Cheap Stocks, 2% Bonds and Modest Earnings Built Record Bull Run

From tame valuations to little competition, these were the forces that sent the S&P 500 up 320 percent over 3,453 days.

(Bloomberg) -- In hindsight, it all made sense.

Though born at the depths of a crisis, rarely has a bull market had better support than this one, which just became the longest ever recorded by some definitions. Tame valuations, little competition and earnings growth that looked spectacular but rarely got above the historical trend -- these were the forces that sent the S&P 500 up 320 percent over 3,453 days.

Is it over? A look at the forces that powered the rally that just usurped the dot-com bubble suggests the ingredients for gains haven’t been used up.

“Often when you hit these milestones, it causes psychological issues,” said Tom Plumb, chief investment officer of the Plumb Funds in Madison, Wisconsin. “But the reality is, it’s long because we’ve been a favorable environment, and a lot of the underpinning of that favorable environment is still in place.”

Here is a rundown of where these forces stand right now.

Valuations

Starting with one of the cheapest multiples on record, the bull owes a lot of its resilience to the fact that stocks have almost never strayed far from the historic norm relative to how much companies make in profits.

The S&P 500 traded below its average price-earnings ratio through 2015 and has since shown few signs of stretched valuations, apart from the few months leading up to the January highs. At 17.6 times forecast income, the ratio is now slightly above the mean of 17 since 1990.

Fed Model

The bull case for equities got even more convincing when compared with the bond market. Thanks to years of efforts by the Federal Reserve to keep interest rates low to stimulate demand, “there is no alternative,” or TINA, has been bulls’ mantra for stocks.

The argument is best illustrated by the so-called Fed Model, which compares the relative value of equities to fixed income. Going by that, stocks were a screaming buy in March 2009, with S&P 500’s earnings yield sitting at more than 5 percentage points above the 10-year Treasury note. While the advantage has now narrowed to 2 percentage points, it still shows value in stocks. Particularly when adjusted for inflation, Treasuries have returned almost nothing over the past five years.

Earnings Machine

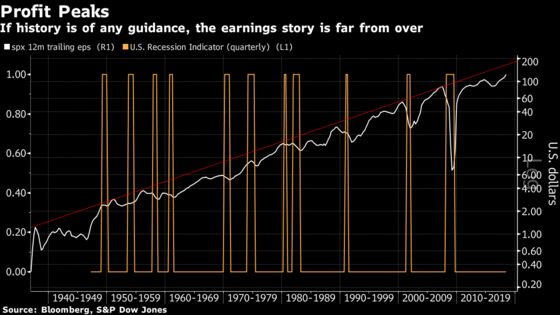

Helping market valuations largely stay in check is the earnings machine that has been running since the economy recovered from the global financial crisis. At first glance, the growth rate is nothing but spectacular. At 9 percent a year, the pace of profit gains since 2009 exceeds the average of 6 percent a year since 1936.

Yet a closer look shows that despite the acceleration, all the gains were only enough to bring S&P 500 profits back to a trendline established over the past eight decades. Blame the lack of progress on the 2008-2009 recession that turned corporate America to the brink of a loss and then the oil-induced earnings contraction in 2015. All together, the lost profits took years to recover.

The sliver lining, if history is of any guide, is that the profit cycle is far from over. While every instance is different, a chart that plotted the peak of past profit cycles shows that corporate earnings currently sit roughly 30 percent below levels that would be deemed too high to sustain.

Corporate Savior

The bull market could have died if companies themselves hadn’t come to the rescue whenever investors bailed out at the first hint of trouble. Since March 2009, corporate America has bought back $4 trillion of its own shares and doled out $3 trillion to shareholders in dividends. That’s equivalent to about a third of the total value that U.S. stocks have added over the same period.

While the use of cash has constantly drawn criticism, companies are showing no signs of slowing down. As President Donald Trump’s tax cuts freed up more money for firms, they’ve announced $777 billion of buybacks this year, a 76 percent surge from a year ago, data compiled by Birinyi Associates Inc. showed.

To contact the reporter on this story: Lu Wang in New York at lwang8@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2018 Bloomberg L.P.