Gundlach Is Right. Surging U.S. Bond Yields Are Met With Shrugs

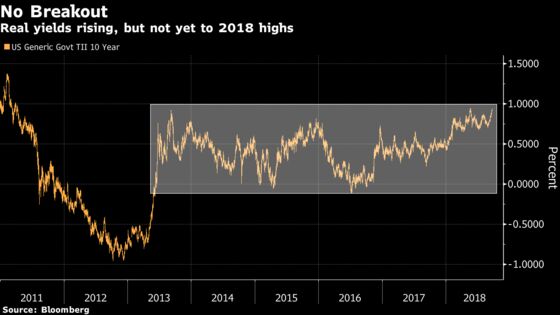

Longer-term inflation-protected Treasury yields are up but haven’t broken out to fresh year-to-date highs.

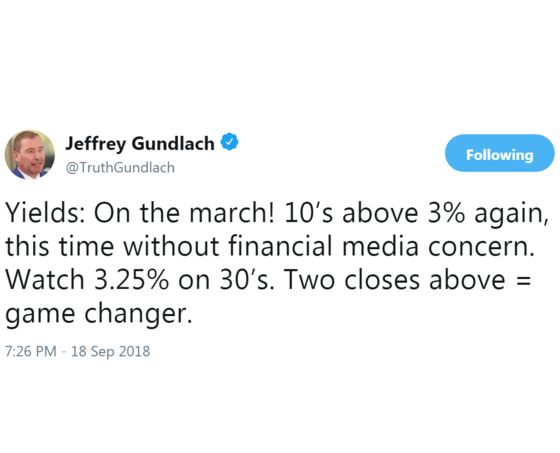

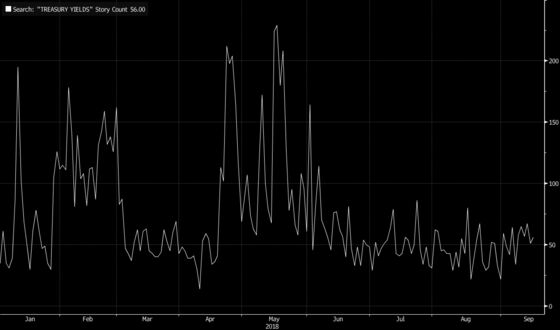

(Bloomberg) -- The selloff in Treasuries that’s taken the 10-year yield above 3 percent isn’t getting enough attention. And DoubleLine CEO Jeffrey Gundlach has noticed.

He’s right -- at least on the first part. References to "Treasury yields" in news articles are dramatically below where they were in April, when the 10-year yield traded above 3 percent for the first time since 2014.

There’s a simple reason no one’s talking about the selloff in the $15 trillion Treasury market: It’s tough to find the negative ramifications across other asset classes. U.S. stocks have been moving in near-tandem with bond yields since the 10-year crossed the 3 percent threshold.

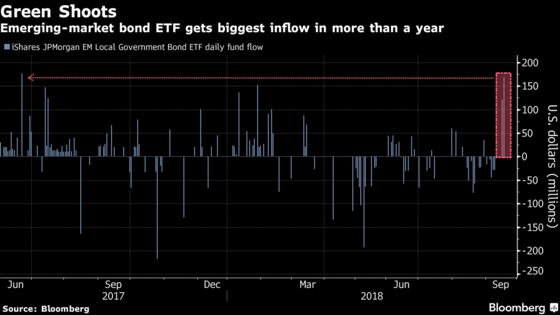

The traditional master-slave relationship in global markets -- soaring U.S. yields undercutting emerging markets -- isn’t on display this week. BlackRock is touting the asset class, and inflows are staging a tentative return.

Case in point: The largest exchange-trade fund tracking emerging-market local currency bonds reeled in $169 million on Tuesday, the most since June 2017, after losing about a quarter of total assets since early April.

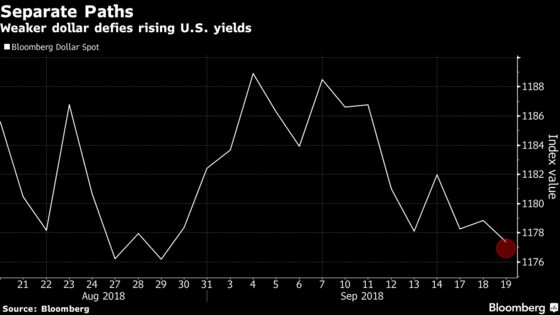

And that’s in part because King Dollar is eating humble pie this week despite the push higher in yields. The Bloomberg Dollar Spot Index is trading at its lowest level in three weeks.

Longer-term inflation-protected Treasury yields are up but haven’t broken out to fresh year-to-date highs, and have been mired in a relatively tight range for five years.

“Ninety-three basis points on 10-year real rates is attractive,” said TD Securities head of global rates strategy Priya Misra, who nailed the top in inflation-protected yields this May. “I don’t think we are at the point where rates can break out to the upside.”

So long as real yields remain well-contained, equity investors can avoid material upward revisions to the rate used to discount future earnings.

Some more global context: The selloff in Treasury bonds has come during a reduction in the perceived risk of turmoil between Italy and the European Union over its budget -- which had previously pushed investors to seek safer options in fixed income. As Italian bond yields have fallen, core rates have risen.

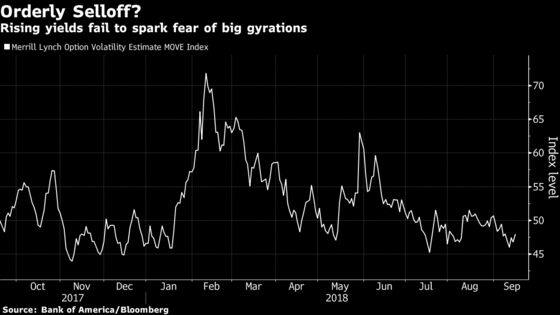

But as Treasury yields have risen, their implied volatility -- as judged by Bank of America’s MOVE Index -- has remained subdued.

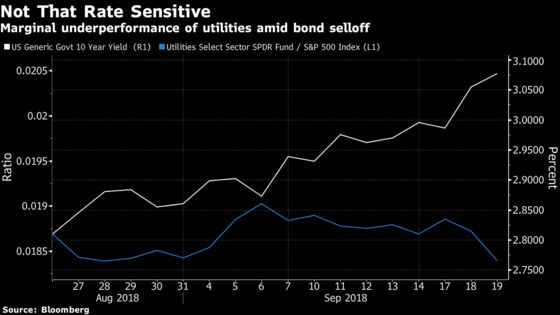

Utilities, an interest rate sensitive sector, haven’t even registered large underperformance amid a roughly 25 basis point rise in the 10-year Treasury yield. This may be a sign that equity investors doubt the increase in risk-free rates will persist.

"Where we are today, is in a period of relative calm as U.S. bond yields probe their highs, and we become accustomed to trade rhetoric and perhaps, blasé about the economic damage it will cause," writes Societe Generale SA’s global strategist Kit Juckes.

--With assistance from Natasha Doff.

To contact the reporters on this story: Luke Kawa in New York at lkawa@bloomberg.net;Sid Verma in London at sverma100@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Dave Liedtka, Brendan Walsh

©2018 Bloomberg L.P.