Low Bond Volatility Creates Trove of Cheap Bets

Low Bond Volatility Creates Trove of Cheap Bets

(Bloomberg Opinion) -- The Federal Reserve is raising interest rates, and that’s going to increase volatility. Or at least that was the nearly unanimous view of investors worldwide heading into 2018.

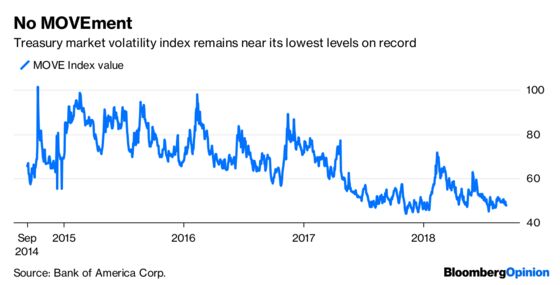

But aside from “volmageddon” in early February, that simply hasn’t been the case. Instead, the stock market’s fear index (formally the Chicago Board Options Exchange Volatility Index) is firmly below its five-year average. Interest rates are even quieter, with Bank of America Corp.’s MOVE index, which tracks price swings on U.S. Treasury options, not far from its all-time low set 10 months ago. The benchmark 10-year yield is still on track for its quietest quarter since 1965.

This is a perfectly fine development for fixed-income investors who are in it for the long haul and content with clipping some of the highest Treasury coupons in the post-crisis era. But for more short-term bond traders, the trend must be maddening. Look at the chart of the 10-year yield over the past five months. The best thing you could have done was simply play the range: Buy the debt as it approached 3 percent and sell once it got close to 2.8 percent, over and over again.

Sovereign debt markets aren’t even offering interesting wagers anymore. Yes, Bill Gross at Janus Henderson Group lost big earlier this year by betting on a convergence in the spread between U.S. and German 10-year yields. Wonder why you haven’t heard much about his unconstrained fund lately? Because the 60-day volatility of that spread is the lowest in at least a decade, according to BMO Capital Markets, and his fund is grinding higher as a result.

In this environment of depressed macro volatility, then, an article from Bloomberg News’s Edward Bolingbroke was eye-catching last week. It said that a Treasury options trade initiated just before the latest U.S. payrolls data were released netted a $10 million profit.

To read the exact mechanics of the trade, click here. But the crux of the wager, which involved paying nearly $2.5 million up front, was for 10-year Treasuries to swiftly sell off for just one day. Considering that it had been more than a month since the yield rose by more than four basis points, there was no guarantee that a jobs report would shake the market enough for the position to make money. But it did, with the 10-year yield climbing almost seven basis points, the most since May.

That mystery options buyer was BlackRock Inc.’s fixed-income group, led by Rick Rieder, according to a person familiar with the trade, who spoke on the condition of anonymity because the transaction was private.

Knowing that, the trade makes a lot of sense (to be fair, it also makes the $10 million seem small in comparison to the firm’s $6.3 trillion in assets). With so many fixed-income portfolios across BlackRock, a swift increase in yields would have proved costly. The put options on 10-year futures, then, served as a near-perfect hedge if that scenario played out.

As I wrote last week, part of the reason for the sudden surge in yields was that strategists were already setting the stage for disappointing August jobs numbers, noting that they had missed forecasts almost every year over the past two decades. That most likely created a skewed environment in which a higher-than-expected increase in payrolls, or stronger wage growth, would move the market more than if the figures trailed estimates. And yet the put options were priced cheap — it would only take yields increasing by a basis point or two, to about 2.9 percent, for the wager to break even.

Still, even with the jolt higher, the 10-year yield hasn’t cracked 3 percent, remaining within its tight quarterly range. The latest read on U.S. inflation, Thursday’s consumer price index data for August, could provide the next catalyst higher or more firmly establish the range.

Whether other investors try to mimic the trade remains to be seen. But it’s telling that one of the only ways for bond traders to profit from volatility at the moment is by betting on sharp moves that last for as little as a day. Indeed, the MOVE index rose on Sept. 7 only to tumble the next session to a one-month low.

All the while, it’s worth remembering that hedge funds and other large speculators have a near-record short position in 10-year Treasury futures, according to Commodity Futures Trading Commission data. And despite all the talk of a short squeeze, they’ve been hesitant to exit their positions.

These fleeting moments of volatility seem destined to continue as long as the Fed is gradually raising interest rates. The biggest question is when officials will decide to slow their quarterly pace. Rieder said on Twitter after the jobs data that he expects hikes later this month, in December, and a couple of times in 2019, “although a pause is quite possible too.”

When signs emerge that a shift is afoot, price swings should get larger and last longer, with options becoming more expensive. For now, betting and hedging are cheap, but the windows are as narrow as ever.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2018 Bloomberg L.P.