Lehman-Era Alphabet Soup of Market Products Is Back on the Table

Lehman-Era Alphabet Soup of Market Products Is Back on the Table

(Bloomberg) -- The collapse of Lehman Brothers Holdings Inc. has consigned some financial products, popularized by their acronyms, to the dustbin of history. But investors’ appetite for high-yielding and relatively risk-free securities never went away.

While the financial crisis permanently damaged the reputation of many esoteric, high-risk portions of the credit market, new products, some with more robust structures, have emerged. These days money managers are piling into leveraged loans, via securitized structures known as collateralized-loan obligations, and securities backed by consumer debt rather than mortgages. Even collateralized-debt obligations, blamed by many for triggering the 2008 financial and economic meltdown, are making a comeback.

Meanwhile, money-market indicators, which are meant to warn for signs of funding stress, have been distorted by ever-present central banks and ballooning fiscal spending. Highly-watched measures, such as the gap between the London interbank offered rate and overnight index swaps, used to be strong indicators of dollar funding stress, but dislocations there now appear to reflect structural changes.

Here is a look at what these markets are up to today:

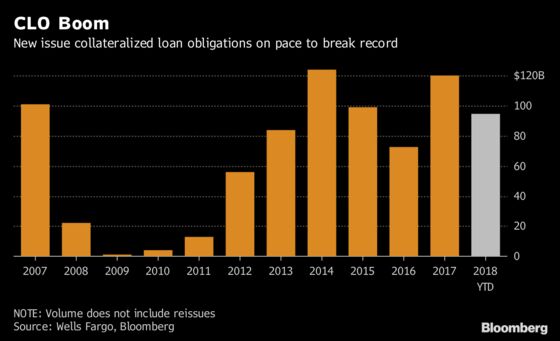

With the Federal Reserve hiking rates, money managers have piled into collateralized loan obligations, which carry a floating rate. That demand has helped lift the size of the U.S. leveraged-loan market to around $1.3 trillion -- rivaling the dollar high-yield bond market. As demand outstripped supply, investors agreed to weaker safeguards and protections on loans to junk-rated companies, according to Moody’s Investors Service. Around 80 percent of leveraged loans are “covenant-lite,” meaning they lack meaningful protections against, for example, the company’s earnings falling to low levels. In 2006-2007, that proportion would have been less than 25 percent, according to Moody’s.

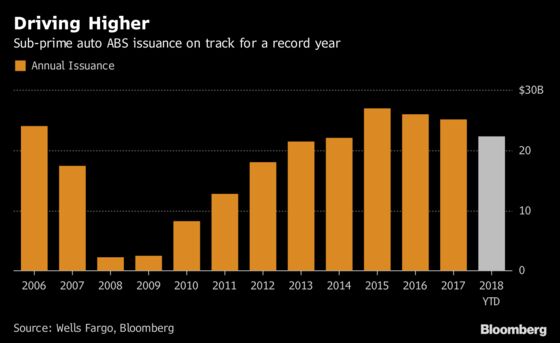

Consumer ABS issuance remains strong, particularly deals backed by auto loans, which saw supply of more than $100 billion last year, the most since 2005, according to information compiled by Bloomberg News and data from Sifma. Meanwhile, subprime auto ABS supply has surpassed its pre-crisis 2007 peak, and saw $25 billion price in 2017. Despite increasing delinquencies, bond investors have faith in the robust structures of subprime-auto bonds and have even shown a willingness to buy the lower-rated tranches.

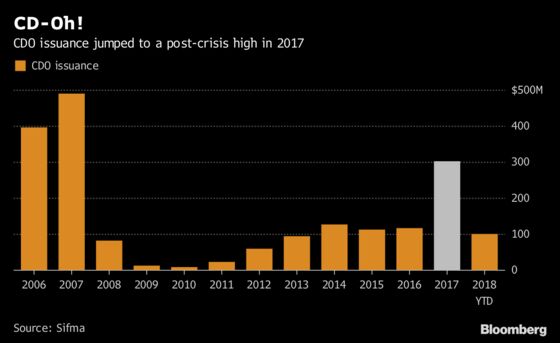

CDO issuance jumped above $303 billion last year, the most since almost $500 billion priced in 2007, according to Sifma data. But CDOs are fundamentally different now; for one thing, post-crisis transactions are typically tied to corporate credit rather than mortgage debt. While the resurgence of complex credit-derivative products, such as synthetic CDOs, has raised a few eyebrows, the structures are more robust and include additional safeguards for investors.

