Cryptocurrencies Fall Off Another Cliff

Cryptocurrencies dropped sharply for the second time in less than 24 hours.

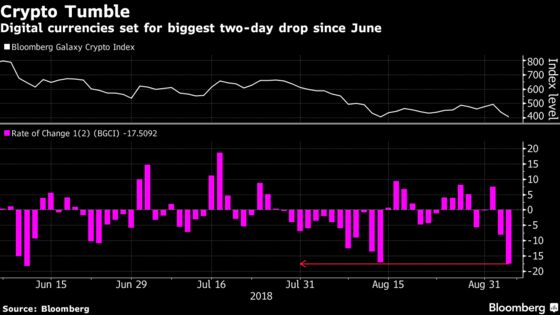

(Bloomberg) -- Cryptocurrencies dropped sharply for the second time in less than 24 hours, sinking toward a nine-month low amid concern that broader adoption of digital assets will take longer than some anticipated.

Bitcoin, the largest cryptocurrency, tumbled as much as 9.8 percent and was trading at $6,480, down 6.8 percent, as of 10 a.m. in New York, according to Bloomberg composite pricing. The Bloomberg Galaxy Crypto Index, a gauge of the largest digital assets, likewise pared some of an earlier decline, when it traded near the lowest level since November 2017. Rival coins Ripple, Ether and Litecoin also slipped.

Cryptocurrency bulls who bet an expanding user base would drive up prices have faced a string of recent disappointments. Business Insider reported on Wednesday that Goldman Sachs Group Inc. was pulling back on near-term plans to set up a crypto trading desk. This comes after last month’s decision by U.S. regulators to reject another round of Bitcoin exchange-traded fund proposals.

“Their name carries weight across the globe,” said Ryan Rabaglia, head trader at digital asset brokerage OSL in Hong Kong, referring to Goldman Sachs. “When people see their name, their eyes may light up, and they say: OK, we’ve finally made it -- the bigger players are going to start to enter.”

At the same time, enthusiasts drawn to Bitcoin’s original promise of anonymity and freedom from government control were also dealt a blow on Tuesday when veteran Erik Voorhees’s trading platform ShapeShift AG said it will begin asking users for personal information.

Regulatory scrutiny over cryptocurrency trading platforms has grown along with usage amid concerns over money laundering and customer protection. ShapeShift’s move is a sign of the growing formalization of a market initially known for its libertarian bent. Imposing mandatory Know Your Customer procedures is “not something we want to do” and a “heavy decision done to derisk under duress,” Chief Executive Officer Voorhees said on Twitter.

While the decision may dispel users that prioritize anonymity, it may also help ShapeShift attract users that trade larger amounts of funds that tend to prefer regulated venues, said Vijay Ayyar, the Singapore-based head of business development at Luno, a cryptocurrency exchange.

“Regulators are never going to be OK with not knowing the identities of who’s doing what and who’s buying crypto,” Ayyar said.

While many banks and institutional investors are dipping their toes into the world of cryptocurrencies, concerns over everything from market manipulation to regulatory uncertainty have prevented institutional adoption. On Friday, finance ministers from the European Union’s 28 member states are scheduled to discuss the challenges posed by the growing popularity of digital assets and whether rules should be tightened.

The market value of virtual currencies tracked by CoinMarketCap.com has slumped about 75 percent from its January peak to about $205 billion.

The next key level to watch for Bitcoin is $5,000, according to Stephen Innes, head of trading for Asia Pacific at Oanda Corp., who said a drop below that threshold may cause losses to accelerate.

For more on Bitcoin risk, check out the Decrypted podcast:

--With assistance from Cormac Mullen and Todd White.

To contact the reporters on this story: Eric Lam in Hong Kong at elam87@bloomberg.net;Justina Lee in London at jlee1489@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Michael Patterson, Todd White

©2018 Bloomberg L.P.