Bears on the Run Again as S&P 500 Ends Drought With New High

Bears on the Run Again as S&P 500 Ends Drought With New High

(Bloomberg) -- For a few minutes, anyway, investors had permission to put the traumas of February and March behind them in stocks. Then Washington crashed the party and the celebration went back on ice.

The S&P 500 has come virtually straight down after peeking above its Jan. 26 high around midday Tuesday, as the legal entanglements of two former aides to President Donald Trump drained the market of cheer. More reversal than rout, the downdraft was still a blow for bulls who’ve waited six months to call the correction over.

“I don’t think this is going to create a lot of fear that will cause people to sell, but it will definitely force people to step back and refrain from buying,” said Matt Maley, equity strategist at Miller Tabak + Co. “Fewer buyers in a rather thin market can cause a further downside.”

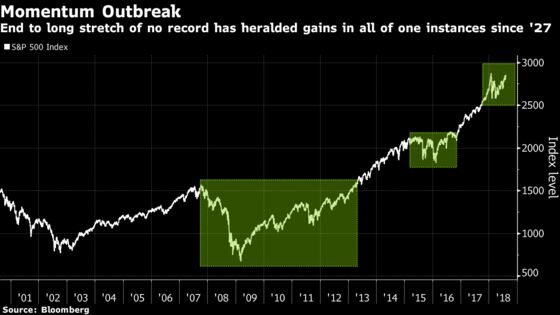

After spending 142 trading days without a record, the dry spell ended Tuesday as the S&P 500 climbed to a new intraday high of 2,873.23. The elevation had additional poignancy, arriving the night before the 9 1/2-year bull market becomes by some measures the longest in history.

Still, if you’re tempted to bail there may be reason to restrain the impulse. If history is of any guide, investors have often been better off ignoring the clustering milestones and hanging on, because buying stocks after a breakout has proved to be a winning strategy.

Since 1927, the S&P 500 has endured 17 other prolonged stretches without records. After the drought ended, all but one saw stocks go higher over the next 12 months. On average, the index rose 13 percent, compared with 7.7 percent over any one-year period.

“There is a lot of talk about the end of cycle and how close it is,” said Andrew Hopkins, head of equity research at Wilmington Trust Co., which oversees more than $80 billion. “But from an economic standpoint, it doesn’t look like that way. It looks like we’re still in pretty solid shape.”

Indeed, U.S. gross domestic product expanded at the fastest pace in four years during the April-June period and corporate America just posted two quarters of 24 percent profit increases. The buoyancy is in stark contrast with the rest of the world, where the MSCI Emerging Market Index is down 18 percent from its peak and the Stoxx Europe 600 index is headed for its third monthly decline in four.

The resilience has done little to mute bears, who say growth is peaking and a confluence of forces -- from rising interest rates to a potential global trade war -- threaten to derail the economy.

While the market is near uncharted territory, the euphoric buying that drove stocks to one of the best starts of a year is nowhere to be found. Over the past month, investors put $15 billion into exchange-traded funds that focus on U.S. stocks. That compared with $40 billion during January.

Rather than relentlessly chasing winners, investors are slowly rotating money out of darling companies, such as tech giants, and into laggards like drug makers and industrial conglomerates. A preference for safety is creeping back, with consumer staples and health-care shares leading the market over the past two months.

As a result, fewer stocks are flagging momentum warnings. At Monday’s close, 67 members in the S&P 500 posted readings above 70 in their 14-day relative strength index, one third of what was seen seven months ago.

“I would be more concerned if there weren’t worries in the market. That would mean you get an euphoric blow-off,” said Malcolm Polley, who oversees $1.2 billion as president and chief investment officer at Stewart Capital Advisors LLC in Indiana, Pennsylvania. “The fact that there are worries means people are realistic in their assumptions,” he said. “The market always climbs a wall of worries -- always.”

Skepticism has been the signature characteristic of this bull market. Since the rally began in March 2009, fear has been a constant companion, from Europe’s debt crisis in 2010 to the downgrade of U.S. sovereign rating in 2011 and China’s currency devaluation in 2015. Now it’s fear of peaking growth.

Yet, what hasn’t killed this bull market has usually made it stronger. Five 10 percent corrections later and $300 billion pulled out of U.S. equity ETFs and mutual funds, the decade-long advance just equaled the No. 1 title from the one during the dot-com era.

Is it closer to the end of the cycle than to the start? Sure, nobody doubts that. And there are tangible signs that equity valuations are getting stretched. Sure, the S&P 500 trades at 2.2 times sales, in line with the peak levels seen in 2000. But look at the median price-sales ratio for the index’s members, which strips out market-cap bias: it’s twice as high. In other words, overvaluation was highly concentrated to tech giants in the years of internet frenzy. Right now, everything is expensive.

While bulls take comfort in forecasts for sales and profits to keep rising over the next two years, helping ease the multiple pressure, skeptics find fault in the downward slope of the growth trajectory. Both S&P 500 revenue and earnings will increase at roughly half this year’s pace in 2020, according to analyst estimates compiled by Bloomberg.

“The earnings and economy growth were better. The question is, can you do it again?” said Paul Christopher, head of global market strategy at Wells Fargo Investment Institute.

Bailing out too early can be costly. A study by Bank of America Corp. on market peaks since 1937 shows that being uninvested in the last year of an advance meant foregoing one-fifth of the rally’s overall return. While every episode is different, that math roughly translates into additional 550 points in the S&P 500, if the bull market goes on for another year.

Rather than worrying over what could trigger the next drawdown, investors should focus on things that could drive the market higher, according to Steve Auth, chief investment officer of equities at Federated Investors Inc. His list of positive catalysts include: persistently subdued inflation, a signal from the Fed to end rate hikes, easing trade tensions, and a lasting trend in better-than-expected economic and earnings data.

Bears “may be waiting in vain” for the next selloff, Auth wrote in a note to clients this month, reiterating his call for the S&P 500 to end the year at 3,100. “Stocks running out of excuses for not going up.”

To contact the reporters on this story: Lu Wang in New York at lwang8@bloomberg.net;Elena Popina in New York at epopina@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2018 Bloomberg L.P.