JPMorgan, BlackRock Warn Contagion Hitting Emerging Markets

Some investors have seen the selloff as an opportunity to buy on the basis of stronger fundamentals.

(Bloomberg) -- First came the Argentine selloff. Then Turkey. And before long, assets from South Africa to Brazil and Indonesia were getting hit in a selling stampede across emerging markets.

It’s a phenomenon that has a cadre of investors and strategists from JPMorgan Chase & Co. to BlackRock Inc. reaching for a single word: contagion.

The argument goes like this: while the asset class may offer value over the long haul, investors will sell relatively safe holdings to cover losses in more vulnerable markets or, worse, treat all emerging markets the same and sell indiscriminately. A herd mentality has taken over, meaning no matter what the relative risks and potential returns are in individual countries, investors who choose to buy run the risk of being trampled.

“We are having a confidence crisis in emerging markets, with some level of contagion being present,” said Pablo Goldberg, a money manager at BlackRock Inc. in New York. “With the short-term currency moves, it’s hard to jump in.”

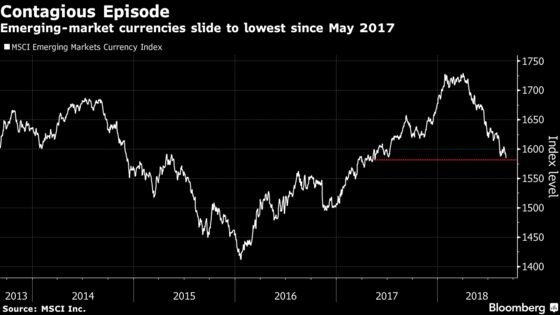

Developing-nation currencies have slid to their weakest levels since May 2017, with the Argentine peso, Turkish lira and Indian rupee among those sinking to unprecedented lows in recent days, reinforcing the view that these aren’t merely idiosyncratic episodes. Indonesia’s rupiah hit its weakest since the Asian financial crisis two decades ago.

Global trade tension, a strengthening dollar and the prospect of more U.S. interest-rate increases led portfolio flows into emerging markets to slow to $2.2 billion last month from $13.7 billion in July, according to the Washington-based Institute of International Finance.

“That’s not a good story for emerging markets,” Anastasia Amoroso, a global investment strategist at JPMorgan Private Bank in New York, said on Bloomberg TV. “As long as trade wars are front and center and the Fed is hiking at a runaway pace versus the rest of the world, I think we are in an environment that argues for a stronger dollar.”

Buying Opportunity

Some investors have seen the selloff as an opportunity to buy on the basis of stronger fundamentals, such as easing inflation, trade surpluses and widening growth differentials between emerging and developed markets.

“One of the interesting things contagion sets up is a selloff in the weak and the strong,” said Arjun Jayaraman, who helps oversee $4.8 billion at Causeway Capital Management LLC in Los Angeles. “That’s when you have to step up and buy the strong currencies, the exporting, current-account surplus countries.”

Stocks from India, South Korea and Taiwan look attractive in this environment, according to Jayaraman. Amoroso said investors will eventually want to step into local debt, while Goldberg said he would prefer hard-currency sovereign debt if trade concerns ease.

Pressure on emerging markets will probably persist for now, with Turkey, Argentina, South Africa, Pakistan, Brazil and India among the weakest links, Wolfe Research strategists including Chris Senyek wrote in a note to clients. The New York-based firm said default probabilities in Asia, interbank lending markets in Europe and credit-default swap spreads from individual banks show some similarities with the 1997 emerging-market crisis, suggesting broader fragility in the asset class.

“Our EM ‘blow-up’ monitor suggests that weakness is spreading across the most vulnerable EM countries,” Senyek said.

--With assistance from Alexandra Stratton.

To contact the reporter on this story: Ben Bartenstein in New York at bbartenstei3@bloomberg.net

To contact the editors responsible for this story: Rita Nazareth at rnazareth@bloomberg.net, Justin Carrigan, Philip Sanders

©2018 Bloomberg L.P.