Aiming at Putin With Sanctions, U.S. May Hit Emerging World

Swinging at Putin With Sanctions, U.S. May Whack Emerging World

(Bloomberg) -- If U.S. sanctions flip Russia to basket case from haven, a fresh stampede from emerging markets could be in the cards, according to some investors and analysts.

On Thursday, Russian officials in Moscow basked in the glow of their balance sheet and the central bank chief gave a speech at the International Monetary Fund in Washington on her successful experience managing past crises. Meanwhile, government bonds and the ruble breached the lowest levels in more than two years.

What was scaring investors was happening down the street from the IMF lecture, in a Senate hearing where legislators were debating new sanctions on Russia. One of the proposals under consideration has been dubbed the “bill from hell,” in part because it includes a ban on buying new sovereign debt.

“Given the near-crisis situation in emerging markets, putting sanctions on the only market where until recently investors could hide would trigger massive contagion risk,” said Elina Ribakova, a fellow at the Bruegel think tank in Brussels and former EMEA research head at Deutsche Bank AG.

Banning new debt purchases by U.S. investors won’t have much of an impact on Russia’s ability to finance itself, since its budget is in surplus and the central bank has plenty of cash to help out if needed. What worries Ribakova and others is the impact the fall of an erstwhile safe harbor could do to what’s left of the confidence across emerging markets.

“It’s an unpleasant situation for portfolio managers because there’s not really anywhere to run to when you have a developing market mandate,” said Vladimir Tikhomirov, an economist with the BCS brokerage in Moscow.

It’s unclear whether the bipartisan proposal forbidding Americans from holding new Russian sovereign debt will even be adopted. But with U.S. midterms approaching, the threat of tougher penalties to punish Moscow for alleged elections meddling has grown, forcing investors to reassess one of their favored local-currency overweight positions.

Read More: DETER or ‘Bill From Hell’? Traders Unpick Russian Sanctions Web

Since the U.S. imposed its toughest round of sanctions to date in April, foreign investors pruned their holdings of local debt from a record high of 34.5 percent to about 26 percent to 27 percent, according to Konstantin Vyshkovsky, the head of the Russian Finance Ministry’s debt department.

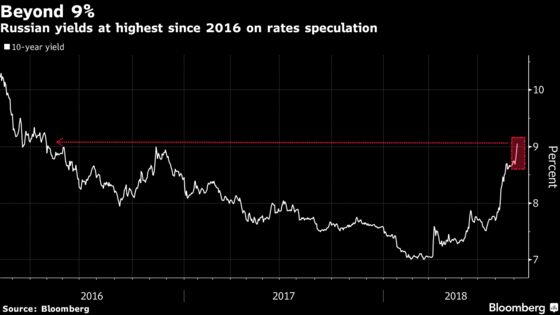

In the first two months of the year, Russia’s local-currency bonds handed investors the second-best return in emerging markets. After the April penalties, they’ve brought a 22 percent loss, the worst result after Argentina, Turkey and South Africa. Yields on Russia’s 10-year local bonds jumped a half percentage point last week, the biggest increase since the 2016 oil slump.

Ruble Beyond 70

"It is difficult for the market to distinguish between idiosyncratic risk and a more broad-based sell-off,” said Anders Faergemann, a fund manager at Pinebridge Investments Europe Ltd. in London, which oversees $87 billion and is underweight on Russia. “So you cannot rule out increased volatility on the back of further Russia sanctions."

The ruble extended its slide on Monday, losing 0.5 percent to 70.26 per dollar, set for its weakest since March 2016. Yields on 10-year local bonds climbed for a fifth day, adding 10 basis points to 9.33 percent, the highest level in more than two years, amid speculation a central-bank rate increase may be in play for the first time since 2014.

That’s all despite the country’s current-account surplus, and the fifth-biggest real return for its asset class. The Bank of Russia’s foreign cash pile is near the largest in four years. Oil, Russia’s main export earner, is just a few dollars off the highest point since 2014.

At an investment conference in Moscow, Vyshkovsky said the declines should only make traders keener.

“Based on fundamentals, Russian sovereign risk is still extremely attractive for investors,” he said. “They’d be hard-pushed to find this kind of yield versus risk anywhere else.”

--With assistance from Gregory L. White and Alec D.B. McCabe.

To contact the reporters on this story: Olga Tanas in Moscow at otanas@bloomberg.net;Anna Andrianova in Moscow at aandrianova@bloomberg.net;Alexandra Stratton in New York at astratton4@bloomberg.net

To contact the editors responsible for this story: Gregory L. White at gwhite64@bloomberg.net, ;Dana El Baltaji at delbaltaji@bloomberg.net, ;Rita Nazareth at rnazareth@bloomberg.net, Alex Nicholson, Paul Abelsky

©2018 Bloomberg L.P.