A Rare U.S.-Europe Junk Bond Split Tantalizes Big-Money Funds

A Rare U.S.-Europe Junk Bond Split Tantalizes Big-Money Funds

(Bloomberg) -- Europe’s high-yield bond market has gotten tantalizingly cheap, according to big-gun debt funds.

Money managers at JPMorgan Asset Management and PGIM Inc. who oversee about $70 billion collectively say it’s time to buy.

Even as the market tries to digest the equivalent of $10 billion of new supply forecast for September and political risk simmers in Italy, there’s a valuation buffer, say investors.

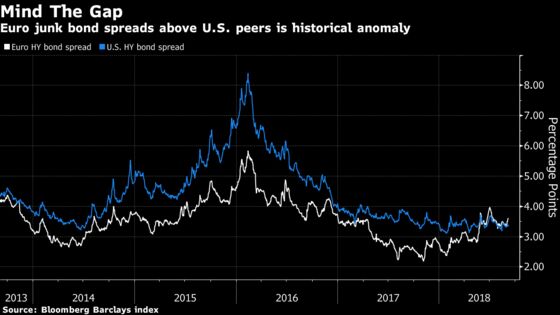

Case in point: Europe’s speculative-grade companies are trading with higher spreads than U.S. peers, driven in part by populists in Rome rising to power in May. That’s a break from historic norms given the region’s typically higher average ratings.

It’s an anomaly that “jumps out” at Michael Collins, a senior portfolio manager at PGIM.

“We’ve actually looked at that relative-value differential, so we’re on the margin buying European high yield relative to U.S. high yield,” Collins said in an interview with Bloomberg TV last week.

“You’ve seen repricing in euro credit purely on perception of political risk rather than fundamentals," said Greg Venizelos, a senior credit strategist in London at AXA Investment. “There’s been a typical kind of contagion effect from Italy to different classes of credit in Europe."

The withdrawal of European Central Bank quantitative easing is a wild card. If it pushes yields higher, companies with heavy refinancing needs would be squeezed. Meanwhile, ‘tourist’ investors who piled into high-yield bonds may return to their safety zones in the investment-grade space, withdrawing cash.

Tatjana Greil Castro, a portfolio manager at Muzinich & Co., says she expects euro-area bonds to get cheaper still.

"The high-yield market has already seen a reprice with as much as a 100 basis points widening so far this year," Greil Castro said at a conference in London this week. "But with just around a 3 percent yield for the asset class on the whole, the expectation of inflows is minimal, which could see spreads widen further still."

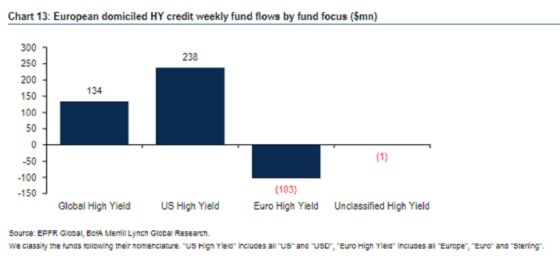

Flows show a flight out of European-focused high-yield bond funds in the last week of August -- even as those with a global and U.S. bent attract cash, according to EPFR flow data.

Still, low inflation and policy uncertainty capping bund yields will also serve to crimp debt premiums.

“You’re going to continue see the zero interest-rate policy, which is going to force people to look at these sorts of corporations to grab yield,” Iain Stealey, head of global aggregate strategies at JPMorgan Asset told Bloomberg TV.

The underperformance of European high-yield relative to U.S. high yield “can reverse,” Stealey said. “Those spreads look pretty attractive to us given the positive corporate fundamentals going on in Europe.”

--With assistance from Lisa Abramowicz and Laura Benitez.

To contact the reporter on this story: Cecile Gutscher in London at cgutscher@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma, Yakob Peterseil

©2018 Bloomberg L.P.