Cracks Form in Foundation of Chipmakers’ Advance: Taking Stock

Cracks Form in Foundation of Chipmakers’ Advance: Taking Stock

(Bloomberg) -- Stock futures are ticking lower as investors digest disappointing results and financial forecasts from a handful of high-profile names. Deere & Co. shares are little changed pre-market after mixed quarterly numbers, but Applied Materials Inc. and Nvidia Corp. are sinking following lackluster guidance, which could crush the tech sector today. Markets in China and Europe slid amid lingering geopolitical uncertainty after Donald Trump pushed Beijing for a better trade deal. Turkish stocks are down for the fifth time in six days ahead of S&P Global Ratings’ decision on the country’s creditworthiness.

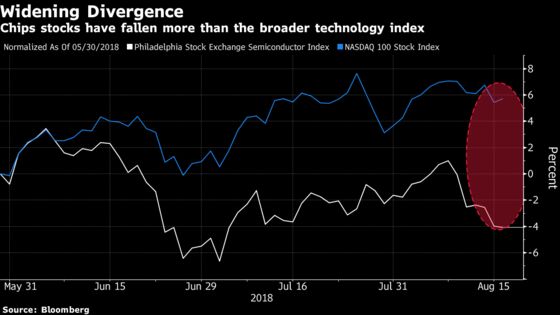

The calm of a seemingly uneventful session on Thursday (all industry groups rose on volume ~7% below this year’s average) was shattered by continuing weakness in chipmakers and a solid news-flow in retail. Semiconductors posted the fifth drop in six sessions on Thursday while most stocks in the Semiconductor Index traded in the red pre-market on Friday after Applied Materials and Nvidia, which both have exposure to cryptocurrency mining, posted disappointing guidance.

Applied Materials is one of the first suppliers chip firms turn to when they’re ramping up production, and the company’s revenue forecast that fell short of the lowest estimate widened concern the chipmaker’s growth may be peaking. Nvidia added to the gloom as it said it projects “no contributions going forward” from sales of graphics chips to miners of cryptocurrencies after anticipating it to be “meaningful for the year. Quarterly revenue for cryptocurrency-specific products was more than 5 times lower than the firm’s previous guidance.

It’s unclear what weighs on investor sentiment the most - weakening demand for chips, the effect of a trade war with China or a slide in cryptocurrencies, but it’s obvious that the recent pain in chipmakers is more pronounced than that in the broader technology group.

Meanwhile, EPFR Global data shows outflows throughout, with $2.6 billion for U.S. equity funds, $200 million in emerging markets, and $2.9 billion for Europe, marking the 23rd straight week of redemptions for that region and a whopping $39 billion since the start of 2018.

Retailers saw some of the widest swings among U.S. stocks on Thursday, all thanks to diverging earnings reports. Walmart (+9.3%) posted the fastest quarterly growth in the grocery segment in nine years, signaling Amazon’s push into the food business won’t be as smooth as some have expected. A pick-up in same-store traffic and sales growth in e-commerce business helped lift the stock the most in the S&P.

J.C Penney was investors’ biggest punching bag after the retailer posted weak earnings for the quarter and cut full-year guidance. Double-digit losses aren’t unheard of for the battered stock, but Thursday’s 27% rout was by far the largest ever. Analysts didn’t hold back their thoughts: Clearview Trading Advisors said the stock is “currently worthless,” an analyst at Credit Suisse cut the stock’s target price by half, and GlobalData’s Neil Saunders said JCP is in “no-man’s land.”

On Tap for Next Week

While most of the earnings season is over, a number of big retailers are yet to report earnings next week. Some of the most notable reports will come from TJX Companies, Kohl’s, Lowe’s, Target, L Brands and cosmetics giant Estee Lauder. Among Internet megacaps, Chinese giant Alibaba is the last one to report earnings. All eyes are on its profit outlook after peer Tencent posted the first profit drop in a decade, partly because Beijing froze approval of digital games the company needed to make money. The trio of Alibaba, Tencent and Baidu is seen as one of the most crowded trades among the U.S. investors, along with the FAANGs, according to Bank of America’s survey, a trade spat with the U.S. and slowing growth in China is taking a toll on the firm, which has lost almost 20 percent of its value since a June high.

Geopolitics is once again the center of attention in the next week: German Chancellor Angela Merkel and Russian President Vladimir Putin meet on Saturday to discuss Syria (though no major headlines are expected), and America’s 25 percent tariffs on an additional $16 billion in Chinese imports goes into effect (watch Caterpillar, Deere, Boeing and carmakers.)

In the deals world, analysts are awaiting Cigna shareholders’ vote on weather to approve the proposed acquisition of pharmacy benefit management giant Express Scripts at a general meeting scheduled for Aug. 24. Activist investor Carl Icahn said on Monday night he was dropping his effort to block the $54 billion takeover. Central bankers gather in Jackson Hole, Wyoming, for their annual policy summit, and the Federal Reserve releases minutes from its July meeting, at which officials left rates unchanged.

Notes From the Sell Side

JPMorgan cut Dean Foods to underweight, saying that there a number of concerns for the company including possible third-quarter earnings miss, higher raw materials costs, less demand for milks and shelf space erosion to alternatives to milk. Price target cut to street low $6 from $9 as JPMorgan still sees “meaningful downside ahead.”

Bernstein cut Hilton Worldwide to market perform as it expects U.S. RevPar and unit growth to decelerate over the next year, possibly faster than currently expected. Hilton price target cut to $83 from $93, while Marriott International’s PT reduced to $132 from $142 as slowing growth and lack of catalysts are likely to limit upside for both stocks. Room demand growth has been strong this year, but if demand grows slower than supply in 2019, support for pricing could “deteriorate quickly.”

Tick-by-Tick Guide to Today’s Actionable Events

- 10:00am -- University of Michigan Sentiment, Leading Index

- 10:00am -- DE earnings call

To contact the reporters on this story: Elena Popina in New York at epopina@bloomberg.net;Lily Katz in New York at lkatz31@bloomberg.net;Joshua Fineman in New York at jfineman@bloomberg.net

To contact the editors responsible for this story: Chris Nagi at chrisnagi@bloomberg.net, Steven Fromm

©2018 Bloomberg L.P.