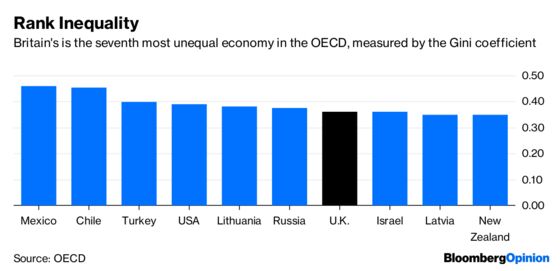

(Bloomberg Opinion) -- The Brexit vote hasn't had much of a leveling effect on Britain’s inequality problem, despite Prime Minister Theresa May’s promises to the contrary. The fat cats are getting fatter, to borrow the language of Jeremy Corbyn.

The average compensation of CEOs at the U.K.’s top 100 firms jumped by 23 percent between 2016 and 2017, according to the High Pay Centre, a think tank. Rank-and-file employees, meanwhile, fared less well: CEOs earned 145 times more than their average worker in 2017, up from 128 times in 2016.

Dig a little deeper into the figures, and it’s clear that they are skewed by lop-sided incentives programs at two companies in particular: Homebuilder Persimmon Plc, which handed its CEO 47.1 million pounds ($60 million) last year, and Melrose Industries Plc, where the boss walked away with 42.8 million pounds.

Both companies offered their leaders long-term incentive plans linked to stock-price performance whose overly generous nature only became obvious, well, over the long term. Strip out these two and the increase in mean CEO pay is a less generous 6 percent.

Shareholders are waking up to their responsibility in this matter. Investors were the ones who waved through pay structures that offered a lot of potential upside without the necessary checks and balances. Now they’re stirring: In February, Persimmon’s board agreed to limit executives’ windfall and promised to cap future payouts. Of the shareholders who voted, almost a quarter opposed Melrose's pay plan.

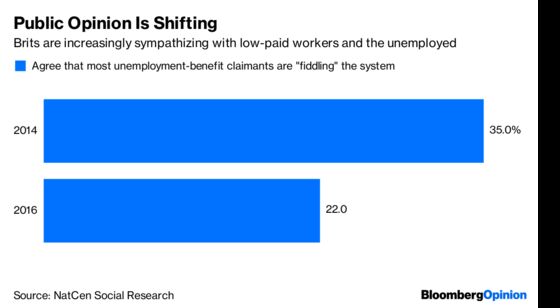

These are just slaps on the wrist — but they point to growing pressure from the court of public opinion. Attitudes toward pay inequality are hardening, while sympathy for nurses, low-wage staffers and the jobless is growing.

A wide corporate gender pay gap is seen negatively by 53 percent of people, according to opinion polling company YouGov, while the proportion of people who think unemployment benefit claimants are dishonestly fiddling the system has hit its lowest level in 30 years, according to NatCen Social Research.

New measures to force businesses to disclose more about their remuneration policies will ramp up the pressure. The fact that May’s traditionally pro-business Conservative Party is forcing companies to disclose and justify the ratio between the pay of their CEOs and their workforce shows how politics has changed. Blunt as these statistics may be, BlackRock Inc. has asked boards to take them into account when setting executive pay.

Life should also be getting tougher for CEOs trying to hit performance targets. Interest rates are marching higher, and the U.K.’s Help-To-Buy property program — a subsidy that propped up not just house prices, but the profits of builders and developers too — is slowly being phased out. Stocks in the FTSE 100 Index are increasingly volatile, giving investors more reason to scrutinize where the rewards are going.

Brexit is the big wild card. As I wrote earlier this year, the pound’s weakness has been a boon for big, international FTSE 100 firms — inflating the value of their overseas revenue — while domestic firms and their staff find life getting more expensive.

But again, investors can still have an impact on the quantum of CEO pay — note last year’s shareholder revolt against BP Plc, which forced the oil giant to cut the maximum bonus CEO Bob Dudley could earn.

And if a messy and painful Brexit pushes the British public into the arms of the Corbynites, it will be the flush global firms that feel the pinch. The pressure has only just begun.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Lionel Laurent is a Bloomberg Opinion columnist covering finance and markets. He previously worked at Reuters and Forbes.

©2018 Bloomberg L.P.