The Philippine Peso Needs a Break. It May Be About to Get One

Embattled Philippine Peso Looks to Remittances to Restrain Slide

(Bloomberg) -- The embattled Philippine peso needs a break and it may soon get one.

More than 10 million overseas Filipinos are preparing to send record amounts of money home for the Christmas and New Year holidays -- a period when remittances pick up -- with analysts from MUFG Bank Ltd. and Standard Chartered Plc saying those funds will help ease pressure on the currency.

The peso, which this month sank to a 2005-low of 54.14 per dollar, strengthened in the fourth quarter last year and in every December in the past four years. Since 2009, the highest monthly remittances value was in every December and last year’s $2.7 billion inflow in the month was the largest ever, according to central bank data.

“The peso may see some support due to the dollar strength seen losing momentum toward the year-end and a seasonal pickup in remittances,” said Teppei Ino, an analyst at MUFG Bank in Singapore. The bank forecast the currency to trade at 53.75 per dollar by the end of the year, compared with the Friday close of 53.97.

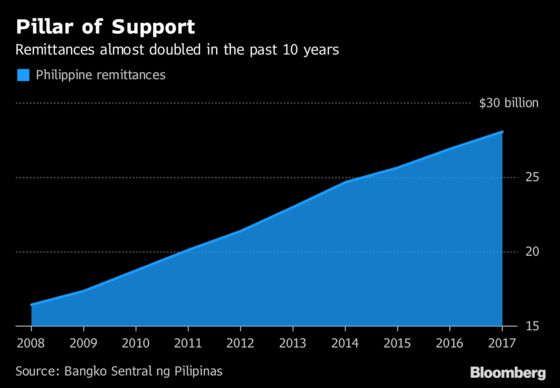

The peso has been caught in the maelstrom engulfing emerging-market assets with the currency among the biggest losers in Asia this year, dropping more than 7 percent. Remittances, which totaled $28 billion last year, are the nation’s largest source of foreign exchange after exports.

“Given the bearish emerging-markets environment and near-term external risks around trade tariffs, we are neutral on the peso, but remain relatively optimistic on the currency’s prospects in coming months,” Goldman Sachs Group Inc. analysts Jonathan Sequeira, Danny Suwanapruti and Andrew Tilton said in a Sept. 10 note.

They said the peso is still about 10 percent undervalued relative to its fair value of 49 per dollar, according to the bank’s GSDEER model, which takes productivity and terms of trade differentials into account.

Remittances probably rose 5.1 percent in July from a year earlier, according to the median estimate in a Bloomberg survey of economists, ahead of data due Monday. Growth was 2.7 percent in the first six months of the year.

Brief Rally?

Any relief rally in the peso could be brief as investors remain cautious over the nation’s worsening current-account deficit. The shortfall was $3.1 billion in the first half of the year, matching the central bank’s forecast for the full year.

“The nation’s current-account deficit is unlikely to turn to a surplus anytime soon and that’s making it hard to expect an appreciation trend for the peso,” Ino said.

The prospect for more interest-rate increases by the central bank could also support the currency. ING Groep NV and Capital Economics Ltd. were among those predicting a rate hike this month. Bangko Sentral ng Pilipinas has delivered 100 basis-points of rate increases since May, including a 50 basis-point hike just in August.

The central bank plans to use some of those remittances to gradually bolster its foreign-exchange reserves, Deputy Governor Diwa Guinigundo has said.

“We expect some recovery in the peso ahead of year-end, driven by a seasonal pick-up in remittances,” said Divya Devesh, head of Asean and South Asia FX research at Standard Chartered in Singapore. “Monetary policy has also turned more supportive. Any recovery is only likely to be temporary.”

Standard Chartered expects the peso to recover to 53 per dollar at year-end.

Below are key Asian economic data and events due next week:

- Monday, Sept. 17: Indonesia trade balance, Philippine overseas workers remittances, Singapore NODX

- Tuesday, Sept. 18: RBA minutes and Australia 2Q house price index

- Wednesday, Sept. 19: Bank of Thailand rate decision, RBA’s Kent speaks, New Zealand 3Q Westpac consumer confidence and 2Q BoP current-account balance, BOJ rate decision and Japan trade balance, Philippine BoP overall, Malaysia CPI

- Thursday, Sept. 20: New Zealand 2Q GDP

- Friday, Set. 21: New Zealand credit card spending, Japan CPI and Nikkei manufacturing PMI, South Korea PPI, Thailand customs trade balance

--With assistance from David Finnerty and Michael J. Munoz.

To contact the reporters on this story: Karl Lester M. Yap in Manila at kyap5@bloomberg.net;Yumi Teso in Bangkok at yteso1@bloomberg.net

To contact the editors responsible for this story: Tomoko Yamazaki at tyamazaki@bloomberg.net, ;Nasreen Seria at nseria@bloomberg.net, Karl Lester M. Yap

©2018 Bloomberg L.P.