U.S. Stocks Beating EM by Most Since 1996 Fuels Fear of Peak

Wall Street Debates End of ‘America First’ Trade as EU Struggles

(Bloomberg) -- The great decoupling may be entering its final phase.

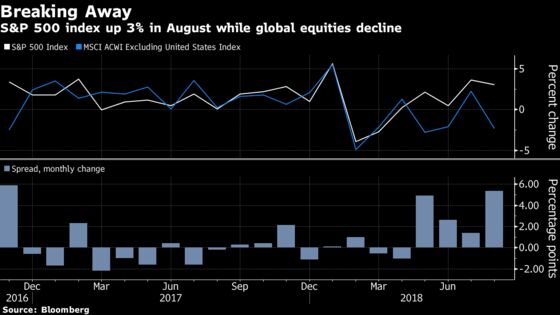

U.S. financial assets surged through the summer while much of the rest of the world floundered. The trend entered a fourth month in August and brought the biggest divergence since U.S. President Donald Trump’s election win in November 2016. That’s left the S&P 500 Index just below all-time highs as Europe’s benchmark equity gauge sits is near a two-month low and developing-nation shares are on the verge of a bear market.

The chasm is dividing Wall Street into two camps: those betting the U.S. will continue to break away from the pack, and others who caution that American financial assets have to fall back to the pack.

John Higgins, a senior markets economist at Capital Economics, is a pessimist on U.S. markets. He expects equities to fall between now and year-end and decline in 2019 as well, due to a slowing domestic economy and retaliatory trade measures by other countries, particularly China, that weigh on multinationals.

Will contagion infect U.S. stocks? Two signals to watch: BI research

“The only other notable occasion in the past quarter of a century when a similar pattern of divergence in the stock markets was seen for any length of time was also during a period of Fed tightening,” according to Capital Economics. “Although we expect interest rates in the U.S. in this cycle to climb until the middle of 2019, we don’t think that the divergence in stock markets will last until then or end with equities elsewhere recovering ground.”

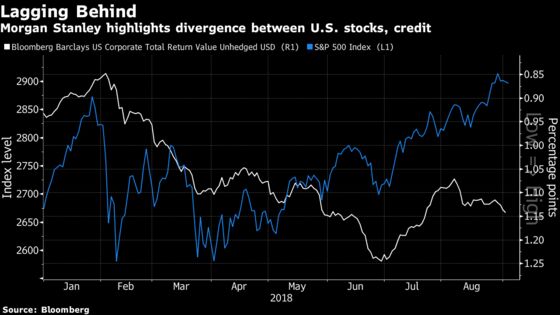

Higgins isn’t alone in the bear camp. The lackluster rebound in U.S. investment-grade credit -- which has interest-rate spreads far from the lows reached earlier this year -- even as equities rally portends downside for stocks, according to Morgan Stanley.

“This is quite a divergence and typical at the end of an economic cycle or before a meaningful equity market correction,” writes chief U.S. equity strategist Michael Wilson.

Seasonality may also be a factor, the strategist adds, as U.S. stocks kick off the weakest month of the year by trading to the downside in the early days of September.

“Correlations can outlast reality for a while as machines chase momentum factors in a quiet summer news cycle” but it won’t last forever, warns Matthew Sigel, a portfolio strategist at CLSA.

Others map out a route for a rosier resolution of the yawning gap between assets in the U.S. and the rest of the world.

“Crowding into U.S. assets doesn’t entail a massive correction, but a window for U.S. underperformance,” said Jared Woodard, a global investment strategist at Bank of America Merrill Lynch. “If the easing we’ve had out of China shows up in South Korean exports and the Kospi, it shows there’s room to run -- and it’s much easier to make a case for recovery in the rest of the world than a catastrophe in the U.S.”

BofA’s sell side indicator dipped to a nine-month low in August, a sign Wall Street’s enthusiasm for U.S. stocks is waning.

Cleanest Dirty Shirt

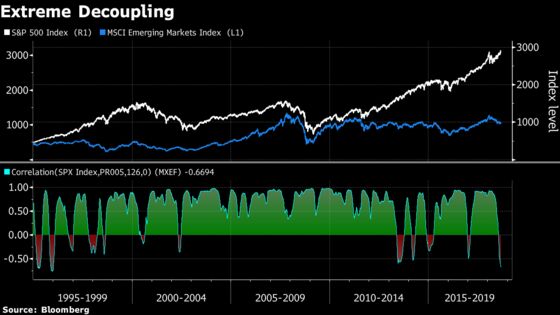

Over the past six months, there’s been an extreme decoupling between U.S. and emerging market equities, which typically move in the same direction. Now, the correlation between the two has turned the most negative since 1996, which followed the Mexican currency crisis that preceded the broad Asian financial emergencies.

