Credit Market’s ‘Eyeball Valuations’ Raise Investors’ Eyebrows

Credit Market’s ‘Eyeball Valuations’ Raise Investors’ Eyebrows

(Bloomberg) -- Around the start of the millennium, high-flying dot-coms said their companies were worth hundreds of millions based on unusual yardsticks like how many viewers were looking at their websites.

In frothy debt markets now, companies want credit for their Instagram followers.

Firms like ride-sharing company Uber Technologies Inc., cosmetics maker Anastasia Beverly Hills and electric carmaker Tesla Inc. are telling debt investors to set aside the fact that future profitability may weaken or that they may not be earning profit at all, and to focus instead on the growth they’re planning, their high equity valuations and the outside cash they’ve raised.

Some investors may be skeptical, but enough are buying the debt to get deals done. The demand shows how willing money managers are to take risk even in what is widely seen as the late stages of an economic expansion, when the worst deals are often made. If fund managers aren’t careful, they are bound to lose out as interest rates march higher and newer companies struggle to meet their obligations.

“Things like clicks don’t pay bond interest," said Scott Roberts, head of high-yield investments at Invesco Ltd., which manages $963 billion. "We have to keep in mind that companies are doing whatever they can to lower their cost of capital.”

“Community Adjusted”

Earlier this month, Anastasia Beverly Hills won a $650 million loan in part by touting its more than 17 million Instagram followers, which cuts its marketing costs. Uber lost $4.5 billion last year, but took out a $1.5 billion loan in March after it bruited about its app penetration rate, a measure of how many people had downloaded its app and will potentially give it revenue.

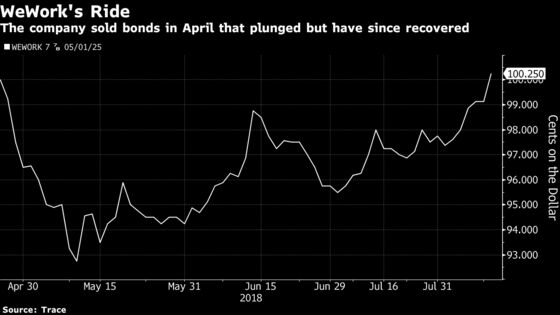

When WeWork Cos. tapped the junk bond market in its first sale in April, it created a new adjusted metric for the cash it would have available to pay interest on its debt. The "community-adjusted earnings before interest, tax, depreciation and amortization" measure was meant to reflect its earnings excluding the cost of growing. Representatives for Tesla and WeWork separately declined to comment. Representatives for Anastasia Beverly Hills and Uber didn’t return calls seeking comment.

The WeWork measure amounted to a gain of around $233 million last year, even as the company’s adjusted Ebitda, a more traditional debt metric, was a loss of $193.3 million, according to bond documents obtained by Bloomberg. The company’s bonds dropped more than 7 percent in the weeks after being issued, but have since climbed back above their face value in part because of another $1 billion investment from SoftBank Group Corp.

There are key differences between the dot-com era and now. Anastasia, for example, generates profits, and investors’ fear is more that its sky-high profit margins will start to narrow as it tries to grow. And companies like Netflix Inc. can probably generate positive cash flow from their operations by investing less in expansion. A representative for Netflix didn’t return an email seeking comment.

“You can get comfortable with cash burn if it’s contributing to increases in earnings or building an asset base that that significantly covers the company’s debt," said John Yovanovic, global head of high-yield at Pinebridge Investments, which manages $87 billion.

Historically, companies struggled to borrow in the bond or institutional loan markets if their Ebitda wasn’t positive. That’s changing, as leveraged finance investors become open to less mature companies. Tesla, for example, sold $1.8 billion of junk bonds last year even though its Ebitda had been positive for only four of the last 11 quarters, according to data compiled by Bloomberg. The company has since posted another four quarters of losses by that measure, and Chief Executive Elon Musk is talking about taking the company private.

‘Earned Media’

For Anastasia Beverly Hills, the company used its Instagram followers and other measures of its social media clout to explain why its marketing costs were low, and would stay low. Where other beauty companies pay for expensive celebrity endorsements and advertising in fashion magazines, Anastasia focuses on social media. The company said that an independent marketing technology consultant, Tribe Dynamics, said that Anastasia generated more "earned media," or mentions from fans, customers, and others, than any other beauty company, including Estee Lauder Cos Inc.’s MAC Cosmetics and L’Oreal SA’s NYX Cosmetics.

“Unless you are a Gen Z or a Millennial, you may or may not know about Anastasia," said Chedly Louis, senior credit officer at Moody’s Investors Service. “The company may have to increase spending on marketing, but that spend will still be significantly less than big cosmetic rivals."

Equity, Cash

High equity values and cash levels at these firms are helping debt investors look beyond potential trouble. Tesla, for one, has a market capitalization of about $60 billion, implying it could sell equity if it had to raise cash to pay debt. Uber’s is also above $60 billion and it had some $6 billion of cash at the end of the first quarter. WeWork, which has sought to raise equity at a $35 billion valuation, had $2 billion of cash when it launched its bond proposal. These companies are burning through cash as they invest in growth, but they can dial down that expenditure when they need to preserve cash.

Even so, as investors learned in the dot-com bubble, equity valuations can plunge fast. Pets.com famously went from IPO to liquidating itself in less than a year. The alternative valuation metrics of that era, like “eyeballs,” “monthly unique visitors” and “stickiness” looked idiotic by late 2000.

Bond investors are trained to be skeptical because their potential losses on bad investments usually far outweigh their possible gains on good ones. But after one of the longest economic recoveries on record, skepticism can fade. There’s more than $9 trillion of corporate bonds outstanding now, up about 50 percent from 2009. The market for loans to junk-rated borrowers now tops $1 trillion, and startup companies are getting loans earlier and earlier in their lives.

Awash in debt, investors can lose discipline. But lowering standards now will haunt money managers later, said Mike Terwilliger, portfolio manager at ResourceAlts.

“When the downturn happens, some of those creative interpretations of valuations fall away,” he said. “That can get pretty ugly."

To contact the reporters on this story: Claire Boston in New York at cboston6@bloomberg.net;Lisa Lee in New York at llee299@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Sally Bakewell, Dan Wilchins

©2018 Bloomberg L.P.