Turkey Is Too Much of a One-Off to Undermine Emerging-Market Strength

Investors cut their exposure to emerging markets as a whole to offset losses in Turkey, or to hedge lira positions.

(Bloomberg) -- Emerging markets rocked by Turkey’s financial turmoil may keep sliding in the days and weeks to come, but will probably withstand the carnage without too much more pain.

Fear of contagion surfaced Monday as the lira extended a two-day slump to about 20 percent, reaching a new low and spurring panic selling of peers including South Africa’s rand, Mexico’s peso and India’s rupee. Investors cut their exposure to emerging markets as a whole to offset losses in Turkey, or to hedge lira positions.

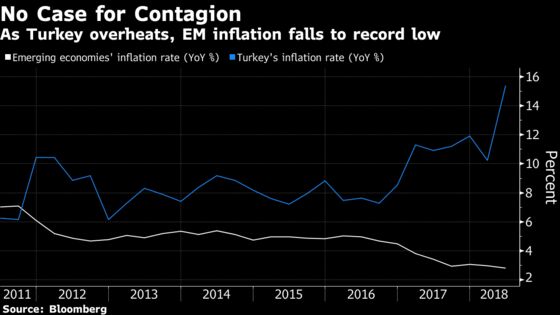

Yet beyond the immediate future, there are few fundamental reasons to lump other emerging markets in with Turkey. With average inflation rates at record lows and current-account balances improving, the developing world is diverging from Turkey. The dichotomy could limit the spillover.

“It can be contained to just Turkey because there aren’t really any other emerging markets that have exactly the same toxic blend that Turkey has,” Paul McNamara, a London-based fund manager at GAM UK Ltd., said in a Bloomberg Television interview. “Only Argentina really has the external deficit, and they don’t have as much domestic debt.”

The core problem in Turkey is runaway inflation that undermines real returns. Average inflation in emerging markets is at a record low of 2.81 percent, which has raised mean real yields by more than 4 percentage points during the past seven years. That isn’t much of an argument for a sustained selloff.

Investors continue to penalize markets where policy makers haven’t done enough to rein in deteriorating current-account balances and spiraling inflation. With Turkey’s inflation at 15.9 percent and Argentina’s at 29.5 percent, the lira and peso have been the worst performers this year.

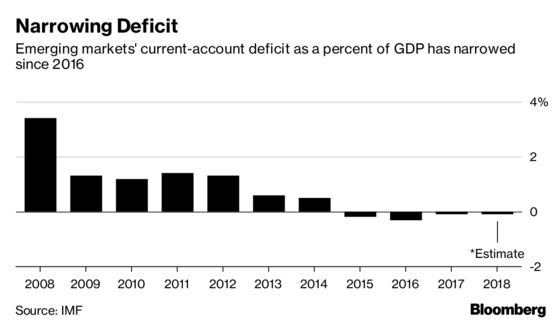

But current-account balances are improving elsewhere. Even amid a drop in China’s surplus and tighter funding conditions because of higher U.S. interest rates, deficits have narrowed since 2016, according to International Monetary Fund figures. Some countries, such as Thailand and Taiwan, have strong positive balances, helping their currencies outperform most of their peers in the past week.

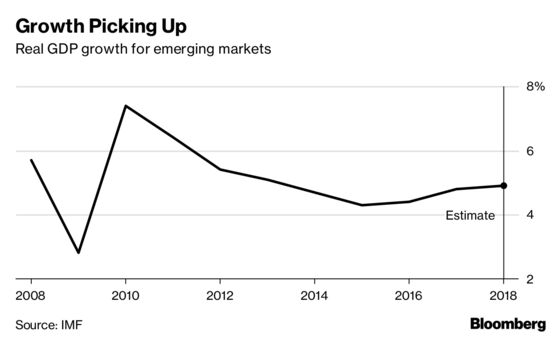

In pursuing growth at the cost of financial stability, Turkey stands alone in the emerging world. Growth in some of the fastest-expanding economies, such as India and China, is orderly, if real gross domestic figures are any indication. The average real GDP has been on the upswing for three years, offering the most compelling argument for emerging-market exposure.

That’s unlikely to come under threat should Turkey head for a hard landing. The nation accounts for just 0.7 percent of MSCI emerging-market indexes.

None of that rules out Turkey acting as a drag on other markets in the short term. Many portfolios still treat emerging economies as a homogeneous asset class that could be shamed by association.

“Our big worry is if Turkey really goes into a major, major crisis and they impose capital controls,” McNamara said. “That’s the sort of thing that brings the asset class into sort of disrepute.”

To contact the reporters on this story: Netty Ismail in Dubai at nismail3@bloomberg.net;Filipe Pacheco in Dubai at fpacheco4@bloomberg.net

To contact the editors responsible for this story: Dana El Baltaji at delbaltaji@bloomberg.net, ;Rita Nazareth at rnazareth@bloomberg.net, Srinivasan Sivabalan, Alec D.B. McCabe

©2018 Bloomberg L.P.