Credit Derivatives Dethroned by ETFs as Managers Fret Downturn

Credit Derivatives Dethroned by ETFs as Managers Fret Downturn

(Bloomberg) -- Battle-ready investors on the prowl to hedge a looming reversal in the global debt cycle are embracing weapons familiar to Mom and Pop -- and falling out of love with complex derivatives.

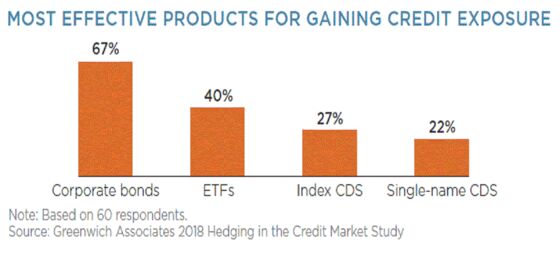

For hedge funds and asset managers, the preferred way to shield credit risks is now the humble exchange-traded bond fund, according to a survey of 60 managers from Greenwich Associates published this week.

ETFs edged out credit-default swaps -- at the single-name and index level -- and were second only to corporate bonds themselves as a way for professionals to access fixed income.

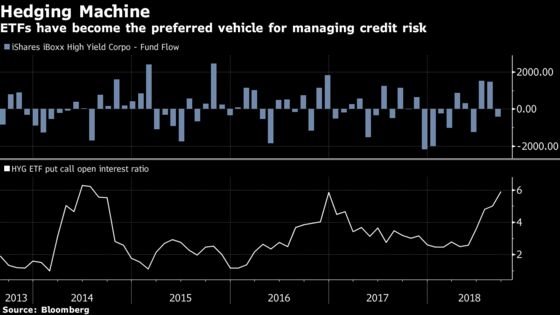

Institutional investors are rubbing shoulders alongside the retail crowd in what has swelled to become a $634 billion market in the U.S. alone.

The principal advantage of ETFs over credit-default swaps is their ever-increasing liquidity, giving credit-default indexes a run for their money, even though trading in the latter has also boomed this year, at the expense of trading in cash bonds.

Sure, passive products are an imperfect hedge because they tend to be broader than swap indexes and single-name CDS, but respondents to the Greenwich survey can’t get enough of them.

“Credit market participants have been forced to make a trade-off between liquidity and specificity, and they’re choosing liquidity,” according to Ken Monahan, senior analyst on the market structure and technology team at Greenwich and author of the report.

It’s the theme du jour. Angst over “vanishing” liquidity was the chief concern expressed by credit buyers in Europe in Bank of America Corp.’s client survey last month.

Passive Preference

The largest corporate bonds funds -- like the $33.6 billion iShares iBoxx $ Investment Grade Corporate Bond ETF, or LQD -- have become bellwethers for fixed-income markets. LQD trades around 5.6 million shares a day, about half of its high-yield cousin, HYG, which trades 10.3 million shares a session, and has the highest open interest of any U.S-listed fixed-income ETF.

“At only $17 billion, HYG is NOT the high-yield market, but with a lot of option activity on HYG, it has become the market for high-yield volatility selling,” according to a recent note from Peter Tchir, head of macro strategy at Academy Securities Inc.

After corporate bonds and ETFs, the most popular ways of gaining credit exposure are through indexes of credit-default swaps such as Markit’s CDX indexes and single-name swaps, according to the survey.

Amid an uptick in late-cycle volatility, credit derivatives trading volume jumped 65 percent year-on-year in the first half of 2018, according to JPMorgan Chase & Co data.

That doesn’t mean bond managers are satisfied with their options.

Investors are hungry for fresh ways to better guard risk with new -- and more liquid -- instruments, according to the survey.

--With assistance from Dani Burger and Misyrlena Egkolfopoulou.

To contact the reporter on this story: Yakob Peterseil in London at ypeterseil@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma, Randall Jensen

©2018 Bloomberg L.P.