Great Earnings Meet Trade Threat and It's Splitting Markets

Trade risk meets banner earnings, creating ‘two-tier’ market.

(Bloomberg) -- Battle-lines are being drawn across markets as bears fret the brewing trade war and higher borrowing costs -- while bulls relish the banner corporate earnings season.

As a result, the winners and losers across asset classes and geographies are becoming ever-more pronounced.

“The tension between healthy current conditions and a future trade shock continues to reinforce two-tier market performance,” JPMorgan Chase & Co. strategists, headed by John Normand, wrote in a recent note.

Here’s a rundown of some of the largest market schisms right now.

America vs. the World

With over 90 percent of developed-market companies beating earnings expectations so far, according to JPMorgan, the bull market in stocks has firm foundations. Trade tensions, however, are forcing investors to separate the wheat from the chaff. One clear consequence is the outperformance of businesses tied to the U.S. economy.

S&P 500 Index stocks with the highest domestic-revenue exposure are firmly beating those with the most international sales, according to baskets compiled by Goldman Sachs Group Inc.

Since the start of June, domestically focused companies have gained 5.8 percent compared to their internationally oriented brethren, which are little changed. That’s a volte-face from last year when international companies outperformed by nearly 8 percentage points.

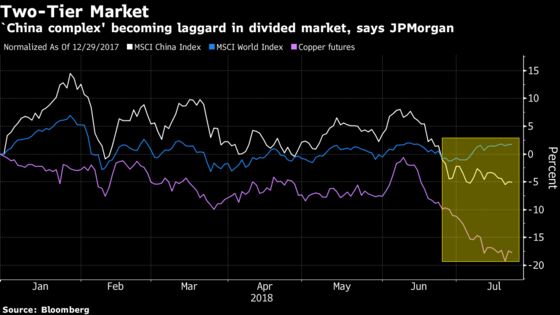

China Complex

JPMorgan points to another broad divergence on the back of trade tensions of late: resilient developed-market equities versus a beleaguered China complex. Asian equities and currencies have been plumbing new lows for the year alongside industrial metals.

Equity vs. Debt

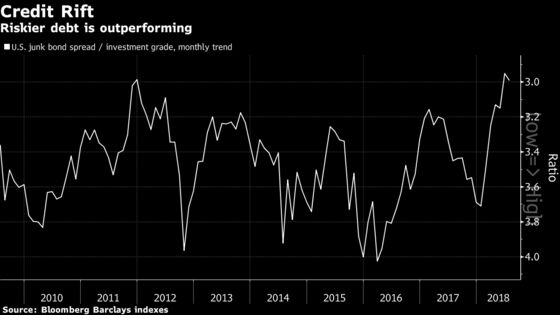

Credit and equity investors, meanwhile, are busy placing opposite bets on the business cycle.

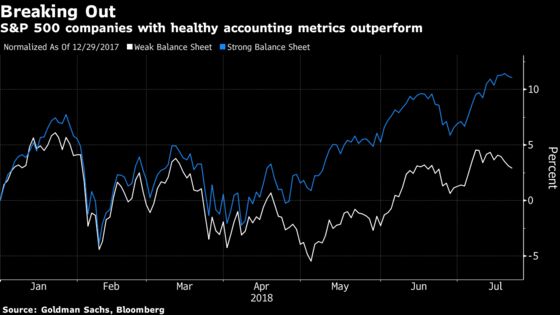

Stock buyers are bidding up companies with low debt loads and healthy financial metrics, and shunning those with the weakest financial ratios. The 50 S&P companies with the strongest balance sheets have outperformed their weaker equivalents for the past five quarters, the longest winning streak in at least 12 years, according to baskets compiled by Goldman Sachs.

Bonds issued by U.S. companies with stronger balance sheets, by contrast, are posting losses this year, while junk obligations are in the green.

The divide was confirmed in a Bank of America Corp. fund-manager survey this month, which showed a net 37 percent of equity investors covet an improvement in balance sheets. That’s a post-crisis record.

Fixed-income peers, meanwhile, are sanguine, with the proportion fretting “releveraging event risks” such as merger and acquisition activity declining to 23 percent in July from 32 percent the previous month.

Their bullish posture recalls the early stages of an economic recovery, according to BofA, while equity sentiment appears more late-cycle. One reason: rising borrowing costs are making debt-financed buybacks more expensive, capping stock gains going forward, according to Jared Woodard, a strategist at the U.S. bank.

Fiscal Funk

U.S. tax policy, meanwhile, has spurred splits within the S&P 500. American companies with the highest rates -- and therefore the most to gain from the fiscal agenda -- advanced 9 percentage points more than the low-tax basket in the second quarter, according to Goldman Sachs indexes. That’s the biggest quarterly spread in a decade.

All told, even as cross-asset volatility snoozes, the market landscape is looking more complex as macro headwinds gather pace.

“2018 has been a year of strong growth at the macro/economic and micro/earnings levels,” Mike Wilson, Morgan Stanley’s chief U.S. equity strategist, wrote in a Monday note. “Our concerns this year were never about growth, but about Fed policy that was tightening more than appreciated and the sustainability of the strong growth.”

To contact the reporters on this story: Sid Verma in London at sverma100@bloomberg.net;Dani Burger in London at dburger7@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Todd White

©2018 Bloomberg L.P.