Mergers and Math Announce Their Conscious Uncoupling

Mergers and Math Announce Their Conscious Uncoupling

(Bloomberg Opinion) -- Math and mergers have always had a love-hate relationship. This year, you could say they’ve consciously uncoupled.

Megadeals continue to sweep through the U.S., led by the media and health-care industries, while over at Tesla Inc., Elon Musk has revved up talk of a buyout transaction for the record books. Many of these deals have something in common, and it’s not just sky-high prices. They tend to be personality-driven negotiations that require spectators to put down their calculators and put faith in one person’s vision, whether the numbers precisely check out or not.

That’s the challenge in analyzing M&A these days. When characters like Musk and Rupert Murdoch are in the mix, trying to justify each incremental dollar in a bid or fussing over the Ebitda multiple feels beside the point. But as the figures get more eye-popping, the analysis must get more creative, and history has shown that megadeals usually don’t live up to management’s ambitious projections. Then again, linking up with rivals or expanding to other parts of the food chain is the clearest way for companies from Walt Disney Co. to CVS Health Corp. and General Mills Inc. to protect profits and stave off new competition that’s upended their markets.

Is Disney overpaying for the 21st Century Fox Inc. assets that Murdoch is selling? Maybe not. CEO Bob Iger has proven to be the best dealmaker in the media space, and there’s immense value in controlling so much popular TV and film content. It will help round out Disney’s strategy for on-demand viewing services as it tries to take on Netflix Inc., and there will also be significant cost savings. But let’s face it, the ultimate price came down to whatever Iger or Comcast Corp.’s Brian Roberts was willing to pay to win. Disney, of course, wouldn’t admit its fierce rival forced it to pay up. Instead, here’s how Disney explained its $19 billion sweetener in June:

Since the original agreement was announced, the intrinsic value of these assets has increased, notably due to tax reform and operational improvements.

If you say so.

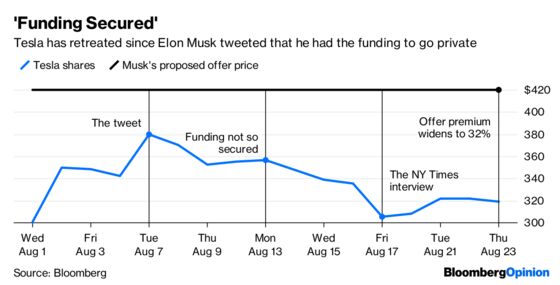

At Tesla, Musk flat-out admitted that his $420-a-share buyout proposal had no quantitative basis. He simply tacked on a typical 20 percent premium to the stock’s price at the time, which came to $419. He then rounded up to $420 because “it seemed like better karma,” assuring folks that he “was not on weed.” In fairness to Musk, it’s not like one should expect a discounted cash-flow analysis—Tesla doesn’t have any. Still, each dollar per share represents another roughly $170 million that Musk would need to fund, and so far it’s unclear how he’ll do that and why he even wants to do it now.

Earlier this year, I explained why General Mills will need its Wheaties to make its latest deal work for the packaged-food giant. As it tries to shift away from the shrinking cereal market, General Mills decided to dish out nearly $8 billion for Blue Buffalo Pet Products. That’s a steep price at more than 20 times projected Ebitda—even for a fast-growing business—and it ranks among the most expensive consumer-products acquisitions ever. While I think Blue Buffalo is one of the best takeover targets General Mills could have chosen, the deal has also saddled the company with over four times more debt than Ebitda.

Deal-related debt could be a major constraint on CVS’s business, too, as my colleague Max Nisen has written. CVS is seeking regulatory approval to acquire insurer Aetna Inc. for $68 billion in cash and stock, plus the assumption of Aetna’s own net borrowings. In the same way that media companies are scrambling for ways to defend against Netflix and Amazon.com Inc., the health-care industry is also facing a threat from Amazon.

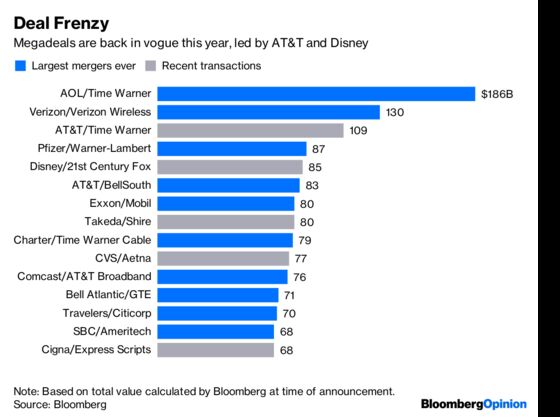

Of the 15 biggest U.S. takeovers in history, five are from the past year. Tesla could also be the largest leveraged buyout or management buyout ever, topping the 2007 LBO for electric utility TXU, which later went bankrupt.

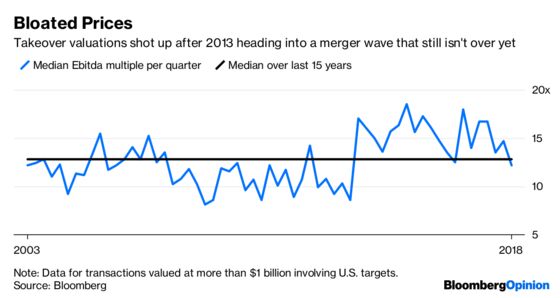

Valuations have been at highs during the deal boom of the last few years, particularly in the U.S. This quarter the median Ebitda multiple for acquisitions of American companies has fallen just slightly below the 15-year average:

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tara Lachapelle is a Bloomberg Opinion columnist covering deals, Berkshire Hathaway Inc., media and telecommunications. She previously wrote an M&A column for Bloomberg News.

©2018 Bloomberg L.P.