Smart Beta ETFs Take on the $3.8 Trillion Municipal Bond Market

Smart Beta ETFs Take on the $3.8 Trillion Municipal Bond Market

(Bloomberg) -- First smart beta investing took stocks by storm. Then it moved to bonds. Now it’s making its way to the $3.8 trillion market for U.S. municipal debt.

Columbia Threadneedle Investments, known for its municipal-bond mutual funds, has filed for an exchange-traded fund called the Columbia Multi-Sector Municipal Income ETF, which will seek to replicate the performance of a muni market index with a “rules-based” and “strategic beta” approach, according to a May filing with the U.S. Securities and Exchange Commission.

Once it starts trading, it’ll be Columbia’s first municipal bond ETF and likely one of the first smart beta funds in the muni market. Smart beta is a strategy that aims to give investors more targeted exposure by building indexes around themes, called factors, such as momentum or value.

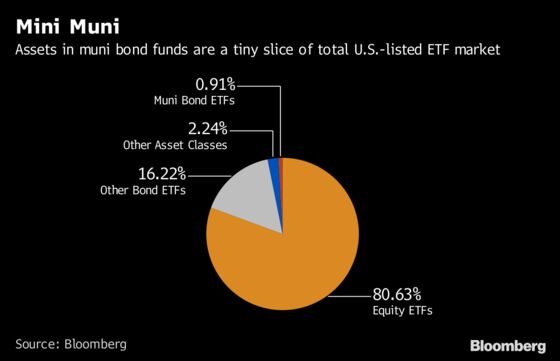

ETFs haven’t made deep inroads in the municipal-bond market like they have in other asset classes, with just over 40 muni funds trading. Still, Columbia found in a survey of more than 100 financial advisers that over half would consider buying a smart beta municipal-bond ETF for clients.

The results are “encouraging,” Marc Zeitoun, head of strategic beta at Columbia Threadneedle, said in an interview. He estimates the shift to benchmarking and passive investing in municipals is about six years behind the equity market.

“This is a trend that will likely occur in the municipal world,” Zeitoun said. “It’s happening in every other asset class.”

Making Munis Smart

Muni ETFs typically use traditional passive investing strategies. For example, BlackRock Inc.’s $10 billion iShares National Muni Bond ETF, known by the ticker MUB, follows the performance of a market-value weighted index, meaning it carries high exposures to the states and sectors with the largest amounts of debt outstanding, like California and New York.

The Columbia fund would take a different approach, targeting debt market factors such as yield, quality, maturity, liquidity and interest rate sensitivity, according to the filing. The ETF also would establish “rules” for what it won’t buy, like California bonds, which have gotten increasingly expensive as people look to shield their income from taxes.

Similarly, while the fund will have some exposure to junk-rated munis, it’s taking a careful approach to those securities. The ETF won’t have tobacco bonds as part of its high-yield holdings because they risk default if Americans keep quitting smoking. And it won’t buy notes sold by bankrupt Puerto Rico or other U.S. territories that are all facing high debt levels.

About 45 percent of the fund will be in “core” revenue bonds that are rated Aa3 or lower, 20 percent will be in health-care municipals rated Aa2 or lower, 15 percent will be in revenue bonds rated Aa2 or higher, 10 percent will be in general-obligation bonds rated Aa3 or higher and another 10 percent will be in high-yield municipals, according to the filing says. Each sector carries different maturity requirements.

Indexing Catches On

Catherine Stienstra, head of municipal bond investments at Columbia, is listed as the lead portfolio manager for the Columbia Multi-Sector Municipal Income ETF.

The high exposure to revenue bonds jibes with a widespread preference among municipal-bond investors for debt backed by a revenue stream as opposed to a promise to pay, known as general-obligation bonds. This comes after Detroit’s bankruptcy imposed losses on general-obligation bondholders, eroding the value of a pledge once considered sacrosanct.

Indexing has been slow to catch on in the municipal market because investors believe it’s difficult to navigate and therefore are willing to pay for actively-managed portfolios, said Todd Rosenbluth, director of ETF and mutual fund research at CFRA Research. The Columbia fund could be appealing because its smart beta approach would screen for investments based on characteristics that active managers use, he said.

Evolutionary ETFs

“It’s a great marriage of what’s working in both the active world and in the index world,” Rosenbluth said.

One concern financial advisers have surrounding smart beta fixed-income funds is the cost, Columbia found in its survey. The ETF filing does not yet disclose the fund’s proposed fees. Rosenbluth said the costs will likely be cheaper than actively-managed alternatives. He expects smart beta to catch on in the municipal market -- just like equities and taxable fixed-income products -- especially if the Columbia fund can gather assets quickly.

“It’s evolutionary that we see this happening in the muni bond ETF space,” he said.

To contact the reporters on this story: Amanda Albright in New York at aalbright4@bloomberg.net;Carolina Wilson in New York City at cwilson166@bloomberg.net

To contact the editors responsible for this story: Courtney Dentch at cdentch1@bloomberg.net, Eric J. Weiner, Michael B. Marois

©2018 Bloomberg L.P.