The Hidden Reason Why Hedge-Fund Returns Are at Risk

One Hidden Factor Has Been the Downfall of Hedge-Fund Returns

(Bloomberg) -- Smart money is blindsided by a flaw of its own making hiding in plain sight -- an investing maxim quants have known for an age.

Blame bets on volatility.

Research from Robeco Asset Management’s David Blitz concludes hedge funds have hitched their wagon to stocks with large equity-price swings -- a misguided strategy over the long haul.

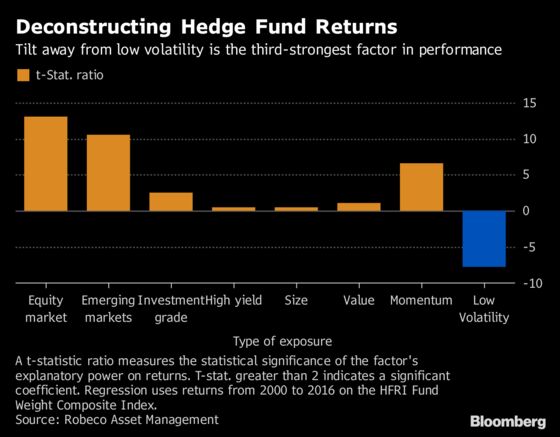

Not only have high-volatility shares massively underperformed low-vol peers, this outsized exposure to the high-octane cohort is one of the strongest explanations for hedge-fund performance, according to Blitz.

The sweeping study crunched industry returns from 2000 to 2016, and concluded funds overall have negative exposure to a long-short version of low volatility.

“The fact that hedge funds are positioned like investors in high-volatility stocks, this does not contribute positively to their returns,” the Rotterdam-based head of quantitative equity research said in an interview. “They would likely have been better off if they had chosen not to bet against the low-volatility anomaly."

A tilt away from the low-volatility factor ranks among the top three drivers of fast-money performance, alongside the broader index itself and emerging-market exposures, according to Blitz.

Efforts to deconstruct active-manager returns are in part the founding principle behind factor investing, one of the most popular quantitative strategies -- with Blitz a key proponent of the low-vol variety.

Academics have long discovered that most equity alpha is extracted from sources other than bets on the prospects of an individual company. Rather, successful managers pick stocks that share common factors, like momentum or earnings growth, that reliably beat the market over time.

From there, the low-volatility factor was born. Today, it’s a booming industry. Along with its inclusion in factor funds offered by Robeco and other quant giants like AQR Capital Management, smart beta exchange-traded funds focused on the investing style have $53 billion in assets.

Sure, there are periods where low-vol underperforms. This year, a calmer version of the S&P 500 has lagged the broader benchmark by over 2.5 percentage points. Yet quants point to its long-term success. Since 2000, the factor has bested the S&P 500 by a whopping 119 percentage points.

Hedge funds, it would seem, have missed the memo. Maybe it’s for good reason.

Managers succeed by locating overlooked companies, that while unpredictable and volatile, may eventually turn out large gains, said Benjamin Dunn, president of the portfolio-consulting practice at Alpha Theory.

“You need earnings variable to really drive alpha and have an edge over other investors,” Dunn said. “You’re not going to pay someone 2 and 20 to be long General Mills.”

Low-Vol Risk

Explicitly tracking the low-vol factor also comes with its own challenges, especially overcrowding. In 2016, a volatility blow-up was blamed on investors who piled into the strategy and then rushed for the exits. More recently, JPMorgan Chase & Co.’s 2018 outlook flagged richly priced low-volatility stocks as a source of equity-market risk.

“We’ve had a lot of questions from clients asking if this low-volatility factor was being arbitraged away, because you’d expect it to disappear if more people are exploiting it,” Blitz said. “But on the other side of the trade seems to be $3 trillion in hedge-fund assets.”

Since Robeco’s study looked at aggregate returns and not individual holdings, it is possible that some funds do track low volatility. But not enough to sway the total bias.

As for why hedge funds gravitate toward stocks with large swings, Blitz blames performance fees that incentivize managers to take riskier bets.

It’s a tad ironic. More so than most other active managers, hedge funds are in a prime position to take advantage of the low-vol anomaly. For example, they have fewer leverage constraints, so can buy the boring stocks, deploy debt, and post higher returns.

“If someone is trying to exploit it, it should be hedge funds,” Blitz said. “At least some positive exposure to low volatility, and not the other way around.”

To contact the reporter on this story: Dani Burger in London at dburger7@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma, Cecile Gutscher

©2018 Bloomberg L.P.