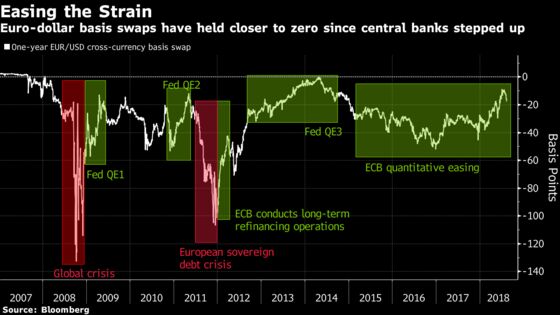

At the same time, global funding markets are still recovering from the disruptions of the crisis. The 2008 turmoil and the subsequent European sovereign debt debacle in 2011 made it more expensive for borrowers to convert their euro-denominated cash flows into dollars as the one-year cross-currency basis swap widened to record levels. Financing costs cheapened when the Federal Reserve stepped in with quantitative easing and opened liquidity swap lines with other central banks. The basis swaps remain close to zero as the Fed is only one year into its balance-sheet unwind and the ECB is still conducting its bond-buying program.

The expansion of central banks’ balance sheets mitigated financial institutions’ need for interbank funding. As a result, the Libor-OIS spread collapsed, dragging U.S. two-year swap spreads with it. This muted the market’s reaction to other tempests such as the European sovereign debt crisis and U.S. money-market reforms. When Libor-OIS ballooned in April to the widest level in more than eight years, market participants didn’t panic. The spread, which investors once considered a more complete picture of how the market is viewing credit conditions, is now driven by more technical factors, such as money-market fund flows, Treasury bill supply, Fed policy expectations and U.S. tax-related concerns surrounding repatriation.

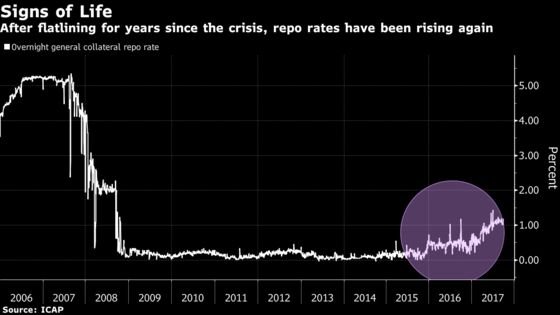

After flat-lining in the wake of the financial crisis, the market for repurchase agreements is showing signs of life again. New regulations designed to shore up financial institutions’ capital buffers spurred demand for high-quality liquid assets, such as Treasury repos, and pushed short-term funding rates to zero. The combination of the Fed’s interest rate hikes, and Treasury’s rising debt issuance to finance soaring deficits and the balance sheet unwind has pushed overnight repo rates to around 2 percent.

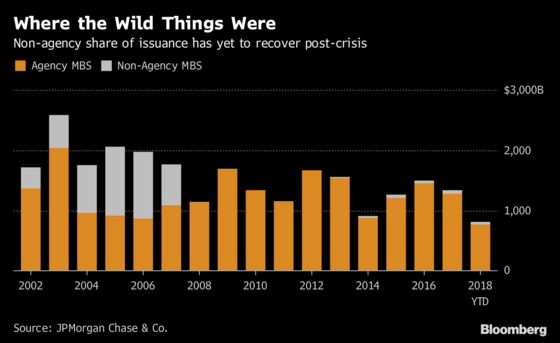

The collapse in credit standards seen during the housing boom led to the spectacular rise and fall of the private-label MBS sector. At its height in 2005 and 2006 such debt accounted for higher mortgage origination than Fannie Mae and Freddie Mac combined, but the housing correction put that to an end. Since 2007, private-label MBS has averaged less than three percent of annual gross supply.

--With assistance from James Crombie.

To contact the reporters on this story: Christopher Maloney in New York at cmaloney16@bloomberg.net;Alexandra Harris in New York at aharris48@bloomberg.net;Adam Tempkin in New York at atempkin2@bloomberg.net

To contact the editors responsible for this story: Christopher DeReza at cdereza1@bloomberg.net, Jenny Paris

©2018 Bloomberg L.P.