‘You're Going to Lose Money.’ $270 Billion Investor’s Bond Worry

A $270 billion investor is sounding the alarm bell on a strategy that’s grown increasingly popular.

(Bloomberg) -- A $270 billion investor is sounding the alarm bell on a strategy that’s grown increasingly popular with some of the world’s biggest bond funds.

AllianceBernstein’s Gershon Distenfeld reckons portfolios which have negative average duration have staked too much on a bet that yields will rise with growth and tighter policy. Any returns being made from the strategy in the current environment of rising interest rates and strong growth could quickly turn to losses when the cycle ends, he said.

“I understand the allure because people are taught that you don’t want to be in fixed income when rates go up,” Distenfeld, co-head of fixed income at the New York-based firm, said by phone. “But since no one knows when yields will go up, you’re going to lose money.”

A host of grand predictions from big-name investors on the direction of yields have fallen flat this year as trade tensions and late-cycle concerns prevent Treasuries from breaking higher in line with accelerating U.S. growth. That underscores the rising risks for a bet that was seen as a no-brainer when global expansion was synchronized.

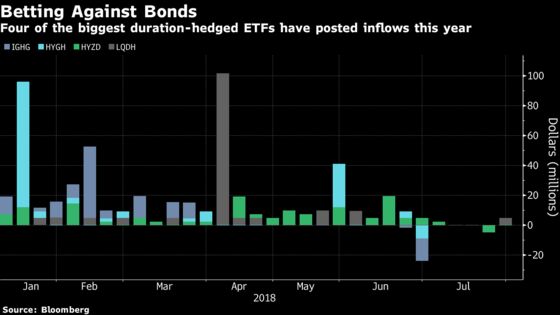

The strategy has captivated firms such as Franklin Templeton, which has used instruments like interest-rate swaps to short Treasuries in its flagship Global Bond Fund. Exchange-traded funds which hedge out U.S. bond duration are also growing in popularity, with total assets in the biggest portfolios nearly doubling this year to about $2 billion.

It’s been lucrative when it comes to U.S. bonds, which have risen this year despite benchmark 10-year yields struggling to breach the 3 percent mark. Duration-hedged ETFs have returned an average 2.3 percent, trouncing the Bloomberg Barclays global aggregate bond index, and both Goldman Sachs Asset Management and Franklin Templeton pointed to short Treasury positions as income generators in the second quarter, according to filings.

Similar bets on Europe have wrongfooted investors, however, including Bill Gross. His wager that German bund yields would close the gap with Treasuries led to a quarterly loss for the Janus Henderson Global Unconstrained Bond Fund.

Ashis Dash, an associate director at Morningstar Inc., said in an interview in late June that while a large number of funds have adopted the flexibility to go negative duration in the past decade, the risks are so high that most will only chose to use it tactically for very short periods of time.

Distenfeld argues that duration-hedged approaches can only outperform in the kind of late cycle environment markets are currently enjoying. Yet there are already signs growth may be fragile: In the euro zone, expansion is sputtering with at least a year still to go before rate liftoff by the European Central Bank.

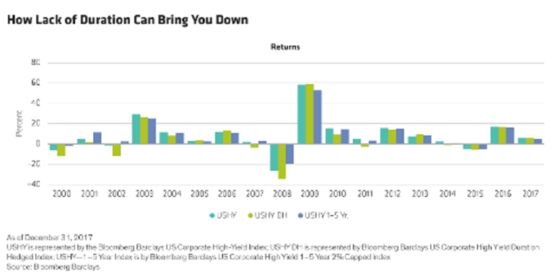

When the cycle ends and higher rates start to slow growth, the losses will mount very quickly, Distenfeld said. By his calculations, an investor who hedged duration in a U.S. high yield fund going into the 2008 financial crisis -- basically a worst case scenario -- would have posted losses exceeding 34 percent.

“You’re paying away a lot of carry to be short duration. It’s expensive, the timing is critical,” Distenfeld said. “History shows that very few people, if any, are able to time what’s going to happen to yields.”

--With assistance from Yakob Peterseil and Sid Verma.

To contact the reporter on this story: Natasha Doff in Moscow at ndoff@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Cecile Gutscher

©2018 Bloomberg L.P.