In a U.S. Mall Owner’s World, ‘Boring’ Is Actually Pretty Good

In a U.S. Mall Owner’s World, ‘Boring’ Is Actually Pretty Good

(Bloomberg) -- Mall landlords, besieged for the past two years by the rise of online shopping, are trying to push a new narrative of improving sales and increased demand for empty space at their properties.

Second-quarter earnings results for the biggest owners were largely in line with expectations, according to DJ Busch, an analyst at Green Street Advisors LLC, a research firm that specializes in real estate investment trusts. And that’s good news for an industry that’s struggling to stay relevant.

“We are pleasantly surprised -- boring is pretty good in retail,” Busch said. “Incrementally, we’re moving in the right direction, but it’s going to take several quarters to get back to speed and get some of these centers leased backed up.”

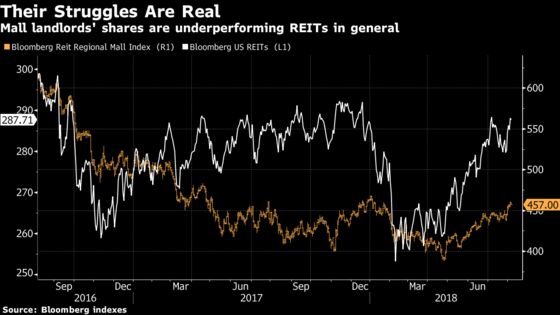

U.S. mall REITs have been beaten up as the growth of e-commerce and a surge in retailer bankruptcies and store closures upends their business model. In the past 24 months, a Bloomberg index of eight regional-mall owners plunged 25 percent through Monday, compared with a 3.3 percent decline for all REITs. After a brutal 2017, landlords are trying to paint a rosier picture and convince investors that the worst is behind them.

“Demand from tenants for space in our highly productive centers is increasing,” David Simon, chief executive officer of Simon Property Group Inc., the largest U.S. mall owner, said on a call with analysts last week. “We continue to redevelop our irreplaceable real estate with new, exciting, dynamic ways to live, work, play, stay and shop that will further enhance the customer experience.”

The strong economy is helping prop up sales numbers, according to Busch. Simon’s sales per square foot, a key metric for mall owners, increased 4.6 percent from a year earlier to $646. For Santa Monica, California-based Macerich Co., sales per square foot rose 7.1 percent to $692. Macerich and Simon, based in Indianapolis, own some of the best malls in the country, the so-called A malls that industry analysts maintain will be able to weather the tumult.

“We never panicked over the whole retail craze last year,” said Alexander Goldfarb, an analyst at Sandler O’Neill & Partners. “It was completely overdone.”

Troubled Retailers

Not everybody is as sanguine. The backdrop for mall landlords remains challenging. The effects of the Toys “R” Us collapse are still filtering through, and troubled retailers continue to go bust, even if the pace has slowed. Last week, Brookstone Inc., a purveyor of novelties such as massage chairs and foot spas, filed for bankruptcy and said it’s closing all of its mall locations.

“We remain skeptics about the pace of market rent growth,” SunTrust Robinson Humphrey analysts led by Ki Bin Kim said in a note last week. “We fully understand that A malls will not go away, there is healthy need for A malls, but it doesn’t mean they will be unscathed.”

Occupancy remains the Achilles’ heel for landlords, falling for all mall trusts in the second quarter except Pennsylvania REIT, which had a slight increase from a year earlier, Busch wrote in a report this week. Most companies said they expect declines to moderate later in the year as they re-lease space left behind by failed stores, but owners of lower-end properties will be more challenged, according to Busch.

For better or worse, lease-termination fees -- paid by tenants to get out of rental obligations early -- emerged as a material quirk in the numbers for several landlords. Macerich lowered it 2018 earnings forecast due to a projected $7 million reduction in lease-termination income. On the opposite end of the spectrum, Philadelphia-based Pennsylvania REIT, whose malls typically aren’t considered top-tier, said a $5.2 million gain in such income lifted its results in the second quarter.

--With assistance from Lily Katz.

To contact the reporter on this story: Sarah Mulholland in New York at smulholland3@bloomberg.net

To contact the editors responsible for this story: Daniel Taub at dtaub@bloomberg.net, Christine Maurus

©2018 Bloomberg L.P.