China Explorer Cnooc May Reward Investors Even If Oil Won't

Chinese Explorer Cnooc May Reward Investors Even If Oil Won't

(Bloomberg) -- Chinese offshore oil giant Cnooc Ltd. may have more to offer equity investors betting on the recovery in global crude prices, even if the rally appears to be taking a bit of a breather.

The state oil company boasts vast reserve potential and a robust track record in cost cutting -- making it better positioned to tap strong oil prices than most of its regional rivals such as Australia’s Woodside Petroleum Ltd., Inpex Corp. of Japan and Thailand’s PTT Exploration & Production PCL, according to analysts and data compiled by Bloomberg.

Yet Cnooc is still trading at an around 30 percent discount to those peers, partly reflecting investor disappointment over its first-quarter revenue and concern over its status as a national oil company, while indicating it may have been undervalued. The stock has a potential to gain about 29 percent over the next 12 months, the most among Asian oil and gas producers after India’s Oil & Natural Gas Corp., according to analysts’ price targets compiled by Bloomberg.

“Cnooc is a low-risk play on a bullish oil price view,” said Laban Yu, an analyst at Jefferies Group LLC in Hong Kong. The stock is “absurdly cheap” compared with international majors such as Exxon Mobil Corp. and Chevron Corp, he added.

Cnooc -- which gets almost all its earnings from exploration and production of oil and gas -- tracks closely crude’s rise and fall. Prices have staged a comeback since the 2014-2016 slump, first as OPEC restrained output and more recently amid concern about supply disruptions from countries such as Libya, Iran and Venezuela. While there are signs the rally is cooling, benchmark Brent is still more than double its nadir below $30 a barrel, and Cnooc is reaping the benefit as shares and profits rebounded.

Cnooc’s shares have gained about 12 percent in Hong Kong this year to HK$12.52 as of Monday, extending two annual gains. It’s trading at 8.9 times its forecast 2018 earnings, below the 15.4 for its major peers in the Asia Pacific region. Of the 22 analysts covering the stock, 19 had the equivalent of a buy rating and none called for a sell.

The company may post a more than 60 percent surge in first-half net income from a year ago when it reports financial results later this month, according to estimates in a Bloomberg survey. In the past year, Cnooc’s earnings growth have trounced 93 percent of its regional peers, and 79 percent in terms of sales, according to data compiled by Bloomberg.

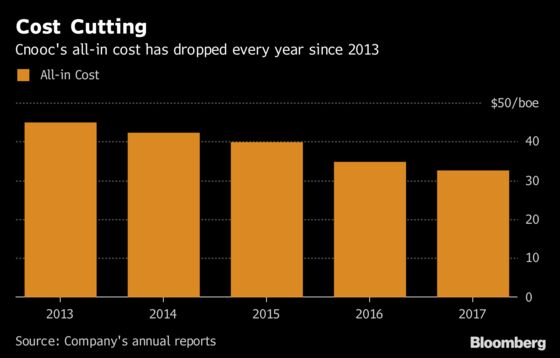

Even as prospects for further gains in crude are limited, the company’s cost cutting and higher spending on exploration and production projects will probably bolster earnings. Cnooc’s all-in cost has declined every year since 2013 to $32.54 per barrel of oil equivalent last year, according to its annual reports.

The Beijing-based explorer is targeting capital expenditure of between 70 billion and 80 billion yuan ($10.2 billion to $11.7 billion) this year, the highest since 2014. It’s also aiming to produce 500 million barrels of oil equivalent by the end of the decade, with 42 percent coming from overseas, from 469 million barrels last year.

Cnooc’s proved reserves -- a gauge of future earnings potential -- rose by a quarter to about 4.84 billion barrels of oil equivalent at the end of 2017. Its reserves are set to expand further, largely due to contribution from the Stabroek Block in Guyana, the world’s biggest new deepwater project in which Cnooc has a 25 percent stake.

Exxon, operator of the project, raised estimates of its discovery by 25 percent, saying last month the find could now produce 4 billion barrels of oil. Goldman Sachs Group Inc. has cited reserves from the project as reasons for its buy rating on Cnooc.

“We still see Cnooc as the essential oil to own in the sector,” Goldman’s Hong Kong-based analysts including Mark Wiseman wrote in a July 29 note, adding that the Guyana discovery is overlooked. The bank will seek an update from the company on its reserve life and progress of international projects at its first-half results release.

Naturally, with Cnooc’s fortunes so wedded to oil, any potential slump in prices could hurt its shares. Citigroup Inc. has outlined a scenario where the company’s shares may slide to HK$11.80 if Brent were to fall to $45 a barrel next year. The reverse holds true as well: should oil climb to $85, Cnooc would jump to HK$19.90, Citigroup said in a July 19 note.

So far this year, the global benchmark has traded at about $72. Brent is expected to average $66 next year, according to the median estimate of eight forecasts compiled by Bloomberg in the past month.

“Cnooc has underperformed the China oil sector average on concerns of lower production volume guidance and reserve writedowns,” Citigroup said in the note. “With these concerns behind us, and with the company’s excellent cost control track record and strong cash flow position, the stock looks well positioned to outperform.”

--With assistance from Matt Turner.

To contact the reporter on this story: Aibing Guo in Hong Kong at aguo10@bloomberg.net

To contact the editors responsible for this story: Charlie Zhu at qzhu46@bloomberg.net, ;Ramsey Al-Rikabi at ralrikabi@bloomberg.net, Jasmine Ng

©2018 Bloomberg L.P.