UBS Investors Demand Sense of Urgency With Rivals Closing In

UBS Investors Demand a Sense of Urgency With Rivals Closing In

(Bloomberg) -- In the high-stakes drama of soured loans and failed investment banking ambitions that is European finance, Sergio Ermotti has a problem others would love to have: His UBS Group AG is starting to look a little dull.

Seven years after a sweeping revamp of the bank, whose tilt toward wealth management became a blueprint for rivals, the chief executive officer is overseeing one of the most stable lenders in Europe. The stock is trading at a premium to peers, clients are adding assets and the bank reports predictable profits.

But as turnaround plans at peers such as Credit Suisse Group AG gather speed, some investors are asking whether UBS is doing enough to sustain its lead.

“People I speak to are just concerned the story has got a bit boring, a bit stale," said Amit Goel, a bank analyst at Barclays Plc. “They’re looking at what’s the next thing that drives outperformance apart from that the market just goes up."

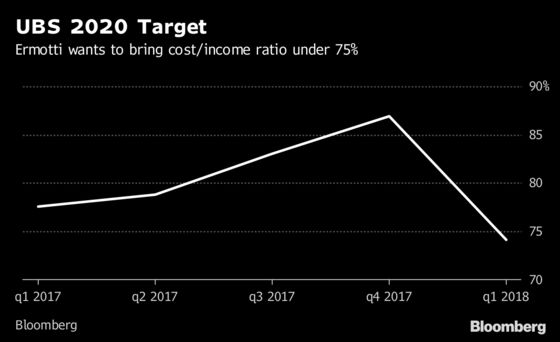

Ermotti tried to address such concerns with a strategy update in January, the first in four years, in which he outlined plans to buy back as much as 2 billion Swiss francs ($2 billion) of stock and merge the bank’s two huge wealth-management businesses. But the buyback did little to lift the stock, and the wealth merger was seen as lacking detail, leaving UBS’s shares trailing those of rivals including Credit Suisse and Barclays.

UBS fell 0.3 percent at 10:21 am in Zurich trading, bringing losses to 21 percent since the bank announced the buyback on Jan. 22. Credit Suisse has declined 17 percent in the period.

The CEO has another chance to persuade shareholders when UBS reports second-quarter earnings, scheduled for July 24. In a statement, the lender said that investors support its strategic direction and its updated targets point to “significant ongoing efficiency improvements.” It doesn’t make sense to announce a big public cost target because UBS is not in restructuring mode, the bank said.

“When you look at all key relative indicators, then it’s clear that we’re positioned at the top of our peer group,” UBS said. “Doing your homework early doesn’t make you less smart -- even when others decide to do theirs later and start improving. It’s no coincidence that UBS is one of the few banks that earns its cost of capital.”

Boosting the share price seems an increasingly Sisyphean task as the bank’s hard-won stability, a treasured trait in the aftermath of the financial crisis, is now being faulted for the stock’s lack of excitement. One top 20 shareholder, asking not to be identified, said their institution had held internal discussions about the reasons for the stock performance. One conclusion: UBS could communicate better on cost cuts compared with rival Credit Suisse.

UBS is the largest manager of billionaire money in the world. The bank’s $2.3 trillion wealth management business outstrips U.S. rivals Bank of America Corp. and Morgan Stanley. But unlike the American competitors, Switzerland’s largest bank has almost half of its wealth assets spread internationally managed in a jumble of booking centers and currencies. That, the bank contends, makes it a more complex and expensive business to run.

To benefit from the same synergies as U.S. rivals -- with pooled infrastructure and clientele -- Ermotti tasked Tom Naratil, head of the U.S. wealth business, and Martin Blessing, the former chief executive officer of Commerzbank AG, with the merger. Yet the move has been followed by few details since it was announced in January.

‘Show Me’

“The market is definitely in a show-me phase,” Jonathon Fearon, a fund manager who helps manage 648 billion euros ($753 billion) at Standard Life Aberdeen Plc, said by phone, adding that investors want to see an increase in sales and lower costs. “The merger of global wealth management is still to come. They haven’t really articulated yet the synergy there."

An internal strategy update for employees in late June talked of "seamless global business units" and “improving the client experience," while providing little in the way of specifics. At the time, it said the merger would give it more purchasing power because of the size of its asset base, as well as create savings in technology and innovation.

While it may be early in the wealth management merger project, investors would welcome a target for cutting the cost base, Martin Moeller, who oversees around $3 billion for Union Bancaire Privee, said in an interview.

“If it’s 2 percent of the wealth management cost base it would be embarrassing, 5 percent would be neutral, 10 percent -- convincing,” Moeller said.

Valuation Difference

To be sure, investors point to positive flows into wealth management as well as the bank’s efforts to boost capital. UBS, with a market value of about 59 billion francs, has a price-to-book ratio above European peers Credit Suisse, Barclays and Deutsche Bank AG, who’ve been distracted with costly restructuring programs.

Urs Beck, a fund manager at EFG International AG in Zurich, said UBS shares, which currently trade just above 15 francs, have dropped almost low enough to become attractive. He would consider buying at 14 francs.

"UBS isn’t a bad business -- it just trades at a substantial premium to Credit Suisse which we think is undeserved," David Herro, one of Credit Suisse’s largest investors said in an interview with Bloomberg TV earlier this month. The valuation difference “is huge between the two."

To contact the reporter on this story: Patrick Winters in Zurich at pwinters3@bloomberg.net

To contact the editors responsible for this story: Dale Crofts at dcrofts@bloomberg.net, Christian Baumgaertel, Paul Armstrong

©2018 Bloomberg L.P.