The divergence narrative was reinforced this week by data signaling no reprieve for some of the most embattled emerging markets. South Africa unexpectedly sank into a recession in the first half of 2018 while Turkish inflation accelerated by more than anticipated in August.

At the same time, a looming budget showdown between Italy and the European Union that’s seen spreads blow out has sparked risk aversion and reduced the appeal of European assets.

Still, the emerging-market selloff of recent weeks amid turmoil in Turkey and Argentina might not yet be sufficiently severe to spill over to U.S. markets or domestic activity.

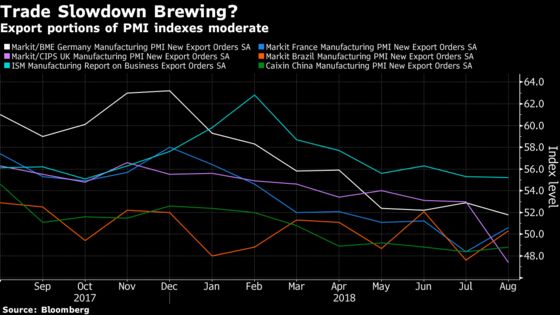

The growth in export orders is off the boil worldwide, but the U.S. is holding up better than other large economies.

The current U.S. policy mix is “potentially poisonous” for developing nations, according to Christian Keller, head of economic research at Barclays Plc. He sees as trade restrictions hampering their ability to capitalize on higher U.S. growth via exports, while rising U.S. interest rates in light of more robust activity stateside bring capital to American assets.

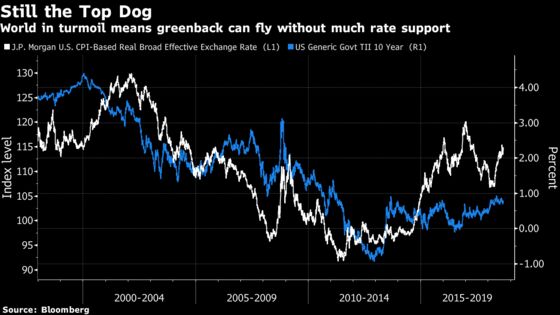

For the U.S. dollar, relative outperformance going forward may be mostly driven by the lack of strength everywhere else.

“The dollar is overvalued and the Fed isn’t doing anything to send it higher, but that’s enough for it to remain top dog in currency markets in the absence of good news elsewhere,” writes Kit Juckes, a global fixed income strategist at Societe Generale. “There’s not much to make me think the dollar should be going up, but there’s plenty to make me nervous about other currencies.”

Even as officials in Turkey, Argentina and Italy act to try to convince traders that the situations are under control, their measures “are plasters on a wound that is already seen in the data,” said Ben Emons, head of credit portfolio management at Intellectus Partners.

Turkey’s manufacturing purchasing managers’ index fell to 46.4 in August, while Italy’s tumbled to 50.1 -- a tick above the mark that separates contraction from expansion. Divergence could persist for as long as the ripple effects from the repatriation of U.S. dollars filter through to domestic assets, according to Emons.

To a certain extent, American outperformance in markets reflects what’s going on in the real economy. The gap between the U.S. ISM manufacturing gauge and similar measures for China, the Eurozone, and the world has reached its highest levels on record, going back to 2015.

The $1 Trillion Club

The U.S. has another big thing going for it that the rest of the world doesn’t: Its equity benchmarks are dominated by massive technology firms that haven’t faced the headwind of domestic regulation.

Amazon.com Inc., which has managed to draw the ire of both Donald Trump and leftist U.S. Senator Bernie Sanders, eclipsed a $1 trillion market cap on Tuesday. The primary upshot from Facebook Inc. Chief Executive Officer Mark Zuckerberg’s testimony before Congress in April seems to be that lawmakers’ barks are worse than their bites.

Europe doesn’t boast tech heavyweights to rival the U.S.-based behemoths. And China has moved to crack down on online games to the detriment of Tencent Holdings Ltd., the third-largest stock in the Hang Seng Index and largest weighting in the MSCI Emerging Markets Index.

The U.S. decoupling from the rest of the world will play out until “the very late part of 2019,” said Credit Suisse chief U.S. equity strategist Jonathan Golub, who lists technology as among his preferred sectors.

In any event, macro noise abroad won’t overwhelm the fundamental forces pushing U.S. risk assets higher, says Brian Reynolds, asset class strategist at Canaccord Genuity.

“Our nation’s public pensions, who are now the dominant global investors, are focused on meeting their outsized return assumptions,” he writes, highlighting their increased appetite for credit. “Those flows should continue to produce more buybacks and M&A designed to boost stock prices until two years after the yield curve inverts.”

To contact the reporter on this story: Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Brendan Walsh

©2018 Bloomberg L.P.