CLOs Are the New Hedge Funds. Plan Accordingly.

CLOs Are the New Hedge Funds. Plan Accordingly.

(Bloomberg Opinion) -- A number of hedge fund firms have a hot product. It’s not their hedge funds.

Och-Ziff Capital Management’s investors withdrew $418 million from its hedge funds in the second quarter. Total inflow of assets under management, however, were $1.2 billion, its largest increase in assets in four years. The firm’s hot product: Collateralized loan obligations — a derivative debt investment that invests in leveraged loans and is a cousin of the type of funds that blew up in the housing bubble.

Like hedge funds, CLOs are supposed to be protected from losing money, particularly now. That’s because they invest generally in floating rate loans, which, unlike normal bonds, won’t lose money when interest rates rise. What’s more, CLOs have also had better returns than other asset classes this year, particularly hedge funds. The Palmer Square CLO Debt index was up 2.5 percent in the first seven months of the year, compared with 1.5 percent for hedge funds, according to Hedge Fund Research Inc.

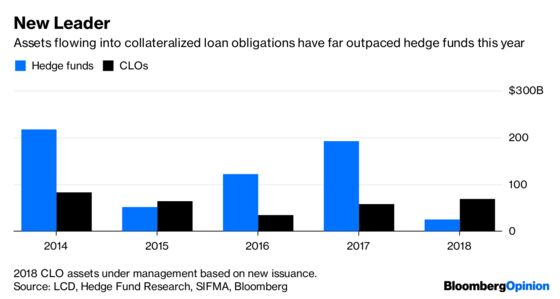

As a result, CLOs, which are also managed by private equity firms as well as other more specialized debt investors, have become one of the hottest products on Wall Street, with inflows continuing to pick up this year, leaving hedge funds far behind. Just more than $69 billion in CLOs — which are like funds but raise money like bonds — were issued in the U.S. in the first half of the year, according to S&P Global Market Intelligence’s LCD. An additional $9.7 billion flowed into the credit derivatives in July. And last month, Wells Fargo predicted that U.S. CLO issuance would hit $150 billion this year, a record.

On the other hand, assets under management for hedge funds rose by less than half that, or $25 billion, in the first half of 2018, according to HFR. Hedge funds are still much bigger in total, with $3.2 trillion in assets compared with just less than $600 billion in CLOs. But the investment flows to CLOs, and away from hedge funds, turned this year. Last year, hedge funds increased their assets under management by $192 billion, more than three times the $57.8 billion increase in CLOs.

CLOs are not new. They were around during the financial crisis, and survived, even though they invest in risky loans. And when described as cousins of collaterlized debt obligations, which is true, many on Wall Street see that as an unfair tarring. Investing in corporate debt as CLOs generally do, even riskier corporate debt, is different from investing in subprime housing debt. And few CLOs appear to be based on synthetic debt, or structures similar to CDO-squareds, which were CDOs made up of the riskiest portions of other CDOs.

But there is a risk to any market that comes with being the investment of the moment. That may go double for CLOs, which are not only hot themselves but invest in leveraged loans, where issuance is also growing as well. And there does seem to be some tell-tale signs of a bubble in CLOs, like when former critics change sides. Earlier this year, Morningstar Inc. warned that CLO managers’ push to boost returns had led to weaker deal structures. This week, those same researchers said many lower-rated CLOs may in fact be less risky then their BBB or BB grades imply.

Critics that remain warn that CLOs weathered the financial crisis because they were invested in corporate, not consumer, debt. If corporate loans turn out to be the big problem in the next downturn, then CLOs may not prove as bulletproof as the last time around, especially after a number of years in which companies have been taking on more debt relative to their assets. Safeguards and covenants, too, appear to have weakened in corporate loans. All this comes when a growing number of investors are warning that the corporate loan market might be stretched.

And remember, many people thought once upon a time that hedge funds, because they were hedged, wouldn’t lose money. That didn’t prove true. It won’t for CLOs, either.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2018 Bloomberg L.P.