One-Way Vol Bets Seen as ‘Fool’s Errand’ by 6,000% Winner

One-Way Vol Bets Seen as ‘Fool’s Errand’ by 6,000% Winner

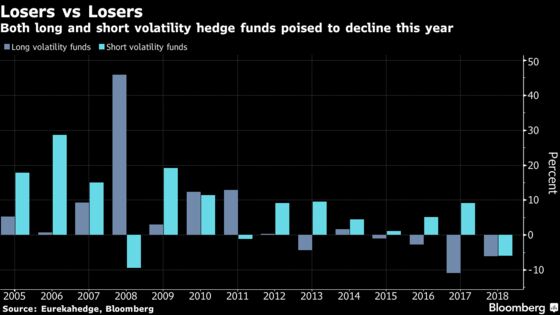

(Bloomberg) -- Heads you lose, tails you lose. This year for the first time, trading strategies betting on a jump in equity market volatility and those wagering for calm are both losing.

The reason? February’s “volmageddon” blow out, which did enough to sink short-volatility strategies but not enough to protect long-vol trades from the tranquility that’s enveloped stocks on their way to new peaks.

“Winning trades are quite hard to come by,” said Lincoln Edwards, founder of Houndstooth Capital Management LLC, a $9 million hedge fund in Austin, Texas that reaped 6,000 percent in February’s meltdown. These days his bets seek to ride volatility on the way down as well as up; trying to time the crests is “a fool’s errand,” he reckons.

Spikes, No Spillover

The remainder of 2018 is poised to confound volatility traders searching for a clear winning bet. Though a supportive economic backdrop will help to subdue market swings, too many threats linger to assume the coast is clear, according to the economics research team at Goldman Sachs Group Inc.

“We think that in the near term neither a high nor low vol regime appears likely, with potential for vol spikes but limited spillover,” the strategists, including Christian Mueller-Glissmann, wrote in a Tuesday note.

Playing both sides, expecting traders to change their mind as quickly as they made them up, may be one of the few ways to avoid getting caught by this year’s schizophrenic market. The relative value category, market-neutral vol funds that look to play ups and downs, are the only ones in the Eurakahedge indexes up this year, though barely.

Edwards at Houndstooth says he likes puts on short-VIX positions just as the gauge spikes. While risky, the trade pays off in a market that reliably returns to calm.

“We like VIX options that trade a couple months out,” he said. “Since February, we’ve seen some sort of VIX spike almost every single month. Selling option spreads a couple months out allows you enough time for the VIX to calm back down and erode the options’ value.”

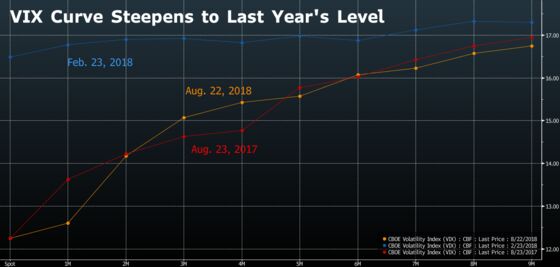

VIX Repeats

Turbulence in stocks is muted even as convulsions from Turkey to Argentina send emerging markets into a tailspin and the U.S. escalates a trade war with China. A steep VIX futures curve looks virtually indistinguishable from a year ago, a sign of dimming demand for near-term volatility protection. And February’s winning bets have turned into losers six months on.

“Short-vol funds are on the recovery up from February when they saw massive losses,” said Mohammad Hassan, head of hedge fund research and indexation at Eurekahedge. “On the other hand the long-vol funds will likely see their February gains get further eroded in a low-volatility environment.”

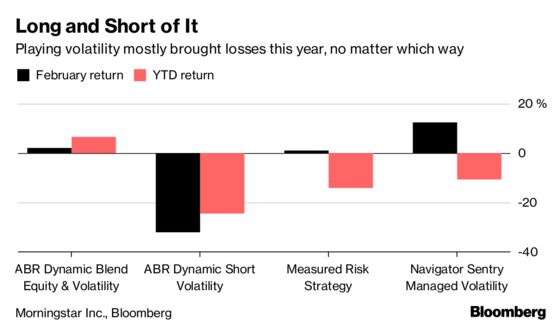

For a few funds that came into February prepared for the bursting of the volatility complex, focus has returned to controlling costs as profits for the year flip to losses.

Clark Capital Management Group saw a 12 percent gain in its managed volatility strategy fund in February. The $13-billion asset manager is using option spreads to contain risks on their bets as the fund, Navigator Sentry Managed Volatility, has slipped 11 percent over the year.

“There are periods of time where we’re more interested in controlling the cost of the hedging strategy -- like right now -- where your outlook is positive in markets, it’s a risk-on environment and we don’t see credit spreads moving higher,” said Sean Clark, chief investment officer.

Managers of Unigestion’s Multi Asset Navigator fund are still bullish on the VIX, but less so than in January as the cost of hedging piles up. At the start of the year they bought calls on the index because they expected stocks to deflate from lofty valuations. The portfolio is up 2.2 percent this year, which puts returns above 87 percent of peers, according to data compiled by Bloomberg.

“Net-net we have a slight long volatility position in the portfolio but that can change pretty quickly,” said Salman Baig, multi-asset investment manager at the Geneva-based firm. “You’re paying a cost for holding this insurance and the risks you see never materialize, or they materialize but it doesn’t find its way into implied volatility.”

Risky Business

Still, Baig sees plenty of reason to hedge: Italy’s much-anticipated budget next month and a fresh dose of political risk, the threat of a bigger slowdown in China that spreads to the U.S. and Europe, contagion from Turkey’s woes, and U.S. protectionism sapping global trade.

“We’re still believers in the global growth story and see that story favoring developed-market equities,” Baig said. “That said there’s a big shadow over this positive growth picture.”

And even as long-vol bets get flushed out, a few are up on the year. The ABR Dynamic Blend Equity and Volatility Fund (ABRVX) has gained (though not as much as the S&P 500) despite this year’s short-lived bouts of turbulence.

“Stocks have rallied out of every possible scenario,” from geopolitics to trade war to inflation to the threat of an economic slowdown, said Edwards at Houndstooth. Still, “people understand that eventually something terribly wrong will occur. It’s not a matter of if -- but when.”

To contact the reporters on this story: Dani Burger in London at dburger7@bloomberg.net;Yakob Peterseil in London at ypeterseil@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Cecile Gutscher

©2018 Bloomberg L.P.