IMF cutting its global growth outlook to the lowest level since the global financial crisis.

In the meantime, Euro Stoxx 50 futures are down 0.1% ahead of the open.

- Watch the pound and U.K. stocks after the European Union are set to reject U.K. Prime Minister Theresa May’s plea for a short Brexit extension, and instead give her a longer delay of up to a year at today’s summit. This is another defeat for May that will leave Brexiteers in her party fuming.

- Watch banks as the European Central Bank’s rate decision comes a day after the International Monetary Fund made cuts to its 2019 growth forecasts, with the outlook for euro-area countries significantly affected. The ECB is said to be in no rush to soften the impact of negative rates on the banking sector. Here’s a decision day guide.

COMMENT:

- “FTSE 100 volatility is all but vanishing and hedge funds are taking bets on the pound off the table in a lull that we don’t believe will last long, said Bloomberg Intelligence analysts Tim Craighead and Laurent Douillet. “The EU will either grant a short Brexit extension to Theresa May, a much longer delay (our likely scenario) or hold fast to this Friday’s exit deadline. The pound should react well on the second and poorly on the third, and groan in annoyance on the first.”

COMPANY NEWS AND M&A:

- Deutsche Boerse to Buy Axioma for About EU820m Equity Value

- Tryg First Quarter Pretax Profit Beats Estimates

- Telepizza Board Has Favorable Opinion on KKR Bid: Filing

- Adevinta Set for Trading Debut After Spinoff From Schibsted

- Volkswagen Is Said Eyeing Big Stake in JAC Motor: Reuters

- Airbus May Start Bribery Settlement Talks By Year-End: Les Echos

- Ghosn Holds Nearly 1 Million Renault Shares, Les Echos Says

- Panalpina Board Proposes No Dividend Be Paid Out in 2019

- Sopra Steria Unit to Acquire A Majority Stake in SAB

- Swedish FSA Looking at Whether Swedbank Misled Authorites: DI

- ECB to Investigate Swedbank’s Estonian Unit, DN Reports

- Carmat to Delay Resumption of Artificial Heart Study

- Takeaway First Quarter Orders +51%

- Pandora Introduces Jewelry Collection Aimed at China, JP Says

- Indonesia Chases Volvo, Renault Investment in Electric Vehicles

- FTC Approves Final Order on Fresenius Medical/NxStage Deal

- Commerzbank Staff Call For Vote to Scupper Deutsche Deal: FT

- Unibail to Sell Tour Majunga in Paris for EU850 Million

- Cepsa Wants to Sell 42% Stake in Medgaz to Naturgy: Cinco Dias

NOTES FROM THE SELL SIDE:

- Citi refocuses its valuation approach within the European auto parts sector, says with revenue growth coming under pressure that cash flow is becoming ever more important. Valeo is downgraded to sell, while broker reiterates buy on Michelin. Continues to like Valeo’s ethos, although skeptical on its ability to sustain current margins considering the pressures faced by its customers. Valeo is lowest-margin supplier and has highest rate of investment, which exposes “mediocre” cash generation. Citi’s 2019 and 2020 Ebit estimates for Valeo are 5% below consensus.

- Within the food industry, the long-held advantages of scale, major brands and mass marketing has “been all but eroded,” but these large-cap companies are starting to fight back, Barclays says in a note. Prefers new overweights Nestle, Danone and overweight-rated AB Foods, with Unilever and Lindt rated new underweight. Says Danone has healthiest portfolio and structural growth of its plant-based products underappreciated, while Nestle still has plenty of scope to unlock value even after strong recent performance. Concerned by Unilever’s margins and lack of room for structural change.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 392.7 (July high); 403.7 (100% Fibo)

- Support at 385.7 (76.4% Fibo); 374.5 (61.8% Fibo)

- RSI: 62.7

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,516 (76.4% Fibo); 3,596 (May high)

- Support at 3,403 (61.8% Fibo); 3,309 (50% Fibo)

- RSI: 63.4

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Aena Upgraded to Buy at Kepler Cheuvreux; PT 180 Euros

- FLSmidth upgraded to overweight at Morgan Stanley; PT 395 Kroner

DOWNGRADES:

- DNA downgraded to hold at SEB Equities; Price Target 21.50 Euros

- EON downgraded to underperform at MainFirst; PT 8.10 Euros

- Epiroc cut to equal-weight at Morgan Stanley; PT 103 Kronor

- Glencore downgraded to sector perform at RBC

- Novartis cut to underweight at Morgan Stanley; PT 80 Francs

- Valeo downgraded to sell at Citi

- Valora downgraded to sell at Baader Helvea; PT 242 Francs

INITIATIONS:

- Alcon rated new hold at Berenberg; PT 55 Francs

- Alcon rated new overweight at Morgan Stanley

- Danone rated new overweight at Barclays; PT 82 Euros

- Intervest Offices rated new hold at ING; PT 26 Euros

- Lindt & Spruengli rated new underweight at Barclays

- Nestle rated new overweight at Barclays; PT 106 Francs

- Nostrum Oil & Gas Resumed at Peel Hunt With Add; PT 1.40 Pounds

- Viafin Service rated new accumulate at Inderes; PT 6.70 Euros

MARKETS:

- MSCI Asia Pacific up 0.4%, Nikkei 225 down 0.7%

- S&P 500 down 0.6%, Dow down 0.7%, Nasdaq down 0.6%

- Euro down 0.02% at $1.1261

- Dollar Index up 0.01% at 97.01

- Yen down 0.02% at 111.16

- Brent up 0.1% at $70.7/bbl, WTI up 0.3% to $64.2/bbl

- LME 3m Copper down 0.1% at $6483.5/MT

- Gold spot down 0.1% at $1303.4/oz

- US 10Yr yield down 1bps at 2.49%

MAIN MACRO DATA (all times CET):

- 8:45am: (FR) Feb. Industrial Production YoY, est. -0.2%, prior 1.7%

- 8:45am: (FR) Feb. Manufacturing Production YoY, est. 1.0%, prior 0.9%

- 8:45am: (FR) Feb. Industrial Production MoM, est. -0.5%, prior 1.3%

- 8:45am: (FR) Feb. Manufacturing Production MoM, est. -0.4%, prior 1.0%

- 10am: (IT) Feb. Industrial Production MoM, est. -0.8%, prior 1.7%

- 10am: (IT) Feb. Industrial Production WDA YoY, est. -1.1%, prior -0.8%

- 10am: (IT) Feb. Industrial Production NSA YoY, prior -0.9%

- 10:30am: (UK) Feb. Visible Trade Balance GBP/Mn, est. £12.876b deficit, prior £13.084b deficit

- 10:30am: (UK) Feb. Trade Balance Non EU GBP/Mn, est. £4.375b deficit, prior £4.977b deficit

- 10:30am: (UK) Feb. Trade Balance, est. £3.789b deficit, prior £3.825b deficit

- 10:30am: (UK) Feb. Industrial Production MoM, est. 0.1%, prior 0.6%

- 10:30am: (UK) Feb. Industrial Production YoY, est. -0.9%, prior -0.9%

- 10:30am: (UK) Feb. Manufacturing Production MoM, est. 0.2%, prior 0.8%

- 10:30am: (UK) Feb. Manufacturing Production YoY, est. -0.6%, prior -1.1%

- 10:30am: (UK) Feb. Construction Output SA MoM, est. -0.4%, prior 2.8%

- 10:30am: (UK) Feb. Construction Output SA YoY, est. 2.3%, prior 1.8%

- 10:30am: (UK) Feb. GDP (MoM), est. 0.0%, prior 0.5%

- 10:30am: (UK) Feb. Monthly GDP 3M/3M Change, est. 0.2%, prior 0.2%

- 10:30am: (UK) Feb. Index of Services MoM, est. 0.1%, prior 0.3%

- 10:30am: (UK) Feb. Index of Services 3M/3M, est. 0.4%, prior 0.5%

- 1:45pm: (EC) April ECB Main Refinancing Rate, est. 0.0%, prior 0.0%

- 1:45pm: (EC) April ECB Marginal Lending Facility, est. 0.25%, prior 0.25%

- 1:45pm: (EC) April ECB Deposit Facility Rate, est. -0.4%, prior -0.4%

--With assistance from Hanna Hoikkala.

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2019 Bloomberg L.P.