The Fed May Be About to Make a Mistake

The Fed May Be About to Make a Mistake

(Bloomberg Opinion) -- The natural state of a capitalist economy is expansion. Recessions occur when “something breaks” rather than an expansion simply dying of old age. Unfortunately, central banks have a history of pumping the brakes for too long and too hard when attempting to contain growth and inflation and are often the cause of a recession.

Given that the Federal Reserve has now shifted away from its so-called third mandate of financial stability, which dominated much of the post-crisis period, and back to worrying about faster inflation, concern about too much tightening is warranted. While inflation is indeed accelerating, investors remain skeptical that higher prices are returning with the vengeance needed to justify the several more interest-rate hikes the Fed is talking about. We fear another Fed mistake is in the offing.

The chart below shows the percentage of official Fed communications — speeches, testimonies and statements — by topic since the mid-1990s. Inflation concerns and hawkish rhetoric make up well more than half the talk, and are crowding out dovish comments and global and financial-stability concerns.

Zeroing in on inflation, Fed Chairman Jerome Powell and his fellow policy makers at the central bank have talked more about inflation in 2018 than any other post-crisis year. A good example is Chicago Fed President Charles Evans, a longtime monetary dove, who has shocked Fed watchers by putting on his seldom-used hawk talons. Evans suggested the Federal Open Market Committee may need to raise rates to “somewhat restrictive” levels to combat anticipated inflation.

Evans justified his position by pointing to economic surveys which see more inflation on the horizon. In a Bloomberg Opinion column in May we argued that such surveys no longer work. Nevertheless, investors are acknowledging the Fed’s commitment to battling higher prices by fully pricing in a rate hike at the Sept. 26 FOMC meeting. Even the December meeting shows a very high 70 percent probability of a hike.

The next chart shows that this aggressive pace of rate hikes has decoupled from realized economic growth. The blue line shows the Citigroup U.S. economic data change index, which is an aggregate measure of incoming economic releases relative to one-year averages. The orange line shows the number of rate hikes priced in over the next 12 months. The data is clearly softening, yet expectations for rate hikes remain elevated. Inflation concerns are superseding actual economic data.

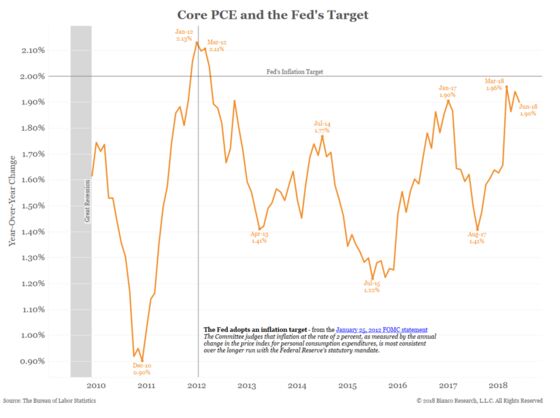

Is the Fed right to worry so much about inflation? Six years ago, the Fed adopted a 2 percent inflation target. As the chart below shows, other than the first few months after it was implemented, this target hasn’t been reached. Yet Fed officials are preparing for a battle by assuming inflation will exceed a target it has not hit it in seven years.

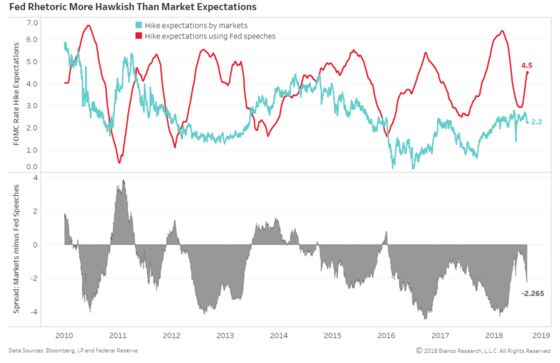

To illustrate how Fed talk is running ahead of market expectations, the chart below uses the central bank’s own words to estimate the number of rate hikes expected over a 12-month period. We modeled the number of rate hikes synonymous with Fed rhetoric from 1996 through 2007, and then projected it starting in 2008. The blue line provides a market-based expectation for rate hikes over the next 12 months taken from the futures market. The spread between market and Fed expectations for rate hikes is shown in the bottom panel. Values below zero show periods when Fed talk is more hawkish than market pricing.

This spread between Fed rhetoric and market expectations is also shown in blue in the chart below. It is compared to U.S. 10-year Treasury note yields. Periods of the Fed being more hawkish than markets have coincided with declining yields. Conversely, when the Fed is less hawkish than the market — positive blue line — yields have risen. However, this circumstance has been infrequent in the post-crisis period, which we believe has contributed to the inability of 10-year yields to break out to the upside. Fed rhetoric is giving bond vigilantes a reason to drive yields higher.

The case for more Fed tightening hinges on inflation. The Fed assumes it will return, and it is talking about hiking well ahead of the economic data and market expectations. If policy makers are correct, and the economic surveys are right this time and inflation returns, they have the correct policy. But if the surveys are wrong — like they have been for two decades — and the Fed is worrying too much about something that doesn’t materialize, then it risks “breaking” the nine-year old expansion and becoming the catalyst for a recession. Evans needs a better argument.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Jim Bianco is the President and founder of Bianco Research, a provider of data-driven insights into the global economy and financial markets. He may have a stake in the areas he writes about.

Ben Breitholtz is a data scientist at Arbor Research & Trading. He may have a stake in the areas he writes about.

©2018 Bloomberg L.P.