Trump Topples U.S. Exceptionalism in Markets as World Catches Up

Trump Topples U.S. Exceptionalism in Markets as World Catches Up

(Bloomberg) -- President Donald Trump may have put a lid on American exceptionalism in financial markets.

U.S. stocks were pulling away from the pack and the greenback was soaring as the rest of the world showed signs of political and economic weakness. Then the president browbeat the Federal Reserve’s monetary policy, bemoaned the strength of the dollar and accused Europe and China of currency manipulation.

It was all enough to reverse the greenback’s rally and give such a boost to shares in the rest of the world that they’ve outperformed the American equity benchmark for the past few days. U.S. stock futures continued to weaken Wednesday after the president’s personal lawyer implicated him in campaign finance violations. Meanwhile, global equities extended gains.

U.S. financial assets have stumbled compared with the rest of the world, halting -- at least for now -- an unrelenting four-month trend. While many analysts say superior earnings growth stateside may continue to see U.S. stocks outperform and that the cross-asset action is just a pause, a growing cohort say the ‘America First’ trade can’t continue.

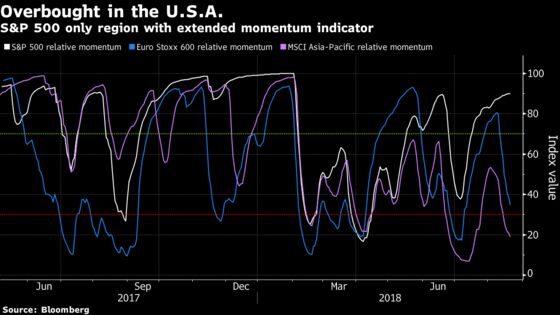

“The recent divergence in the performance of U.S. equities versus the rest of the world is unprecedented in history,” writes Marko Kolanovic, global head of quantitative and derivatives strategy at JPMorgan Chase & Co., highlighting a record divergence in U.S. price momentum relative to Europe and emerging markets. “Given that this is such a rare occurrence (has never happened for both Europe and Asia), it suggests to us this is a market condition that will not persist.”

As the president singled out Jerome Powell for not being a “cheap money” chairman of the Federal Reserve, the foreign exchange and rates markets have heard the message.

“U.S. Treasury yields have responded and softened to levels last seen in mid/early-July, eroding the fundamental underpinnings that have driven the bulk of the U.S. dollar rally since mid-April,” writes Shaun Osborne, chief FX strategist at Scotiabank. “The USD’s most recent upswing was not supported by movements in interest rate differentials and driven primarily by safe haven flows and positioning adjustments sparked by the panic in Turkey.”

Release Valve

Traders had been betting the greenback’s strength would endure, with a net short position on all other G10 currencies for the first time since January 2017. That fits the argument that this week’s softness is just a blip.

“The stretched U.S. dollar has required a trigger to release some of the energy,” according to Mark McCormick, North American head of FX strategy at TD Securities. “Trump offered a release valve, implying that the Fed is undoing his work on the economy.”

A decisive move higher for the euro “would suit our long-term bias but really, President Trump jaw-boning isn’t a sensible reason for it to happen,” writes Kit Juckes, global strategist at Societe Generale. “A shift in the E.U./U.S. relative economic surprise indices is a better reason.”

Economic Convergence

Indeed, economic expectations have now been reset amid less-disappointing European data coupled with U.S. releases that haven’t lived up to analysts’ estimates.

The surprise indexes for the eurozone, G10, and emerging markets are all higher than the U.S. for the first time since October. Global equities modestly outperformed their American peers during the six-month stretch in 2017 when U.S. data proved underwhelming relative to these regions.

Michael Purves, chief global strategist at Weeden & Co., is calling for a brisk retreat in 10-year Treasury yields in light of relatively unimpressive U.S. data and stretched positioning -- with ripple effects across risk assets.

“As we saw in early 2014 and 2017, this drop in this index can reinforce a drop in yields, and this has yet to happen,” he writes. “If we are correct and yields do fall here, we would expect the dollar to decline, U.S. small caps to weaken (at least on a relative basis) and the prospects for an emerging markets relief rally to increase significantly.”

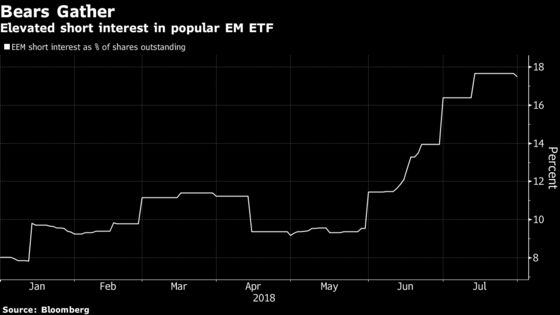

Any relief rally for embattled developing-nation equities may also get a hand from elevated short interest, according to Macro Risk Advisors chief macro strategist, Mayank Seksaria.

“The probability of a tactical rally in EM and bonds is enhanced by the large short base in both asset classes,” he writes. “As the narrative shifts, U.S. dollar and bonds are both vulnerable to a squeeze given heavy positioning.”

“EM assets are likely to remain volatile in the short-term but given valuation support and overall investor positioning, there is the scope for a sharp rebound should the dollar stabilize, China growth rebound, or the combative trade rhetoric between the U.S. and China evolve into something more conciliatory,” adds Erin Browne, head of asset allocation at UBS Asset Management.

--With assistance from Cormac Mullen and Dani Burger.

To contact the reporters on this story: Luke Kawa in New York at lkawa@bloomberg.net;Sid Verma in London at sverma100@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Samuel Potter

©2018 Bloomberg L.P.