Leveraged-Loan Lovefest Will End in Heartbreak

Leveraged-Loan Lovefest Will End in Heartbreak

(Bloomberg Opinion) -- Moody’s Investors Service last week published an in-depth look at U.S. leveraged loans. And it seems the more the analysts dug in, the more alarmed they became.

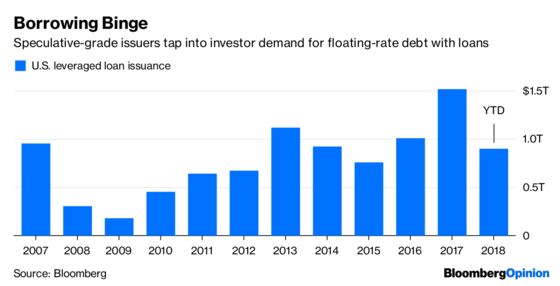

Yes, the nearly $1.4 trillion market can take comfort in a low 3.4 percent default rate that Moody’s projects will only get lower, most likely dropping to 2.2 percent over the next year. But that’s largely where the good news ends. In its report, the credit-rating firm is emphatic that when the credit cycle takes a turn for the worse, leveraged-loan investors will be in for a rude awakening, even compared with the financial crisis.

The loans have become popular in recent years because they carry floating interest rates, which better shield buyers from losses as the Federal Reserve tightens monetary policy. They’ve also been promoted as a safer alternative to high-yield bonds because they’re usually backed by collateral. It’s all led to an explosion in popularity, particularly through collateralized loan obligations, which are pools of leveraged loans divided into tranches. My Bloomberg Opinion colleague Stephen Gandel recently called CLOs the new hedge funds. Barron’s has suggested individual investors get in while they can.

The Moody’s report serves as a sobering reminder that we’re at “a high point in the credit cycle” and that the good performance is unlikely to last. The analysts point to a potentially lethal mix of weaker investor protections, a smaller amount of unsecured debt to cushion losses and the demand for loans leading investors further down the rating scale. All told, the average recovery rate on U.S. first-lien loans will probably decline to 61 percent in the next downturn, compared with a 77 percent long-term historical average and 70 percent in 2008. Second-lien loans may recover only 14 percent, down from 43 percent.

The market is not pricing in these risks. Rather, it’s the general ambivalence of investors that’s allowing loans with weak covenants (often called “cov-lite”) to percolate in the first place. Moody’s estimates the debt cushion below cov-lite loans fell to 20 percent in 2016 and 2017, down from 33 percent before the crisis. Plus, a quarter of recent transactions were first-lien-only structures, compared with just 5 percent a decade ago. That makes a big difference in recovery expectations — being first in the pecking order doesn’t mean much if everyone else is, too.

There are other ways that loan issuers are eroding creditors’ positions, effectively making them no more secure than high-yield bonds. By Moody’s estimate, overall covenant quality in leveraged loans is weaker today than in 2007 across every risk category.

Now, you may be thinking that those risks are offset by the returns on the floating-rate loans. That depends how you measure it. The S&P/LSTA Leveraged Loan Total Return Index, for one, is up 3.1 percent this year — a strong showing in a largely down year for fixed-income assets. But the price of the $7.4 billion Invesco Senior Loan ETF (ticker BKLN) is flat on the year, and over the past three years its dividend has shrunk 2 percent.

That appetite is starting to wane. Investors added just $23 million overall to U.S. leveraged loan funds in the week ended Aug. 15, down from $199 million a week earlier, according to Lipper data. ETFs fared the worst, with $289 million of withdrawals, the largest outflow since mid-November.

It remains to be seen whether that’s just a temporary exodus. The market will need all the support it can get, judging by data compiled by Bloomberg News’s Lara Wieczezynski. Issuance related to mergers and acquisitions is poised to reach $27.3 billion after the U.S. Labor Day holiday, almost double what it was at the same time in 2017.

On the other hand, less cash pouring into loans is probably just what the market needs right now. This is perhaps the most troubling finding in Moody’s analysis of weakening creditor protections:

“They are creating credit risks that portend an extended and meaningful default cycle once the current economic expansion ends. This would mean more defaults than the last downturn as well as lower recoveries, which would undercut a foundational premise for investing in loans.”

No one ever wants to harm a market’s foundation, much less a nonstandardized one that’s nearly doubled over the past decade. But that’s the existential risk that leveraged loan investors now face.

I’m not a big believer in the idea that “CLOs are the next CDOs,” as some suggest. It’s almost too neat to tie loan pools to the debt structures that brought the financial system to its knees. Still, it would be an unequivocally good idea to start pushing back on some of the worrisome borrowing trends highlighted by Moody’s. Just because an investment is humming along now doesn’t mean it can’t still end in tears.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2018 Bloomberg L.P.