‘America First’ Risks Making U.S. Assets a Costly Last Resort

‘America First’ Risks Making U.S. Assets a Costly Last Resort

(Bloomberg) -- America First seems to have become an investment theme by default, as money managers turn to the U.S. in a fraught global environment. The danger is that these flows may be concealing risks in the world’s safe haven.

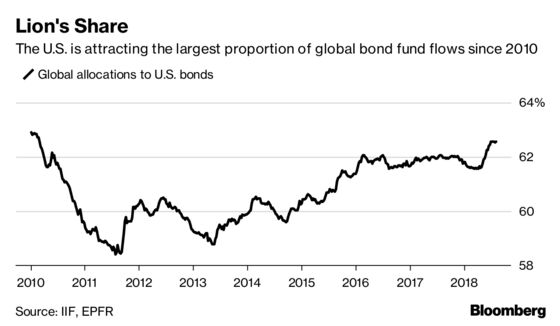

The prospect of the strongest economic expansion since 2005 has helped draw investors to American markets. Geopolitical uncertainty is magnifying the move, despite rising domestic political risks. The percentage of global bond-fund allocations to the U.S. reached 62.6 percent in August, the highest since 2010, according to the Institute of International Finance. If sustained, this demand could exacerbate distortions: Robust growth and Federal Reserve rate hikes haven’t managed to push 10-year Treasury yields above 3 percent for long, and credit spreads are near their tightest levels in a decade.

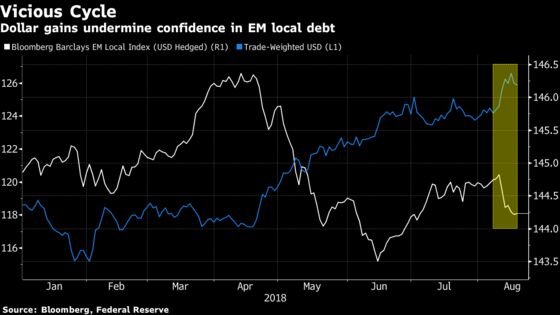

What’s more, a vicious cycle may be developing, where U.S. sanctions and tariff threats are driving yet more cash toward American markets. Even with a decline over the past week, the Bloomberg dollar index is still up more than 5 percent since mid-April. The strength puts pressure on emerging economies, which have amassed about $3.7 trillion of dollar-denominated borrowings. One question for investors is whether the U.S. can remain immune to the strains its policies are creating in markets from Turkey to China.

“The dollar debtors out there are all scrambling to find dollars and that contributes to the dollar strength,” said Joachim Fels, global economic adviser at Pacific Investment Management Co. But Fed rate hikes are gradually removing liquidity, “so the tide is going out and I think that will expose the weaknesses.”

Domestic Risks

The greenback’s recent bout of weakness also raises the question of how resilient U.S. assets will be in the face of domestic political risks, after President Donald Trump’s former lawyer pleaded guilty to federal charges. While the economic backdrop and policies that support further dollar gains remain in place, the resulting uncertainty may give pause to investors seeking refuge in the U.S.

The tension between global demand for safety and domestic challenges is evident in Treasuries. Buyers are still favoring long-dated debt in the face of record auction sizes as the U.S. seeks to plug an expanding budget deficit. Treasury bulls can cite geopolitical risks to support their case, as well as the threat to U.S. growth from tariffs.

So far, the economy is on solid footing, allowing the Fed to tighten monetary policy, while the Bank of Japan and the European Central Bank continue providing stimulus. Riskier U.S. assets have found support in corporate earnings growth of 25 percent this reporting period, which has driven the S&P 500 to record highs. In contrast, the MSCI emerging-markets index is down more than 17 percent from its 2018 peak.

‘Priced for Perfection’

“Things in the U.S. are priced for perfection,” said David Kelly, chief global strategist at JPMorgan Asset Management. “There’s been a bit of a failure to launch in the rest of the world. We thought that the good momentum last year would be maintained into this year, and that really hasn’t been the case for places like EM or Europe or even really Japan.”

U.S. credit markets seem particularly impervious to the forces buffeting global markets. But vulnerabilities may be building.

In investment-grade bonds, years of borrowing at cheap rates has fueled debt-driven mergers-and-acquisitions and weakened credit quality. The proportion of bonds in the lowest tier above junk in the Bloomberg Barclays corporate index has jumped to 53 percent, from 38 percent in 2007. The average spread in the corresponding high-yield index is within 30 basis points of the lowest in more than a decade. And as investors have piled into leveraged loans, a record proportion are accepting weaker protections.

Too Dear

American credit markets are too expensive, according to James Athey, senior investment manager at Aberdeen Asset Management, which has shifted much of its U.S. exposure to favor equities over the past year. Still, he finds the U.S. more insulated from geopolitical risks, and better equipped than its peers to fight the next economic downturn.

“When you look further afield, you see other countries which have similar but more acute and more concerning problems,” he said.

That said, the support for elevated asset prices may be tested soon. Fels is among analysts expecting U.S. growth to slow in the second half of 2018, and corporate earnings to weaken. The dollar’s strength could start to weigh on companies’ profits, Fels said, and the pro-cyclical policy of tax cuts and deregulation may prove to be a sugar high as the expansion enters its 10th year.

A few Fed officials also see fiscal stimulus as a potential headwind to growth, according to the minutes of the central bank’s latest meeting, which noted their view that "a faster-than-expected fading of the fiscal impetus or a greater-than-expected subsequent fiscal tightening constituted a downside risk."

Investors may not be ignoring these concerns, so much as struggling to measure them, as U.S. policy is in uncharted waters.

“Investors find it very difficult to deal with geopolitical risks in their portfolio construction,” Fels said. “It’s very different from other risks that investors deal with and are used to: interest-rate risk, credit risk and so on, where we have a lot of instruments to price them.”

The flow of cash could reverse if investors start to question whether they’re being adequately compensated for U.S. risks.

But so far, they’re not balking at the flood of deficit spending and an administration bent on upending longstanding norms. As global financial and geopolitical tensions mount, the money is still following the path of least resistance to its traditional haven.

--With assistance from Dan Wilchins and Benjamin Purvis.

To contact the reporter on this story: Emily Barrett in New York at ebarrett25@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Mark Tannenbaum, Jenny Paris

©2018 Bloomberg L.P.