Bond Market Bears Are in for a Nasty Surprise

Bond Market Bears Are in for a Nasty Surprise

(Bloomberg Opinion) -- Between the punditry and desire to be smarter than everyone else, market participants often come up with ideas that supersede the evidence. As a result, they tend to miss the developed story right in front of them. That's especially true in the bond market right now, where it seems almost everyone has a bearish outlook. Even JPMorgan Chase & Co. Chief Executive Officer says there's a higher probably than most think that Treasury 10-year yields will rise to 5 percent from about 3 percent currently.

I had a lunch with a journalist the other day where we compared notes on what we read, who was saying what, and how confident bulls, bears and pigs were about their views. That last part is really a function of what do we know with a high degree of confidence and how do we position accordingly?

First is the Federal Reserve. The central bank is raising interest rates and withdrawing the liquidity created by its quantitative easing programs. Further rate hikes have the cover of decent economic data, and perhaps the incentive to get ahead of the stimulative impact of tax reform and inflationary consequences of tariffs. As a given, increase in short-term rates tend to flatten yield curve. Also, there's the added bonus that higher rates give the Fed room to ease that much more when the time comes. Motivation, we concurred, is less important than intent.

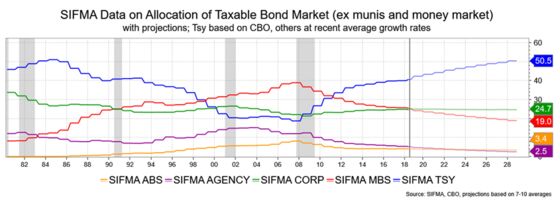

Second, we agreed that financial market structures have changed empirically, but are not high on people’s list of motivational causes. Between the diminished issuance from the likes of the structured credit crowd (including Federal agencies) and rising budget deficits, U.S. Treasuries are a much higher component to the bond market and their influence is rising sharply. In other words, an index contains a higher proportion of Treasuries today than it did pre-financial crisis and the percentage will rise for the next decade at least. In 10 years, Treasuries will constitute over 50 percent of the bond market from 40 percent currently. That means index funds and related benchmark followers will need to buy Treasuries.

Plus, the average maturity of those Treasuries has been rising and will probably continue to increase. After all, a flat yield curve is a big incentive to borrow for longer terms, and the interest in 40- or 50-year U.S. debt may emulate the strong demand seen in foreign markets.

We also noted that the market for investment-grade corporate bonds has changed. Debt rated BBB makes up half that market, up from about 38 percent just six years ago and causing the credit quality of a typical index fund focused on such bonds to drop and, thus, poised for a more difficult time in the next downturn. More risk, in other words, in this part of the market.

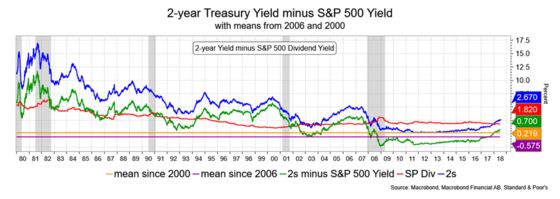

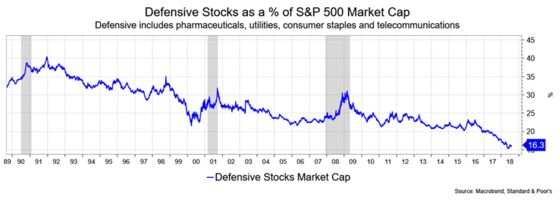

The stock market's appeal is diminishing relative to bonds. Two-year Treasuries yield 70 basis points more than the S&P 500 Index dividend yield, the most in a decade and well above the mean from 2000 or 2006. Yes, the spread is considerably less than longer-term norms, but then the S&P 500 has changed as well. The index has become less exposed to defensive stocks. High dividend paying companies made up 40 percent of the S&P 500 in 1991 and the dividend yield was about 3.16 percent. Today, defensive stocks account for 16 percent of the index and generate a 1.82 percent yield. That's not going to increase even as two-year Treasury yields increase in response to the Fed's rate hikes. It also means the S&P 500 will be less defensive in a downturn.

We now know the U.S. economy had a strong second quarter, but the bond market hardly budged. This tells us the market doesn’t buy its sustainability, and that a subdued pace is more realistic. The Trump administration's economic agenda has largely been set, and the market’s is showing patience to see what it can deliver while reacting with a “yeah, whatever” to the tweeting and hyperbole coming out of the White House.

Going back to the start of this column, if we trade on the thing stated as knowns, logic follows that the trends in place will hold for the rest of the year. Volatility will provide opportunities to trade, but not mark a new direction even though market participants will jump at blips hoping they prove to be more. I think the they will warrant simply another “yeah, whatever” for some time to come.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Ader is chief macro strategist at Informa Financial Intelligence. He was the No. 1 ranked U.S. government bond strategist by Institutional Investor magazine for 11 years. He was also ranked #1 5 years for Technical Analysis. David writes for Bloomberg Prophets and Barron Magazine. He also is a frequent guest on Bloomberg TV and Radio.

©2018 Bloomberg L.P.