Volatility Trades Get Reborn as Market Split Spurs New Short

Volatility Trades Are Reborn as Two-Tier Market Spurs New Short

(Bloomberg) -- Call it the volatility trade, squared.

As macro shocks hit global markets, a complex strategy that bets the gap between stock winners and losers will grow is spreading across hedge funds, real-money managers and even private banks.

The so-called dispersion trades offer a way to play a slew of market themes, everything from splits among tech stocks to the prey and predators of the M&A boom and the trade-war fallout.

Known as a short-correlation bet, it pairs a long and short position in equity options to profit from diverging prices.

Those betting economic shifts will separate the wheat from the chaff with renewed vigor can earn steady returns -- even if they lack conviction on which companies will boom and which will suffer. The exotic investing strategy typically only falters when tracked shares move together.

With shorting volatility a key ingredient in the trade, it comes with a health warning for tourists and practitioners alike.

“It’s an elegant strategy but it’s definitely complex,” said Tobias Hekster, co-chief investment officer at hedge fund True Partner Capital. “It requires quite a bit of management and maintenance.”

Fast-money traders with a short-correlation bias incurred “significant” losses in August 2011, for example, when the Cboe Volatility Index gapped upwards by 25 points, according to Hekster, a volatility trader.

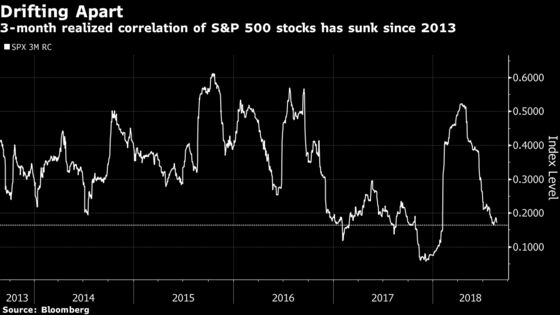

Splitting Up

For now, the strategy is having its day in the sun.

U.S. equities are dancing to their own tunes, as a barrage of market shifts takes stock-picking to the center stage.

Tit-for-tats on trade have led to the growing outperformance of businesses tied to the domestic economy. Tax reform, meanwhile, is inspiring investors to bid up companies that have the most to gain. Stocks are moving apart -- a climate ripe, in theory, for the strategy.

The classic trade involves selling options on an index such as the S&P 500, while buying derivatives on a group of individual equities within the gauge. That dual volatility bet -- short on the index leg and long on the individual stocks -- leaves investors implicitly short correlation.

It’s profitable when the stocks swing around more than the index does -- in other words, when the link between them decreases.

“You just need to have the view that there will be a certain amount of dispersion -- or differences in returns -- amongst a set of stocks,” said Patrick Kondarjian, head of sales in institutional and wealth management solutions at HSBC Holdings Plc.

Hedge Seekers

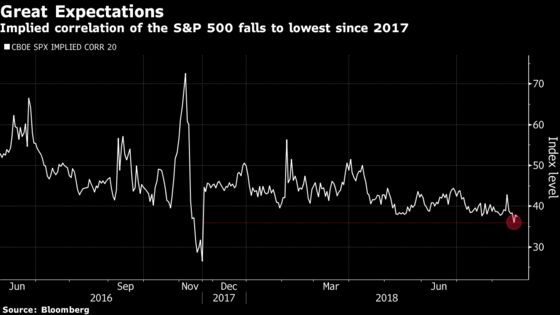

Proponents have a powerful wind at their backs.

Implied volatility of popular indexes like the S&P 500 tends to be inflated by demand for options from hedge-seekers, setting up an effective arbitrage opportunity.

“Much of the principle behind the correlation richness comes back to the idea that there’s a systematic bid for volatility at an index level from people who are hedging,” said Pete Clarke, equity derivatives strategist at UBS Group AG. “There’s less of a bid and hence less of a richness at the stock level due to more balanced flows on single-name options.”

With hedge funds using exotic derivatives like bespoke options and variance swaps, it’s been a forbidding proposition for most -- until recently. For the crowd that’s unable to trade over-the-counter derivatives, banks are democratizing short correlation via customized structured notes, said Kondarjian.

“We have seen much more interest from a wider community of clients -- asset managers, asset owners, wealth managers -- who are coming into this type of product as a means of diversifying their investments.”

A story helps, too.

While hedge funds often enter a trade based on the economics, traditional managers are more inclined to buy if there’s a theme, from leverage to geopolitics. UBS, for example, recommends a dispersion trade using swaps on the Nasdaq 100 versus a basket of constituent stocks, to hedge tech-rally disruptions. Another trade idea applies the concept to global banks, whose performance may diverge based on the strength of their balance sheets.

Regardless, investors had better tread carefully.

The simplest version of the trade that bets heavily against S&P index volatility could backfire spectacularly. A propitious time to enter is when implied share linkages are high -- not when it’s low, as is the case currently.

“If you suddenly get a very sharp correlated down move, you’re in pain,” warns Hekster at True Partner.

To contact the reporter on this story: Yakob Peterseil in London at ypeterseil@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma

©2018 Bloomberg L.P.