SocGen's Lapthorne Calls for Credit Short Via Equity Trade

SocGen's Lapthorne Calls for Credit Short Via U.S. Equity Trade

(Bloomberg) -- The best way to trade worryingly high leverage in the U.S. may not be in the credit markets, but in stocks, according to Societe Generale SA.

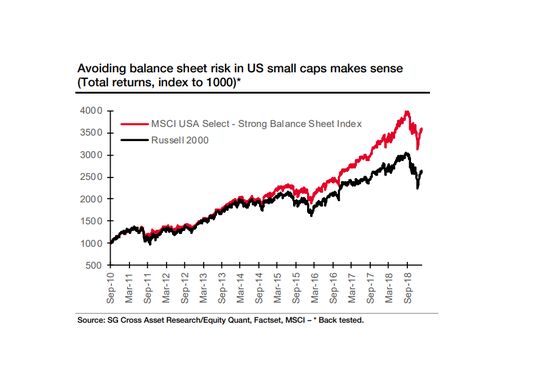

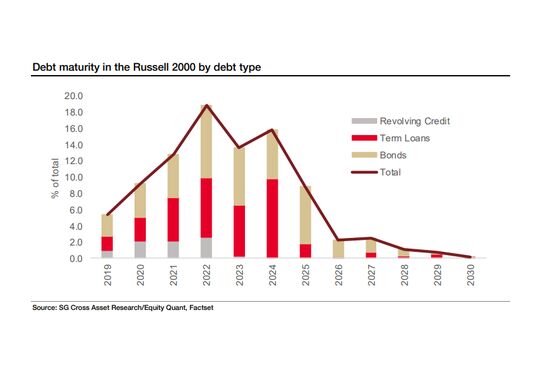

U.S. small-cap stocks are more at risk than larger peers if there’s a corporate credit crunch due to an outsized increase in leverage and relatively short duration of debt, strategists led by the global head of quantitative strategy, Andrew Lapthorne, wrote in a note Thursday. Rather than short credit outright, they recommend betting against a broad gauge of small-cap equities while going long on such stocks with strong balance sheets.

“Shorting credit is expensive” the strategists wrote, saying they “prefer positioning for the ‘short credit’ story via the equity market.” One way to “create a strategy directly exposed to the ‘strong vs weak balance sheet’ story -- one that should outperform if the credit market misbehaves -- is to go long” a gauge of strong-balance-sheet stocks while shorting the broader Russell 2000 index.

SocGen’s recommendation dovetails with that of JPMorgan Chase & Co., where small-cap strategists led by Eduardo Lecubarri maintain a 2019 preference for “stocks that have sold off already, while offering a high free-cash-flow yield, a solid balance sheet and resilient operations,” according to an April 3 note.

Lecubarri’s note added LDC SA to JPMorgan’s pan-European top small-cap picks, while closing positions in stocks like Cancom SE, Wallenstam AB and Petrofac Ltd.

Credit takes center stage in a small-cap recommendation from Gavekal Research as well, where analyst Tan Kai Xian recommended using tinier equities as a bet on a longer U.S. economic cycle, in an April 3 note. He notes that larger companies tend to rely on long-term fixed-rate debt, while their smaller peers are bigger users of floating-rate borrowings.

“Smaller U.S. firms do well in the cycle’s recovery phase, while big companies do better in its twilight phase,” Tan wrote. “If the U.S. really is about to enjoy a longer cycle than seemed likely a few months back, it is fair to assume a continued steepening of the yield curve. Consequently, small caps should do better than large caps in this phase.”

The S&P 500 has risen 15 percent this year through April 4, versus a gain of 16 percent for the Russell 2000.

The SocGen strategists said they considered other methods, including ridding portfolios of highly leveraged stocks or going long the S&P 500 while shorting the Russell 2000, but neither quite satisfied them. The MSCI USA Select Strong Balance Sheet Index allows investors to rotate from existing small-cap exposure, or to create a “credit short” by going long that gauge versus the Russell 2000, they said.

“Deciding when to short credit markets is crucial as the expenses incurred can be significant while waiting for the correction,” the strategists led by Lapthorne wrote. “U.S. small caps appear the most vulnerable, as they have the highest leverage, the lowest interest cover and shortest duration of the riskiest debt,” so “our recommendation is thus to buy the U.S. small caps with the strongest balance sheets.”

To contact the reporter on this story: Joanna Ossinger in Singapore at jossinger@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Andrew Monahan, Ravil Shirodkar

©2019 Bloomberg L.P.