A PGA Golf Course Is Stuck Between Creditors and the Argentine Crisis

A PGA Golf Course Is Stuck Between Creditors and the Argentine Crisis

(Bloomberg) -- The Canuelas Golf Club is spread out on 178 acres of pristine pampas grassland on the western outskirts of Buenos Aires. Inaugurated in 2014, the club plays host to the Latin American PGA Tour and is the pride and joy of its owner, the corporate titan Aldo Navilli.

But the club has now drawn the attention of another set of investors as well: Creditors including ING, Rabobank and the World Bank’s International Finance arm. They want Navilli to sell the club to help make good on the $1.1 billion of debt that his food conglomerate, Molino Canuelas SACIFIA, fell behind on as the Argentine crisis drove the peso down, pushed interest rates up and throttled the economy.

Navilli is balking at the proposal and is threatening to file for bankruptcy, which would force the banks to sharply write down the value of the debt, if they don’t agree to a more manageable haircut, according to people with knowledge of the talks. “You guys have a problem, not me,” Navilli is said to have told two of the bankers at a recent tense meeting.

All across corporate Argentina, victims of the four-month-old crisis are piling up fast. For many, the problem is the same one that Molino Canuelas faces: Debts are owed in dollars while revenue is mainly received in devalued pesos.

This mismatch upended expansion plans at Telecom Argentina SA. Foreign bond investors have shown no interest in buying the debt that the phone company has been trying to sell to finance the expansion. In fact, only one bond has been issued by an Argentine company in overseas markets in the past four months.

Several major asset sales, including a billion-dollar deal planned by oil giant YPF SA, have also been put on ice in recent weeks. All of which is only adding to the economic slump that has put Argentina at the center of the emerging-markets meltdown.

"The Argentine economy is paralyzed," said former central bank President Martin Redrado. With the peso in free-fall and markets seizing up, it’s hard for investors to assign prices to assets, he said. “And it’s very difficult to negotiate deals when the two sides have no price information. There’s no way to reach a deal.”

Free-Market Push

President Mauricio Macri’s Argentina wasn’t supposed to look like this. And yet almost three years into his administration’s free-market push, a historic drought hurting farm exports coupled with nagging fiscal and inflation problems have fueled a more than 50 percent selloff in the peso.

The central bank raised its benchmark interest rate to a world-high 60 percent last month, yields on the government’s dollar bonds have soared to more than 7 percentage points above U.S. Treasuries, hovering near the highest level since Macri took office, and the Merval stock index has plunged to the lowest levels since 2013.

Macri’s economic aides, struggling to contain the crisis, have traveled to Washington to negotiate a faster disbursement of the $50 billion emergency loan the country received from the International Monetary Fund back in June.

Canuelas was one of several companies that sought to take advantage of the momentum that followed wins for Macri’s party in congressional midterm elections in October, aiming to raise more than $300 million in an initial public offering later this year.

Don Aldo

Half of the shares were going to be offered by the company and the rest by shareholders and members of the controlling Navilli family, including the patriarch "Don Aldo," as he likes to sign regulatory filings. The deal has been shelved amid the market volatility, the company said.

Navilli declined to comment on the recent negotiations. A company spokeswoman said that a port he owns on the Parana river, valued at around $70 million, could be given as collateral to secure future repayment. The company may also sell land and empty storage locations received from Cargill SA in a 2014 deal. Navilli will do everything he can to hold on to his golf course, the representative said. Lazard Ltd., which is handling the restructuring for the company, declined to comment.

Telecom Argentina, the country’s second-largest company by market capitalization, hasn’t been able to sell $1 billion in bonds it was hoping to get to expand in Paraguay, Uruguay and Bolivia. Telecom’s revenue in pesos is so weak in dollar terms that the company will be happy to keep up with its capital expenditure needs in Argentina and will have to shelve its plans to expand regionally, according to a company official, who declined to be named discussing internal company strategy.

“The company decided not to sell the bond because of market volatility, but this won’t affect the $5 billion investment plan Telecom has for the 2018 to 2021 period given the strong financial situation the company has," the company said in a statement. “The projects could become delayed but never canceled. Investment plans at our operations in Paraguay and Uruguay remain as usual.”

Shelved Deals

Telecom Argentina isn’t the only one shelving deals. Another $5 billion of bond sales expected to happen before March 2019 are now in doubt. YPF had mandated Citigroup Inc. to sell its 70 percent stake natural gas distributor Metrogas SA, but chose to pause the sale right after it opened the data room for bidders, according to people with knowledge of the matter. YPF has told the Argentine gas regulator that the deal won’t be completed until the exchange rate stabilizes.

A representative for YPF declined to comment.

At least $1.5 billion in equity sales by Argentine companies are also waiting for better times — including two deals that were postponed on the day of their pricing: Bioceres SA and gas distributor Distribuidora de Gas del Centro SA. Other companies that had aimed to sell shares this year include Telefonica SA, which sought to spin sell a stake in its Argentina unit, energy companies Genneia SA and Desarrolladora Energetica SA, real estate developer TGLT SA and Banco Hipotecario SA.

The sale of Prisma Medios de Pagos SA, the local operator of Visa, has been postponed to as late as 2021. A consortium of banks was selling the asset following an order by the local regulator that initially gave the divestment a September deadline. The seller has frozen the process after only one bidder submitted a $1.2 billion offer, about half of what the sellers had originally hoped for, according to people with knowledge of the deal.

A representative for Goldman Sachs Group Inc., which manages the deal for the consortium, declined to comment.

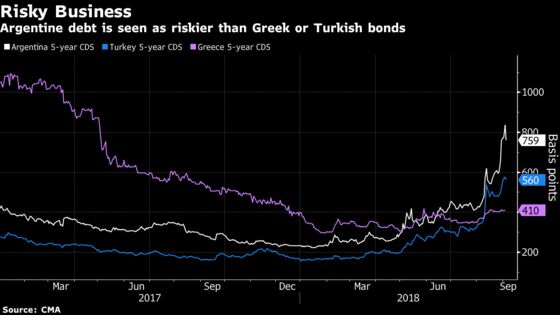

Deals will resurface once investors become more realistic about Argentine risk, Redrado said. The perceived risk of Argentina’s government defaulting jumped to levels exceeding that of Turkish or Greek sovereign debt, according to credit default swaps data from CMA.

The country’s companies are not as indebted as their peers in the region, taking off some of the stress in the current situation. Argentina only returned to global debt capital markets two years ago when the government settled a 15-year-old default with holdout creditors.

“We’re starting to see bargain prices in some cases, for opportunistic buyers,” said Daniel Marx, a veteran negotiator for Argentina with the IMF and now head of consulting firm Quantum Finanzas. “It’s only for those willing to stomach the risk and consider a fearless bet. Argentina is still very difficult.”

To contact the reporters on this story: Pablo Gonzalez in Buenos Aires at pgonzalez49@bloomberg.net;Carolina Millan in Buenos Aires at cmillanronch@bloomberg.net

To contact the editors responsible for this story: David Papadopoulos at papadopoulos@bloomberg.net;Nikolaj Gammeltoft at ngammeltoft@bloomberg.net;Courtney Dentch at cdentch1@bloomberg.net

©2018 Bloomberg L.P.