JPMorgan Sees `Violent' Markets on Volatility-Liquidity Loop

JPMorgan Sees `Violent' Markets on Volatility-Liquidity Loop

(Bloomberg) -- Marko Kolanovic is blaming a “negative feedback loop between volatility and liquidity” for topsy-turvy markets.

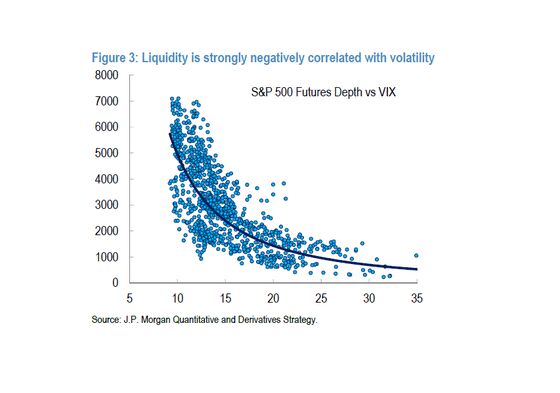

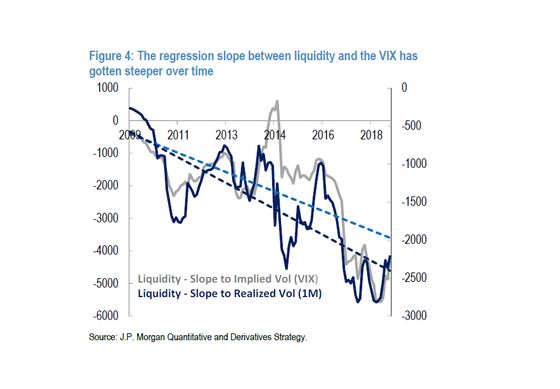

The negative correlation between volatility and liquidity has been getting stronger over time, according to the JPMorgan Chase & Co. global head of macro quantitative and derivatives research. As volatility rises, market depth declines exponentially, exacerbating price moves, he said.

“Why was the Q4 2018 sell-off and subsequent rally so violent?,” Kolanovic wrote in a note last week. “The answer lies in market liquidity.”

A shift from “slower” human market makers, who often rely on valuations, to faster programmatic liquidity that rely on volatility measures to determine risk-taking and position sizing, can strengthen momentum and reduce day-to-day price swings, according to Kolanovic. However, it increases the risk of market disruptions such as that seen in October, he noted.

Volatility has become an increasingly important factor in markets in recent years, with an explosion of products designed to help investors hedge risks or boost exposure to various asset classes. That can leave markets vulnerable to spikes such as that seen in February 2018, when the Cboe Volatility Index jumped to over the 50 level intraday and some products went into meltdown.

During times of high volatility, the VIX starts to dwarf other factors as a driver of market liquidity, according to Kolanovic. Recently up to around 80 percent of liquidity variations were explained by the volatility gauge, he said.

The shift to passive investing from active management, specifically the decline of active value investors, reduces the ability of the market to prevent and recover from large drawdowns, according to the strategist. Active managers would often be stabilizing forces because they might buy into weakness, but fundamentally driven, single-name trading now accounts for only about 10 percent of trading volume, he said.

Investors added $222 million to exchange-traded funds that protect against stock volatility in the past week, pushing assets of funds focused on VIX derivatives to more than $3 billion. The VIX itself is down 48 percent this year to 13.2 as of Monday amid the overall risk-on rally.

“The depletion of market-reversion forces was driven by a decline of value investors as money moved to passive and systematic strategies,” he wrote. “Liquidity has become to a large extent driven by market volatility.”

To contact the reporter on this story: Joanna Ossinger in Singapore at jossinger@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Cormac Mullen, Cecile Gutscher

©2019 Bloomberg L.P.