Oil Traders Suffering Dismal Year as Easy Money Deals Vanish

Oil Traders Suffering Dismal Year as Easy Money Deals Vanish

(Bloomberg) -- After years of easy money, many of the world’s biggest oil traders are enduring a brutal new reality.

Traders have been wrong-footed by wild swings in price spreads between oil grades, particularly in the U.S. market. Amid dwindling profits, trading desks are being overhauled, with some firms restructuring their operations and paring budgets designed for better times.

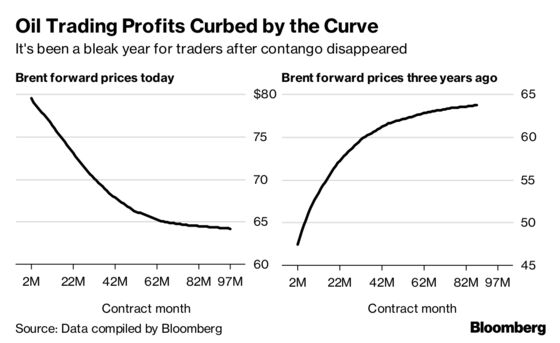

It’s a stark reversal from the long period of big returns that was ushered in by oil’s crash in 2014. Back then, the market moved into a structure called contango, which allowed traders to cash in using a simple carry trade -- filling tanks with crude and profiting by selling futures contracts at higher prices.

“Contango years are golden years for traders and it is difficult if you make that the benchmark,” said Olivier Jakob, managing director of Zug, Switzerland-based consultants Petromatrix GmbH.

The weak results are looming over one of the oil industry’s biggest annual gatherings, the Asia Pacific Petroleum Conference known as APPEC, which kicked off Monday in Singapore.

For most crudes, futures contracts are trading below current prices -- a structure known as backwardation that makes it much more difficult for traders to make money.

“It is an easier job when you have strong contangos,” Jakob said. “It is always more challenging in backwardation.”

Indeed, some of the largest trading houses, many with major operations in the Swiss trading hub of Geneva, have been making big changes amid the shift.

Gunvor Group Ltd., which handles about 2.7 million barrels of crude and products a day, told employees last month it was laying off staff and cutting costs. After deciding to halt a refinery upgrade, CEO Torbjorn Tornqvist said that a “very competitive trading environment” had crimped earnings.

Profit Slump

Gunvor’s 2017 net income sank 49 percent to the lowest in at least eight years, and its head of crude, Jose Orti, is leaving at the end of 2018 for “personal reasons.” Gunvor is also shutting its Bahamas trading office, where Orti is based.

Trafigura Group Ltd., the No. 3 independent oil trader, reshuffled its senior management earlier this year and the company’s only North Sea traders left in the summer.

Another Geneva firm, Socar Trading SA -- the global trading arm of Azerbaijan’s state oil company -- has pulled back from key markets and installed a new chief executive officer, Mariam Almaszade. Shortly after Almaszade took over, Socar Trading shut a new support office in Estonia, and in August, the bulk of its North Sea crude traders left.

Litasco Listing

Meanwhile, Litasco, the Swiss-based trading arm of Russia’s Lukoil PJSC, hired a new CEO in April. Two senior oil traders left around the same time and the head of crude trading was replaced in August, people familiar with the matter said. Although Lukoil had been considering listing Litasco, CEO Vagit Alekperov said in June that a sale or public offering was now unlikely this year.

“2018 hasn’t provided an easy trading environment for oil traders,” said Jean-Francois Lambert, a consultant at Lambert Commodities. Nevertheless, things could be starting to look up, he said, as “the last few months have been slightly more conducive, and certainly so compared to the first quarter.”

Senior executives from two of the top oil-trading houses said Monday that crude could return to $100 a barrel in the next few months. Mercuria Energy Group co-founder Daniel Jaeggi and Trafigura’s co-head of oil trading, Ben Luckock, told delegates at the APPEC conference that U.S. sanctions on Iran will slash supply and send prices higher.

Brent crude, the benchmark for more than half the world’s oil, rose 2.5 percent to $80.77 a barrel at 12:51 p.m. in London, after earlier jumping to the highest level since 2014.

Ripe for Deals

With trading margins still under pressure, top executives are predicting a wave of mergers and acquisitions.

“With interest rates going up, the cost base of our industry is way too high,” Marco Dunand, CEO and another co-founder of Mercuria, said this month. “We expect to see some major consolidation over the next couple of years.”

Mercuria bought the U.S. power and gas business of embattled Noble Group Ltd. in 2017 and bid for its U.S. oil-trading unit, which was snapped up by Vitol Group.

Commodity houses have seen costs mount after adding employees to boost trading volumes amid shrinking margins. At the same time, some are locked into long-term oil-storage contracts that are no longer profitable, while new derivatives-trading rules have increased regulatory and compliance expenses.

“It is not the best environment,” Petromatrix’s Jakob said. “The financing is more timid, the regulations are increasing on the paper side.”

BP, Shell

Even the oil majors are feeling the pinch. U.K. energy giant BP Plc lost money from trading in the second quarter after Permian pipeline bottlenecks caused big swings in U.S. crude prices. Royal Dutch Shell Plc also said quarterly downstream earnings were pulled lower by sliding trading results.

There may be further upheaval to come, with more companies shedding traders as they tighten the reins on costs.

“There is more to be shaken out this year,” said Shaun Smart, vice president for EMEA at Commodity Appointments in Petersfield, southern England. “This could be a bit of a paradigm shift -- the start of a different type of market to trade -- or this year is just a blip. We’ll find that out next year.”

--With assistance from Javier Blas and Anthony DiPaola.

To contact the reporters on this story: Andy Hoffman in Geneva at ahoffman31@bloomberg.net;Laura Hurst in London at lhurst3@bloomberg.net;Catherine Ngai in New York at cngai16@bloomberg.net

To contact the editors responsible for this story: James Herron at jherron9@bloomberg.net, Amanda Jordan, Helen Robertson

©2018 Bloomberg L.P.