The 1% Threat in Japan That Has Global Bond Markets on Edge

Kuroda's Curve Tweak May Have Just Put $2.4 Trillion in Play

(Bloomberg) -- With investor attention firmly on the spike in the Japanese 10-year yield this week, officials at the U.S. Treasury and France’s Agence France Trésor, will be looking at the longer end of the curve -- with trepidation.

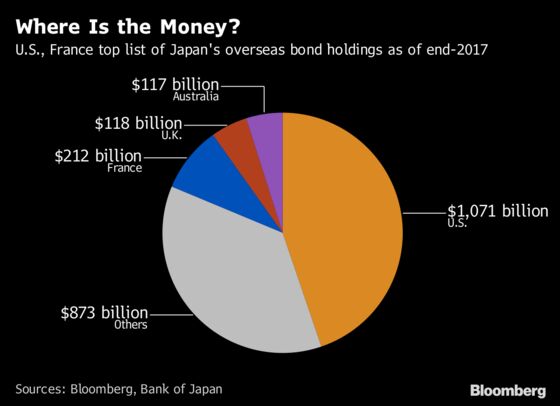

A yield of at least 1 percent on the 30-year JGB is seen as the level that will tempt Japanese investors to shift some of the $2.4 trillion of overseas debt they hold back home. The Bank of Japan’s new guidance, tolerating a 10-year yield of as high as 0.2 percent, could get longer-term bonds close to that, according to market participants.

The question is, will that be enough? Estimates based on typical spreads from the 10-year to the 30-year bond from MassMutual Life Insurance Co. and Daiwa SB Investments indicate the yield on the long-end may touch 0.95 percent to 1 percent.

“The 10-year yield will eventually rise to 0.2 percent over the longer-term,” said Shinji Kunibe, head of fixed income at Daiwa SB Investments in Tokyo. “A steeper yield curve will boost the relative allure of super-long Japanese government bonds as its carry and roll-down income exceeds that from overseas bonds after taking out currency hedging costs.”

The 30-year JGB yield rose to as high as 0.84 percent Thursday, up about 12 basis points from the end of June. It eased to 0.825 percent after the Bank of Japan conducted an unscheduled bond buying operation.

Volatility Returns

Volatility has returned to Japanese bond markets, after the central bank doubled the range allowed for its benchmark under its yield-curve control policy on Tuesday. Moves in 10-year government debt futures were so extreme on Wednesday -- a drop of as much as 0.5 percent, the most in almost two years -- that they triggered an emergency margin call from the clearing house.

Market participants expect yields to continue to rise, further steepening the curve and increasing the attraction of longer-maturity debt for Japan’s investors.

“The spread between 10 and 20 year yields is usually around 50 to 55 basis points, so if the 10-year yield rises to around 0.2 percent at most, the maximum for the 20-year yield would be around 0.75 percent,” said Satoshi Shimamura, head of rates and markets for investment strategy at MassMutual Life Insurance Co. “A similar spread between 20 and 30 year yields is about 20 basis points, which would put the 30-year’s upper end around 0.95 percent.”

Daiwa’s Kunibe sees the 10-year yield in a core range between 0.1 and 0.15 percent as market players find a new equilibrium. The yield on 20-year debt may rise to 0.7 percent while the 30-year may touch 1 percent, he said.

Forward Guidance

Still, while higher yields may help steepen the curve, the BOJ’s new forward guidance could moderate its steepness, said Shimamura. And for Akio Kato, general manager of trading at Mitsubishi UFJ Kokusai Asset Management Co. in Tokyo, the steepening is unlikely to be sustained.

“Considering that hedge costs still exist, flattening pressure will emerge after a steepening,” he said. “In light of arbitrage with foreign bonds, it’s hard to see the surge in super-long JGBs to be sustained at around 1 percent for 30 or 40-year bonds and around 0.2 percent for the 10-year yield.”

Before this week’s surge in yields, Japanese investors had already soured on Treasuries, with holdings recently falling to a seven-year low. They had been net buyers of French sovereign debt until May, when they turned net sellers for the first time since August 2017. At an auction on Thursday, France saw the lowest demand on its 20-year debt since at least 2007.

“Treasuries had already been lacking appeal after hedging costs compared to JGBs, but the latest move by the BOJ would be a slight headwind for French, as it’s certain that Japanese demand for France’s debt will decline,” said Kunibe.

--With assistance from John Ainger.

To contact the reporter on this story: Chikako Mogi in Tokyo at cmogi@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Cormac Mullen

©2018 Bloomberg L.P.