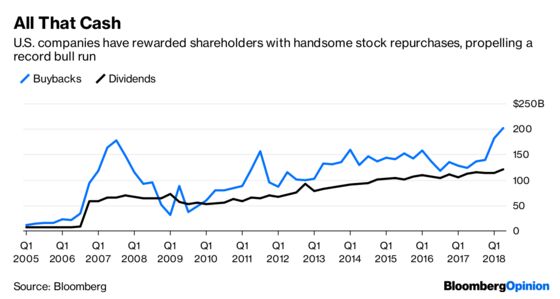

(Bloomberg Opinion) -- Companies returning cash to shareholders have helped propel the U.S. stock market to a record bull run this year. In China, investors take fright when their firms do the same.

This year, more than 700 Chinese firms, or about 20 percent of actively traded stocks, have announced plans to spend money on their own shares. The 24 billion yuan ($3.5 billion) shelled out so far is just shy of the past three years combined. Yet the bear market has only deepened.

In theory, a buyback announcement is a sign of stable cash flow, good corporate governance and more repurchases to come. Yet the Shanghai Composite Index is at a two-and-a-half-year low, and Chinese investors flee when they hear the word.

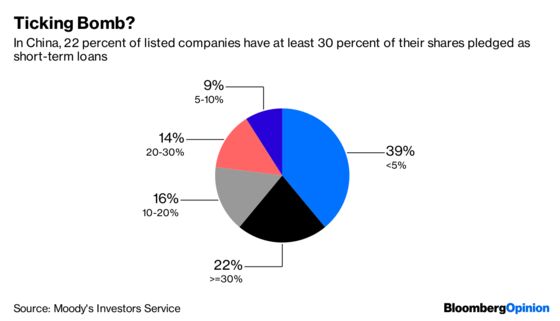

The reason is the volume of shares that have been pledged for loans. In China, major shareholders routinely use their stocks as collateral to secure short-term bank financing. These loans are more common among privately controlled enterprises, which have weak access to bank credit. In the first half, 22 percent of listed companies pledged at least 30 percent of their shares, a 6 percentage point increase from two years earlier.

After this year’s declines, many borrowers are close to facing margin calls. Imagine a Shenzhen-listed company that took out a 400,000 yuan loan at the beginning of the year using 1 million yuan worth of its shares as collateral. The Shenzhen Composite Index, home to more non-state companies than Shanghai, has slumped more than 26 percent this year. This would have raised the loan-to-value ratio to 54 percent, dangerously close to the 60 percent maximum allowed by the government.

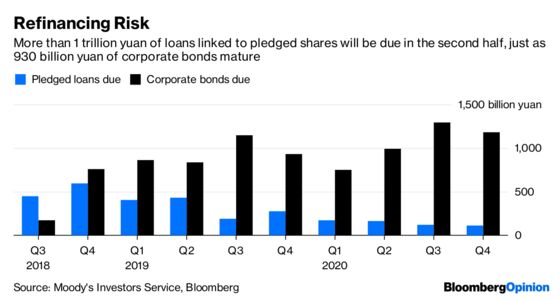

An easy and obvious solution is to prop up the company’s shares with buybacks. In contrast to their U.S. counterparts, Chinese investors are right to be wary. In the second half, a staggering 1 trillion yuan of share-pledged loans will be due. A similar amount of corporate bonds will need to be refinanced, forcing these companies to compete for funding.

Even for firms that aren’t in financial distress, cash rewards can’t disguise weak operations. Midea Group Co.’s 4 billion yuan buyback plan is China’s biggest this year. But since handing out 1.8 billion yuan to shareholders, the electronic appliance maker’s stock has fallen a further 16 percent. Investors understand that Midea must scale back its global ambitions as political tensions check China Inc.’s overseas acquisitions. The Shenzhen-listed company expects only single-digit sales growth this year.

China’s idiosyncratic investment environment often defies the conventional logic of global stock markets. This is just one more example. Foreign investors considering whether it’s time to start bottom-fishing should take note.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2018 Bloomberg L.P.